Answered step by step

Verified Expert Solution

Question

1 Approved Answer

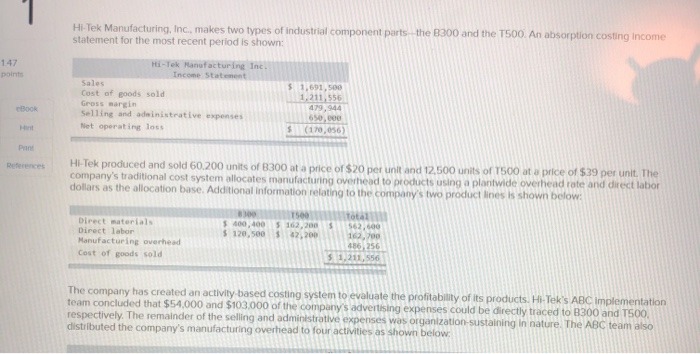

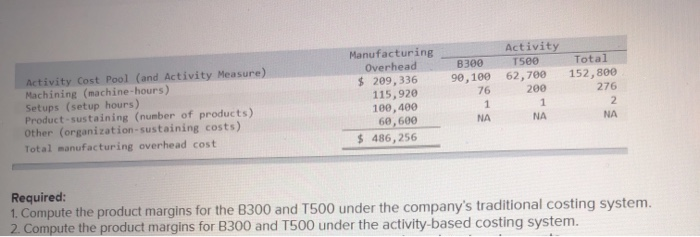

Hi-Tek Manufacturing, Inc, makes two types of industrial component parts the B300 and the T500. An absorption costing Income statement for the most recent period

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Auditing

Authors: Vasuhi M

1st Edition

6206150747, 978-6206150749