Answered step by step

Verified Expert Solution

Question

1 Approved Answer

hi can you do the first four questions thank you Q4. (12.5 marks) Dr. GRECO a young CEO who holds an MBA degree from the

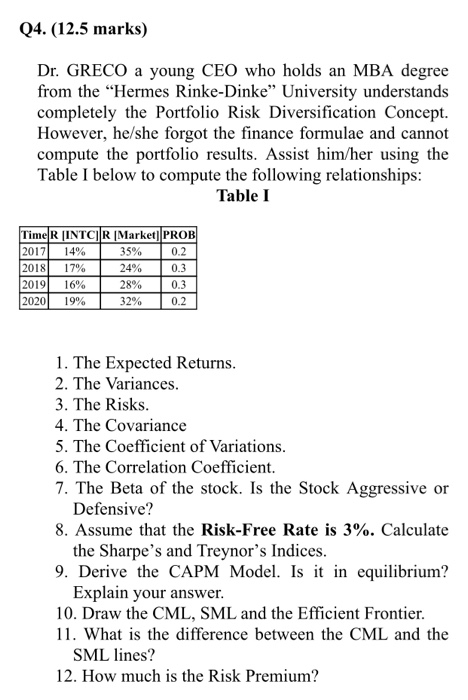

hi can you do the first four questions thank you Q4. (12.5 marks) Dr. GRECO a young CEO who holds an MBA degree from the Hermes Rinke-Dinke University understands completely the Portfolio Risk Diversification Concept. However, he/she forgot the finance formulae and cannot compute the portfolio results. Assist him/her using the Table I below to compute the following relationships: Table 1 Time R (INTCR Market] PROB 2017 14% 35% 0.2 2018 17% 24% 0.3 2019 16% 28% 0.3 2020 19% 32% 0.2 1. The Expected Returns. 2. The Variances. 3. The Risks. 4. The Covariance 5. The Coefficient of Variations. 6. The Correlation Coefficient. 7. The Beta of the stock. Is the Stock Aggressive or Defensive? 8. Assume that the Risk-Free Rate is 3%. Calculate the Sharpe's and Treynor's Indices. 9. Derive the CAPM Model. Is it in equilibrium? Explain your answer. 10. Draw the CML, SML and the Efficient Frontier. 11. What is the difference between the CML and the SML lines? 12. How much is the Risk Premium

hi can you do the first four questions thank you Q4. (12.5 marks) Dr. GRECO a young CEO who holds an MBA degree from the Hermes Rinke-Dinke University understands completely the Portfolio Risk Diversification Concept. However, he/she forgot the finance formulae and cannot compute the portfolio results. Assist him/her using the Table I below to compute the following relationships: Table 1 Time R (INTCR Market] PROB 2017 14% 35% 0.2 2018 17% 24% 0.3 2019 16% 28% 0.3 2020 19% 32% 0.2 1. The Expected Returns. 2. The Variances. 3. The Risks. 4. The Covariance 5. The Coefficient of Variations. 6. The Correlation Coefficient. 7. The Beta of the stock. Is the Stock Aggressive or Defensive? 8. Assume that the Risk-Free Rate is 3%. Calculate the Sharpe's and Treynor's Indices. 9. Derive the CAPM Model. Is it in equilibrium? Explain your answer. 10. Draw the CML, SML and the Efficient Frontier. 11. What is the difference between the CML and the SML lines? 12. How much is the Risk Premium

can you do the first four questions

thank you

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The True Value Of Bitcoin Revealed

Authors: Satoshi Nakaloco

1st Edition