Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Hi I request Help here QUESTION 1: (22 MARKS: 40 MINUTES) Superdade Limited is a company retailing in comic books and analysis the expenses by

Hi I request Help here

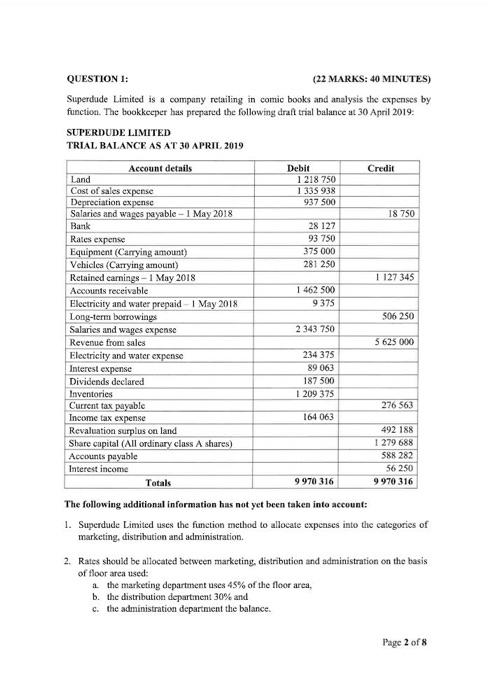

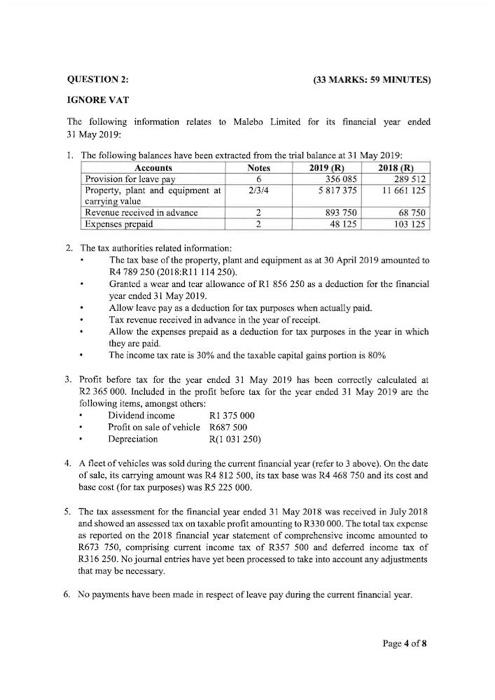

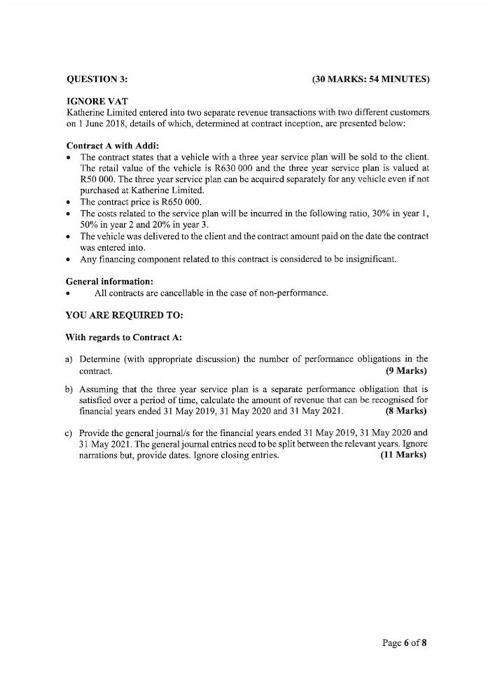

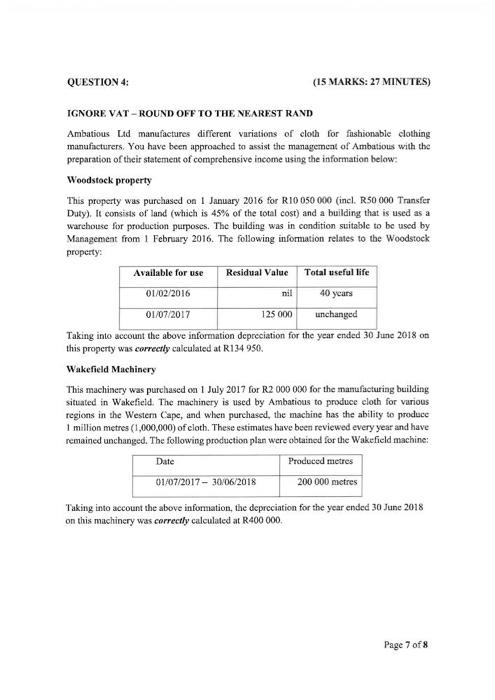

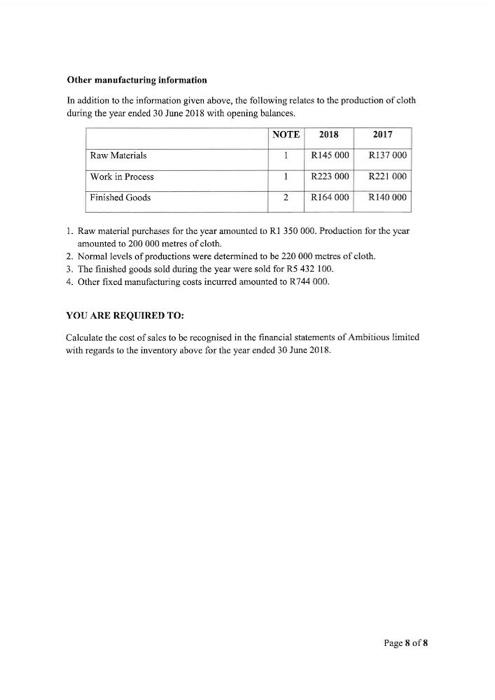

QUESTION 1: (22 MARKS: 40 MINUTES) Superdade Limited is a company retailing in comic books and analysis the expenses by function. The bookkeeper has prepared the following draft trial balance at 30 April 2019 : SUPERDUDE LIMITED TRIAL BALANCE AS AT 30 APRIL 2019 The following additional information has not yet been taken into account: 1. Superdude Limited uses the function method to allocate expenses into the categories of marketing, distribution and administration. 2. Rates should be allocated between marketing, distribution and administration on the basis of floor area used: a. the marketing department uses 45% of the floor area, b. the distribution department 30% and c. the administration departnient the balance. 3. Electricity and water should be alloeated between the marketing, distribution and administration departments in the ratio of 45:30:25. Electricity amounting to R18 750 was paid on 30 April 2019 for May 2019 electricity usage. 4. The land was revalued by R281 250 during the current year. There are no tax consequences relating to this revaluation surplus. 5. Salaries and wages are to be split between marketing, distribution and administration an a 30-35:35 basis. Salaries expenses incurred amounting to R40 242 was unpaid and unrecorded at 30 April 2019 . 6. Depreciation consists of depreciation on oflice equipment (25\%) and depreciation oa vehicles (75\%). The office equipment is used 60%/40% by marketing and administration respectively. Depreciation on vehicles constitutes 55% delivery vans (considered a distribution expense) and 45% depreciation on directors' company vehicles (considered to be an administration expense). 7. During the financial year ended 30 April 2019, ordinary shares amoanting to R526 481 were issed. 8. There is no other movement in other comprehensive income during the year other than that which is evident from the information provided. YOU ARE REQUIRED TO: IGNORE COMPARATIVES. ROUND OFF ALL. CAI.CULATIONS TO THE NEAREST RAND AMOUNT. Prepare the following in aceordance with IAS 1 Presentation of Financial Statements. 1. Statement of comprehensive income for the year ended 30 Aprit 2019 (18.5 Marks) 2. Statement of changes in equity for the year ended 30 Aprit 2019. (3.5 Marks) QUESTION 2: (33 MARKS: 59 MINUTES) IGNORE VAT The following information relates to Malebo Limited for its financial year ended 31 May 2019: 1. The foliowing balances have been extracted from the trial balance at 31 Mav 2019: 2. The tax authorities related information: - The tax base of the property, plant and equipment as at 30 April 2019 amouned to R4 789250 (2018:R11 114250). - Granted a wear and tear allowance of R1 856250 as a deductioa for the financial year ended 31 May 2019. - Allow leave pay as a deduction for tax purposes when actually paid. - Tax revenue received in advance in the year of receipt. - Allow the experses prepaid as a deduction for tax purposes in the year in which they are paid - The income tax rate is 30% and the taxable capital gains portion is 80% 3. Profit before tax for the year ended 31 May 2019 has been correctly calculated at R2 365000 . Included in the profit before tax for the year ended 31 May 2019 are the following items, amongst athers: --DividendincomeProfitonsaleofvehicleDepreciationR1375000R687500R(1031250) 4. A flect of vehicles was sold during the current financial year (refer to 3 above). On the date of sale, its carrying amount was R4 812500 , its tax base was R4 468750 and its cost and base cost (for tax purposes) was RS 225000 . 