Answered step by step

Verified Expert Solution

Question

1 Approved Answer

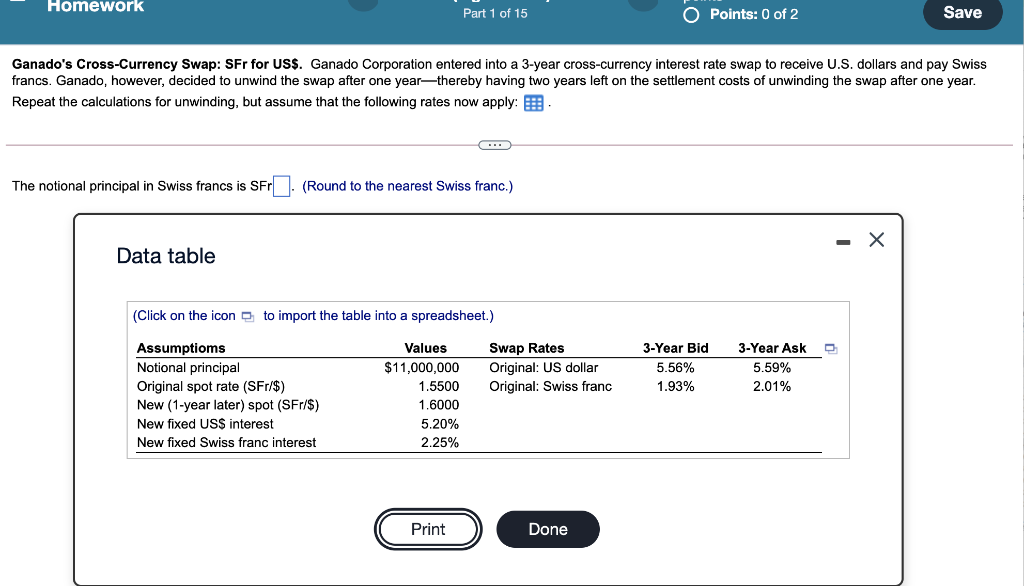

Homework Part 1 of 15 O Points: 0 of 2 Save Ganado's Cross-Currency Swap: SFr for US$. Ganado Corporation entered into a 3-year cross-currency interest

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Power Of Money How Ideas About Money Shaped The Modern World

Authors: Robert Pringle

1st Edition

3030258939,3030258947