Question

Hi this is the question O n 1 February 2019 the bank account in the general ledger of Rush Retailers had a favourable balance of

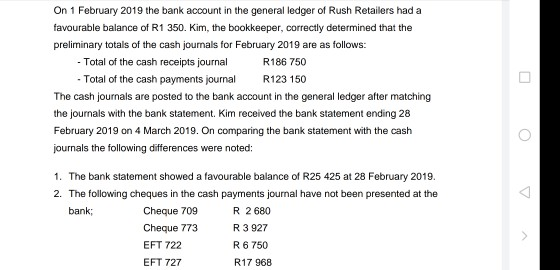

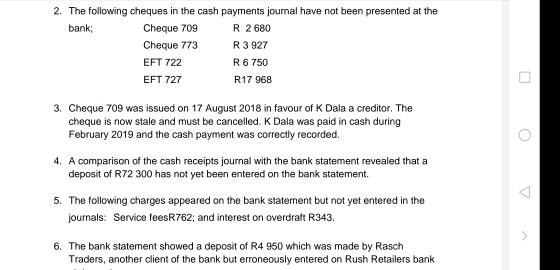

Hi this is the question On 1 February 2019 the bank account in the general ledger of Rush Retailers had a favourable balance of R1 350. Kim, the bookkeeper, correctly determined that the preliminary totals of the cash journals for February 2019 are as follows: - Total of the cash receipts journal R186 750 - Total of the cash payments journal R123 150 The cash journals are posted to the bank account in the general ledger after matching the journals with the bank statement. Kim received the bank statement ending 28 February 2019 on 4 March 2019. On comparing the bank statement with the cash journals the following differences were noted: 1. The bank statement showed a favourable balance of R25 425 at 28 February 2019. 2. The following cheques in the cash payments journal have not been presented at the bank; Cheque 709 R 2 680 Cheque 773 R 3 927 EFT 722 R 6 750 EFT 727 R17 968 3. Cheque 709 was issued on 17 August 2018 in favour of K Dala a creditor. The cheque is now stale and must be cancelled. K Dala was paid in cash during February 2019 and the cash payment was correctly recorded. 4. A comparison of the cash receipts journal with the bank statement revealed that a deposit of R72 300 has not yet been entered on the bank statement. 5. The following charges appeared on the bank statement but not yet entered in the journals: Service feesR762; and interest on overdraft R343. 6. The bank statement showed a deposit of R4 950 which was made by Rasch Traders, another client of the bank but erroneously entered on Rush Retailers bank statement.7. The cash receipts journal showed a deposit of R39 625 by a debtor, S Ndlovu, while the correct amount of R37 925 appeared on the bank statement. 8. A cheque number 972 drawn by Rasch Traders for R7 550 appeared on Rush Retailers bank statement but not in their journals. 9. A receipt of R16 350 issued to G Lucky, a debtor, was incorrectly entered in the cash receipts journal as R14 100. 10.Cheque number 769 for R4 605 in favour of M Stone, a creditor, was issued but subsequently cancelled and not given to the creditor. Kim erroneously entered the cheque payment in the cash payments journal. Required: Prepare the following for Rush Retailers for the month ended 28 February 2019: 1.1The supplementary cash receipts journal and the supplementary cash payments journal. Begin each journal with the relevant preliminary total provided above. Only the bank columns need to be completed. Total the bank column and post to the general ledger bank account. (8) 1.2Complete the general ledger bank account and balance the account as at 28 February 2019. (4) 1.3The bank reconciliation statement at 28 February 2019.