5. The tax assessment for the financial year ended 31 May 2018 was received in July 2018 and showed an assessed tax on taxable profit amounting to R330000. The total tax expense as reported on the 2018 financial year statement of comprehensive income amounted to R673 750 , comprising current income tax of R357 500 and deferred income tax of R.16 250 . No journal entries have yet been proceseed to take into account any adjustments that may be neeessary. 6. No payments have been made in respect of leave pay during the current financial year. 7. There are no other differences between accounting profit and taxable profit other than those evident from the infommation given. All amounts are considered material. 8. There are no components of other comprehensive income. YOU ARE REQUIRED TO: COMPARATIVES ARE NOT REQUTRED. a) Show how the tax expense note is disclosed in the annual financial statements of Malebo L.imited for the year ended 31 May 2019 in acoordance with Interiational Financial Reporting Standards. (31 Marks) b) Prepare an extract from the statement of comprehensive income of Malebo Limited for the year ended 31 May 2019 beginning with the line item 'profit before tax'. Notes are not required. (2 Marks) QUESTION 3: (30 MARKS: 54 MINUTES) IGNORE VAT Katherine Limited entered into two separate revenue transactions with two different customers on 1 June 2018 , details of which, determined at contract inception, are presented below; Contract A with Addi: - The contract states that a vehicle with a three year service plan will be sold to the client The retail value of the vehicle is R630000 and the three year service plan is valued at R50000. The three year service plan can be acquired separately for any vehicle even if not purchased at Katherine Limited. - The contract price is R 650000. - The costs reiated to the service plan will be incurred in the following ratio, 30% in year 1 , 50% in year 2 and 20% in year 3. - The vehicle was delivered to the client and the contract amount paid on the date the contract was entered into. - Any fikancing component related to this contract is considered to be insignificant. General information: All contracts are cancellable in the case of non-performance. YOU ARE REQUIRED TO: With regards to Contruct A : a) Determine (with appropriate discussion) the number of performanee obligations in the contract. (9 Marks) b) Assuming that the three year service plan is a seperate performance obligation that is setisfied over a period of time, calculate the amount of revenue that ean be recognised for financial years ended 31 May 2019, 31 May 2020 and 31 May 2021. ( 8 Marks) c) Provide the general journal/s for the financial years ended 31 May 2019, 31 Mny 2020 and 31 May 2021. The general journal entries need to be split berween the relevant years. Ignore narrations but, provide dates. Ignore closing entries. (11 Marks) IGNORE VAT - ROUND OFF TO THE NEAREST RAND Ambatious Ldd manufactures different variations of eloth for fashionable elothing manufacturers. You have been approached to assist the managencat of Ambatious with the preparation of their statement of comprebensive income using the information