Answered step by step

Verified Expert Solution

Question

1 Approved Answer

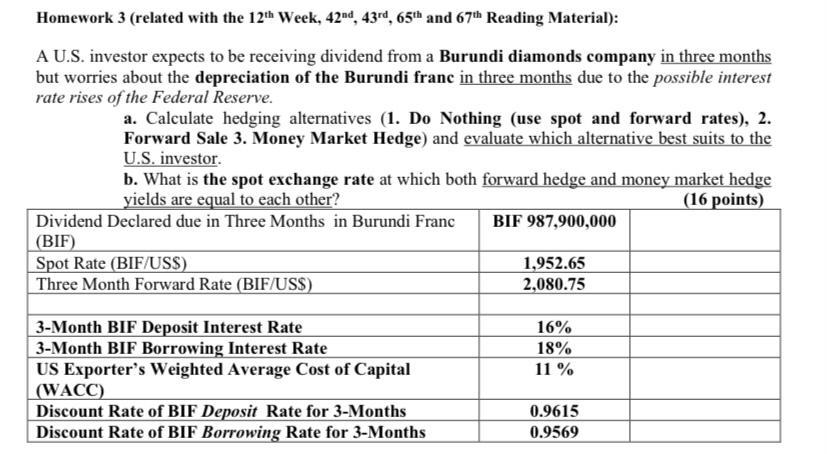

Homework 3 (related with the 12th Week, 42nd, 43rd, 65th and 67th Reading Material): A U.S. investor expects to be receiving dividend from a Burundi

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Diversity Quotas Diverse Perspectives The Case Of Gender

Authors: Stefan Gröschl , Junko Takagi

1st Edition

1409436195,1409461513