On 1 February 2019 the bank account in the general ledger of Rush Retailers had a favourable balance of R1 350. Kim, the bookkeeper, correctly determined that the preliminary totals of the cash journals for February 2019 are as follows: - Total of the cash receipts journal R186 750 Total of the cash payments journal R123 150 The cash journals are posted to the bank account in the general ledger after matching the journals with the bank statement. Kim received the bank statement ending 28 February 2019 on 4 March 2019. On comparing the bank statement with the cash journals the following differences were noted: 1. The bank statement showed a favourable balance of R25 425 at 28 February 2019. 2. The following cheques in the cash payments journal have not been presented at the bank: Cheque 709 R 2 680 Cheque 773 R3 927 EFT 722 R6 750 EFT 727 R17 968 2. The following cheques in the cash payments journal have not been presented at the bank: Cheque 709 R 2 680 Cheque 773 R3 927 EFT 722 R6 750 EFT 727 R17 968 3. Cheque 709 was issued on 17 August 2018 in favour of K Dala a creditor. The cheque is now stale and must be cancelled. K Dala was paid in cash during February 2019 and the cash payment was correctly recorded. 4. A comparison of the cash receipts journal with the bank statement revealed that a deposit of R72 300 has not yet been entered on the bank statement. 5. The following charges appeared on the bank statement but not yet entered in the journals: Service feesR762; and interest on overdraft R343. 6. The bank statement showed a deposit of R4 950 which was made by Rasch Traders, another client of the bank but erroneously entered on Rush Retailers bank 6. The bank statement showed a deposit of R4 950 which was made by Rasch Traders, another client of the bank but erroneously entered on Rush Retailers bank statement. 7. The cash receipts journal showed a deposit of R39 625 by a debtor, S Ndlovu, while the correct amount of R37 925 appeared on the bank statement. 8. A cheque number 972 drawn by Rasch Traders for R7 550 appeared on Rush Retailers bank statement but not in their journals. 9. A receipt of R16 350 issued to G Lucky, a debtor, was incorrectly entered in the cash receipts journal as R14 100. 10. Cheque number 769 for R4 605 in favour of M Stone, a creditor, was issued but subsequently cancelled and not given to the creditor. Kim erroneously entered the cheque payment in the cash payments journal. Required: Prepare the following for Rush Retailers for the month ended 28 February 2019: 1.1 The supplementary cash receipts journal and the supplementary cash payments journal. Begin each journal with the relevant preliminary total provided above. Only Required: Prepare the following for Rush Retailers for the month ended 28 February 2019: 1.1 The supplementary cash receipts journal and the supplementary cash payments journal. Begin each journal with the relevant preliminary total provided above. Only the bank columns need to be completed. Total the bank column and post to the general ledger bank account. (8) 1.2 Complete the general ledger bank account and balance the account as at 28 February 2019. 1.3 The bank reconciliation statement at 28 February 2019. QUESTION ONE [20] On 1 February 2019 the bank account in the general ledger of Rush Retailers had a favourable balance of R1 350. Kim, the bookkeeper, correctly determined that the preliminary totals of the cash journals for February 2019 are as follows: - Total of the cash receipts journal R186 750 - Total of the cash payments journal R123 150 The cash journals are posted to the bank account in the general ledger after matching the journals with the bank statement. Kim received the bank statement ending 28 February 2019 on 4 March 2019. On comparing the bank statement with the cash joumals the following differences were noted: 1. The bank statement showed a favourable balance of R25 425 at 28 February 2019. 2. The following cheques in the cash payments joumal have not been presented at the bank, Cheque 709 R 2 680 Cheque 773 R 3 927 EFT 722 R 6750 EFT 727 R17 968 3. Cheque 709 was issued on 17 August 2018 in favour of K Dala a creditor. The cheque is now stale and must be cancelled. K Dala was paid in cash during February 2019 and the cash payment was correctly recorded. the the bank statement revealed that a EFT 722 EFT 727 R6 750 R17 968 3. Cheque 709 was issued on 17 August 2018 in favour of K Dala a creditor. The cheque is now stale and must be cancelled. K Dala was paid in cash during February 2019 and the cash payment was correctly recorded. 4. A comparison of the cash receipts journal with the bank statement revealed that a deposit of R72 300 has not yet been entered on the bank statement 5. The following charges appeared on the bank statement but not yet entered in the journals: Service feesR762; and interest on overdraft R343. 6. The bank statement showed a deposit of R4 950 which was made by Rasch Traders, another client of the bank but erroneously entered on Rush Retailers bank statement. 7. The cash receipts journal showed a deposit of R39 625 by a debtor, S Ndlovu, while the correct amount of R37 925 appeared on the bank statement. 8. A cheque number 972 drawn by Rasch Traders for R7 550 appeared on Rush Retailers bank statement but not in their journals. 9. A receipt of R16 350 issued to G Lucky, a debtor, was incorrectly entered in the cash receipts journal as R14 100. 10. Cheque number 769 for R4 605 in favour of M Stone, a creditor, was issued but subsequently cancelled and not given to the creditor. Kim erroneously entered the cheque payment in the cash payments journalStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Modeling

Authors: Simon Benninga

3rd Edition

0262026287, 9780262026284