below: Woodstock property This property was purchased on 1 January 2016 for R10 050000 (incl. R50 000 Transfer Duty). It consists of land (which is 45% of the total cost) and a building that is used as a warehouse for production purposes. The building was in condition suitable to be used by Management from 1 February 2016. The following information relates to the Woodstock property: Taking into account the above information depreciation for the year ended 30 June 2018 on this property was correctly calculated at R.134 950. Wakefield Machinery This machinery was purchased oa 1 July 2017 for R2000000 for the manufacturing building situated in Wakefield. The machinery is used by Ambatious to produce eloth for various regions in the Westem Cape, and when purchased, the machine has the ability to produee 1 million metres (1,000,000) of eloth. These estimates bave been reviewed every year and have remained unchanged. The following production plan were obtained for the Wakefield machine: Taking into account the above information, the depreciation for the year ended 30 June 2018 on this machinery was correctly calculated at R400 000 . Other manufacturing information In addition to the information given above, the followisg relates to the production of eloth during the year ended 30 June 2018 with opening balances. 1. Raw material purchases for the year amounted to R.1 350000 . Production for the year amounted to 200000 metres of cloth. 2. Normal levels of productions were determined to be 220000 metres of cloth. 3. The finished goods sold during the year were sold for RS 432100 . 4. Other fixed marsufacturing costs incurred amoasted to R744000. YOU ARE REQUIRED TO: Calculate the cost of sales to be recognised in the financial statements of Ambitious limited with regards to the inventory above for the year ended 30 June 2018 . QUESTION 1: (22 MARKS: 40 MINUTES) Superdade Limited is a company retailing in comic books and analysis the expenses by function. The bookkeeper has prepared the following draft trial balance at 30 April 2019 : SUPERDUDE LIMITED TRIAL BALANCE AS AT 30 APRIL 2019 The following additional information has not yet been taken into account: 1. Superdude Limited uses the function method to allocate expenses into the categories of marketing, distribution and administration. 2. Rates should be allocated between marketing, distribution and administration on the basis of floor area used: a. the marketing department uses 45% of the floor area, b. the distribution department 30% and c. the administration departnient the balance. 3. Electricity and water should be alloeated between the marketing, distribution and administration departments in the ratio of 45:30:25. Electricity amounting to R18 750 was paid on 30 April 2019 for May 2019 electricity usage. 4. The land was revalued by R281 250 during the current year. There are no tax consequences relating to this revaluation surplus. 5. Salaries and wages are to be split between marketing, distribution and administration an a 30-35:35 basis. Salaries expenses incurred amounting to R40 242 was unpaid and unrecorded at 30 April 2019 . 6. Depreciation consists of depreciation on oflice equipment (25\%) and depreciation oa vehicles (75\%). The office equipment is used 60%/40% by marketing and administration respectively. Depreciation on vehicles constitutes 55% delivery vans (considered a distribution expense) and 45% depreciation on directors' company vehicles (considered to be an administration expense). 7. During the financial year ended 30 April 2019, ordinary shares amoanting to R526 481 were issed. 