Question

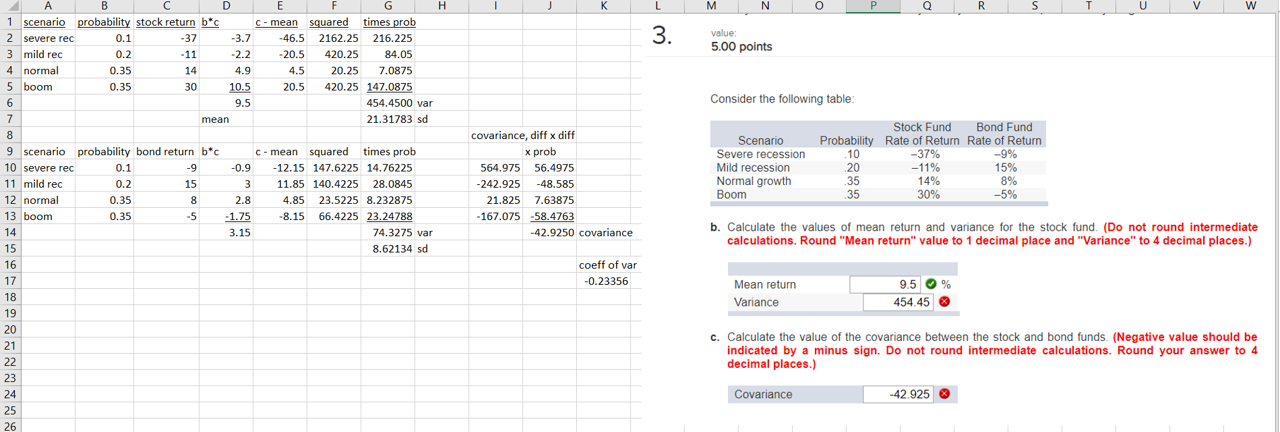

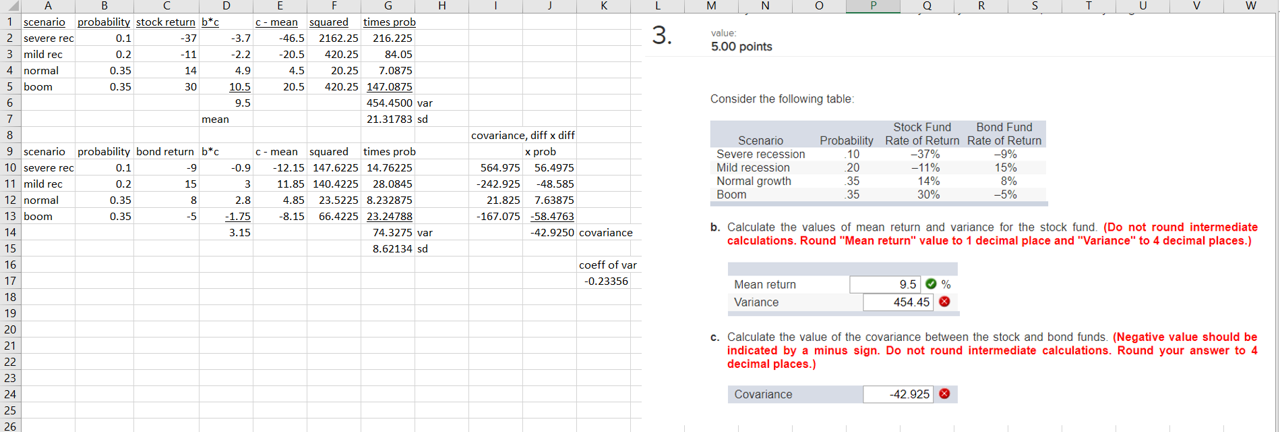

Hi, I'm taking a Finance Class called Securities Analysis and cannot for the life of me figure out this homework item. The attached screen shot

Hi, I'm taking a Finance Class called Securities Analysis and cannot for the life of me figure out this homework item. The attached screen shot includes the question, indicating with a red X my incorrect answers, with my calculations to the left. This is an online class and so far classmates and teacher have been unresponsive to my request for help. Thanks!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Institutions Management A Risk Management Approach

Authors: Anthony Saunders, Marcia Millon Cornett

9th edition

1259717771, 1259717772, 9781260048186, 1260048187, 978-1259717772