Answered step by step

Verified Expert Solution

Question

1 Approved Answer

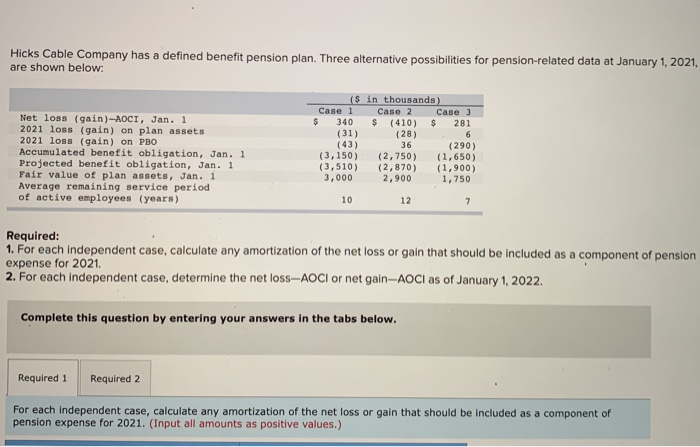

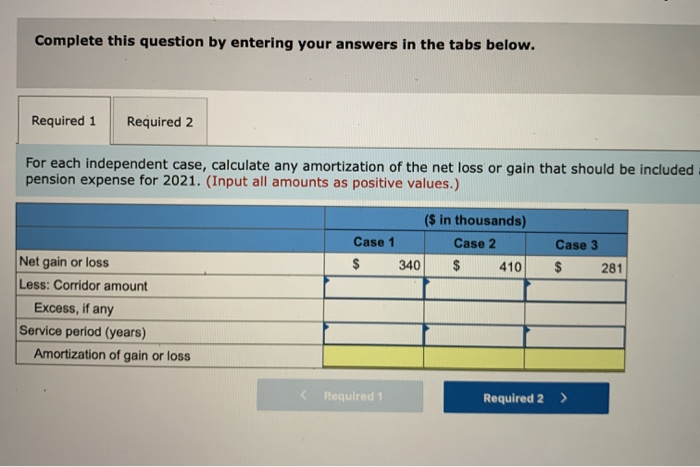

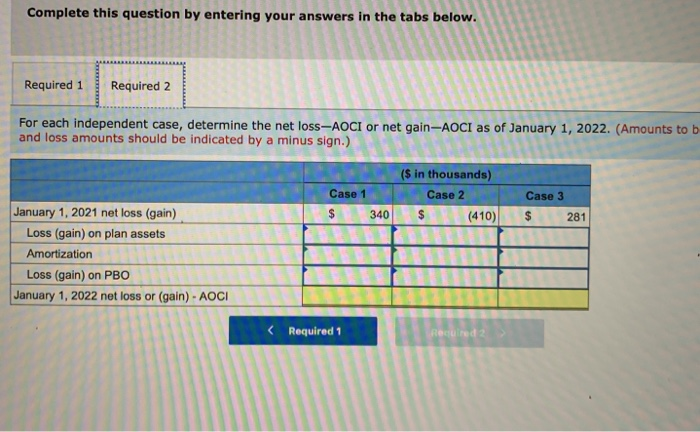

Hicks Cable Company has a defined benefit pension plan. Three alternative possibilities for pension-related data at January 1, 2021, are shown below: Net loss (gain)-AOCI,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Just Leave Me Alone Audit Clerk Knows What To Do Blank Lined Journal Funny Auditor Gifts For Women Men Funny Gift For Auditor Fun Finance Gifts An Auditor Who Loves Accounting And Auditing

Authors: Awesome Auditor

1st Edition

1659112699, 978-1659112696