8. There is no other movement in other comprehensive income during the year other than that which is evident from the information provided. YOU ARE REQUIRED TO: IGNORE COMPARATIVES. ROUND OFF ALL. CAI.CULATIONS TO THE NEAREST RAND AMOUNT. Prepare the following in aceordance with IAS 1 Presentation of Financial Statements. 1. Statement of comprehensive income for the year ended 30 Aprit 2019 (18.5 Marks) 2. Statement of changes in equity for the year ended 30 Aprit 2019. (3.5 Marks) QUESTION 2: (33 MARKS: 59 MINUTES) IGNORE VAT The following information relates to Malebo Limited for its financial year ended 31 May 2019: 1. The foliowing balances have been extracted from the trial balance at 31 Mav 2019: 2. The tax authorities related information: - The tax base of the property, plant and equipment as at 30 April 2019 amouned to R4 789250 (2018:R11 114250). - Granted a wear and tear allowance of R1 856250 as a deductioa for the financial year ended 31 May 2019. - Allow leave pay as a deduction for tax purposes when actually paid. - Tax revenue received in advance in the year of receipt. - Allow the experses prepaid as a deduction for tax purposes in the year in which they are paid - The income tax rate is 30% and the taxable capital gains portion is 80% 3. Profit before tax for the year ended 31 May 2019 has been correctly calculated at R2 365000 . Included in the profit before tax for the year ended 31 May 2019 are the following items, amongst athers: --DividendincomeProfitonsaleofvehicleDepreciationR1375000R687500R(1031250) 4. A flect of vehicles was sold during the current financial year (refer to 3 above). On the date of sale, its carrying amount was R4 812500 , its tax base was R4 468750 and its cost and base cost (for tax purposes) was RS 225000 . 5. The tax assessment for the financial year ended 31 May 2018 was received in July 2018 and showed an assessed tax on taxable profit amounting to R330000. The total tax expense as reported on the 2018 financial year statement of comprehensive income amounted to R673 750 , comprising current income tax of R357 500 and deferred income tax of R.16 250 . No journal entries have yet been proceseed to take into account any adjustments that may be neeessary. 6. No payments have been made in respect of leave pay during the current financial year. 7. There are no other differences between accounting profit and taxable profit other than those evident from the infommation given. All amounts are considered material. 8. There are no components of other comprehensive income. YOU ARE REQUIRED TO: COMPARATIVES ARE NOT REQUTRED. a) Show how the tax expense note is disclosed in the annual financial statements of Malebo L.imited for the year ended 31 May 2019 in acoordance with Interiational Financial Reporting Standards. (31 Marks) b) Prepare an extract from the statement of comprehensive income of Malebo Limited for the year ended 31 May 2019 beginning with the line item 'profit before tax'. Notes are not required. (2 Marks) QUESTION 3: (30 MARKS: 54 MINUTES) IGNORE VAT Katherine Limited entered into two separate revenue transactions with two different customers on 1 June 2018 , details of which, determined at contract inception, are presented below; Contract A with Addi: - The contract states that a vehicle with a three year service plan will be sold to the client The retail value of the vehicle is R630000 and the three year service plan is valued at R50000. The three year service plan can be acquired separately for any vehicle even if not purchased at Katherine Limited. - The contract price is R 650000. - The costs reiated to the service plan will be incurred in the following ratio, 30% in year 1 , 50% in year 2 and 20% in year 3. - The vehicle was delivered to the client and the contract amount paid on the date the contract was entered into. - Any fikancing component related to this contract is considered to be insignificant. General information: All contracts are cancellable in the case of non-performance. YOU ARE REQUIRED TO: With regards to Contruct A : a) Determine (with appropriate discussion) the number of performanee obligations in the contract. (9 Marks) b) Assuming that the three year service plan is a seperate performance obligation that is setisfied over a period of time, calculate the amount of revenue that ean be recognised for financial years ended 31 May 2019, 31 May 2020 and 31 May 2021. ( 8 Marks) c) Provide the general journal/s for the financial years ended 31 May 2019, 31 Mny 2020 and 31 May 2021. The general journal entries need to be split berween the relevant years. Ignore narrations but, provide dates. Ignore closing entries. (11 Marks) IGNORE VAT - ROUND OFF TO THE NEAREST RAND Ambatious Ldd manufactures different variations of eloth for fashionable elothing manufacturers. You have been approached to assist the managencat of Ambatious with the preparation of their statement of comprebensive income using the information below: Woodstock property This property was purchased on 1 January 2016 for R10 050000 (incl. R50 000 Transfer Duty). It consists of land (which is 45% of the total cost) and a building that is used as a warehouse for production purposes. The building was in condition suitable to be used by Management from 1 February 2016. The following information relates to the Woodstock property: Taking into account the above information depreciation for the year ended 30 June 2018 on this property was correctly calculated at R.134 950. Wakefield Machinery This machinery was purchased oa 1 July 2017 for R2000000 for the manufacturing building situated in Wakefield. The machinery is used by Ambatious to produce eloth for various regions in the Westem Cape, and when purchased, the machine has the ability to produee 1 million metres (1,000,000) of eloth. These estimates bave been reviewed every year and have remained unchanged. The following production plan were obtained for the Wakefield machine: Taking into account the above information, the depreciation for the year ended 30 June 2018 on this machinery was correctly calculated at R400 000 . Other manufacturing information In addition to the information given above, the followisg relates to the production of eloth during the year ended 30 June 2018 with opening balances. 1. Raw material purchases for the year amounted to R.1 350000 . Production for the year amounted to 200000 metres of cloth. 2. Normal levels of productions were determined to be 220000 metres of cloth. 3. The finished goods sold during the year were sold for RS 432100 . 4. Other fixed marsufacturing costs incurred amoasted to R744000. YOU ARE REQUIRED TO: Calculate the cost of sales to be recognised in the financial statements of Ambitious limited with regards to the inventory above for the year ended 30 June 2018 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing The Auditors Waste And Abuse At Irs And Customs Hearing Before The Committee On Governmental Affairs United States Senate One Hundred Session August 4 1993

Authors: U. S. Committee On Governmental Affairs

1st Edition

1334865558, 978-1334865558