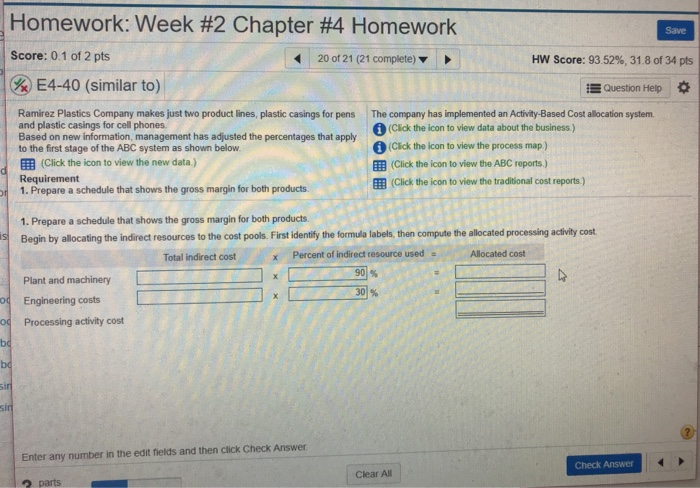

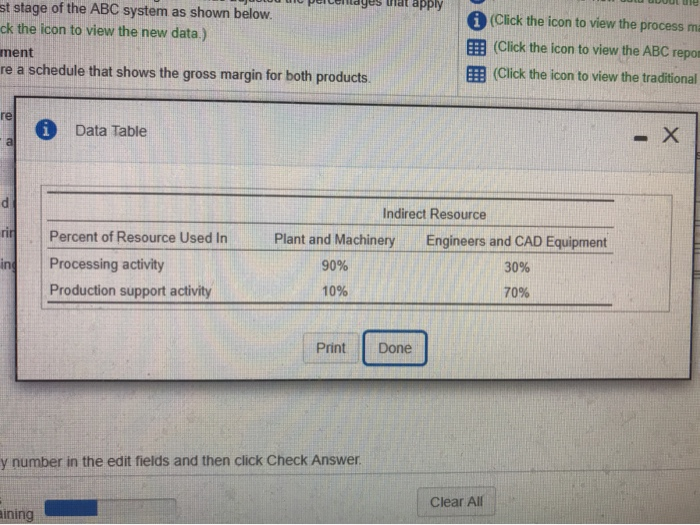

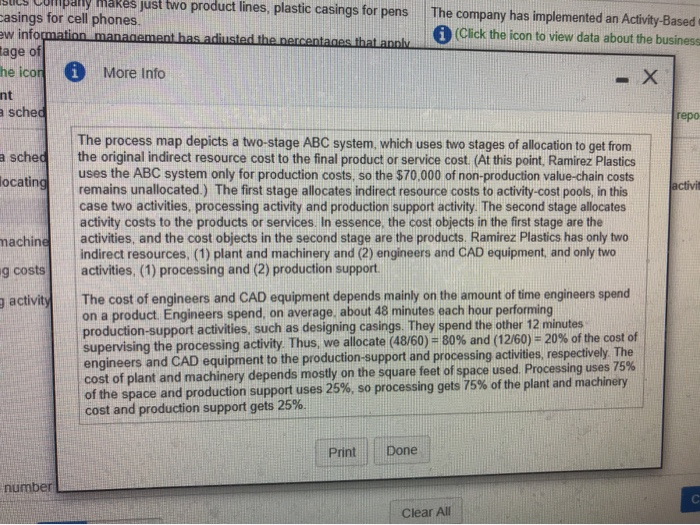

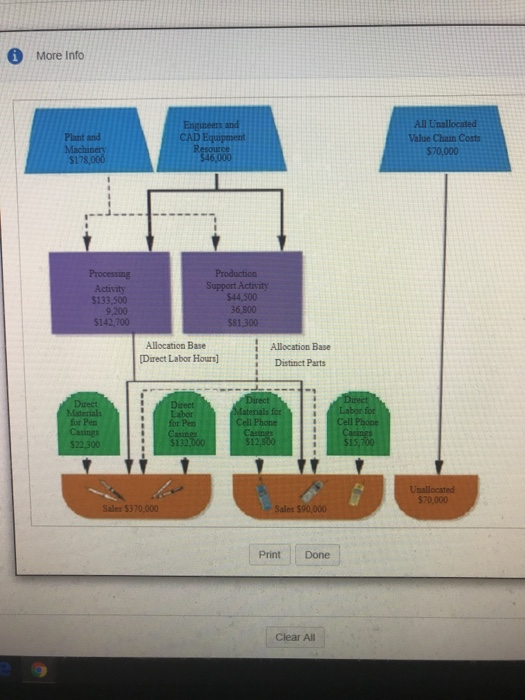

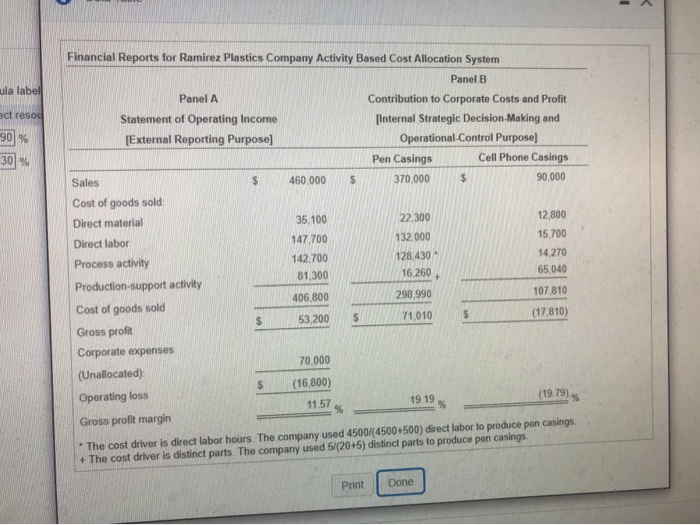

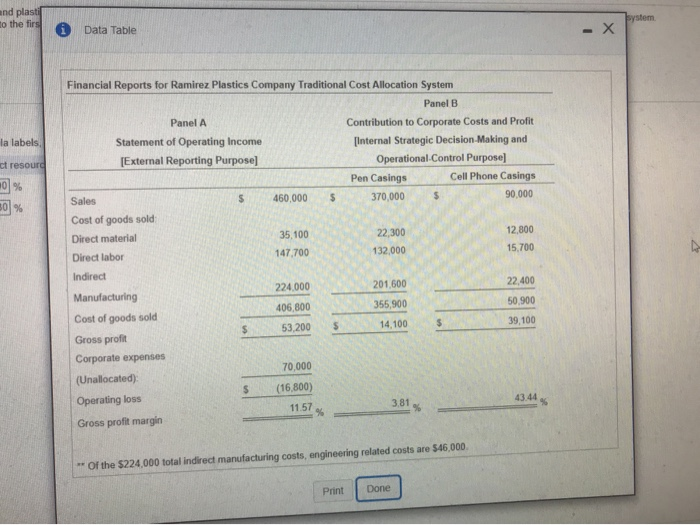

Homework: Week #2 Chapter #4 Homework Save Score: 0.1 of 2 pts 20 of 21 (21 complete) HW Score: 93 52%, 31.8 of 34 pts & E4-40 (similar to) Question Help * Ramirez Plastics Company makes just two product lines, plastic casings for pens The company has implemented an Activity-Based Cost allocation system. and plastic casings for cell phones Based on new information, management has adjusted the percentages that apply to the first stage of the ABC system as shown below EEB (Click the icon to view the new data) (Cick the icon to view data about the business ) i (Click the icon to view the process map) EEB (Click the icon to view the ABC reports) EB (Click the icon to view the traditional cost reports ) Requirement 1. Prepare a schedule that shows the gross margin for both products 1. Prepare a schedule that shows the gross margin for both products Begin by allocating the indirect resources to the cost pools. First identify the formula labels, then compute the allocated processing activity cost x Percent of indirect resource used - Allocated cost Total indirect costx 901 % Plant and machinery Engineering costs o Processing activity cost bo Enter any number in the edit fields and then click Check Answer Check Answer Clear All o parts ho percenild ges that apply st stage of the ABC system as shown below ck the icon to view the new data.) 1 (Click the icon to view the process ma (click the icon to view the ABC repo ment EEB (Click the icon to view the traditional re a schedule that shows the gross margin for both products re i Data Table Indirect Resource Engineers and CAD Equipment Plant and Machinery Resource Used In 30% 90% n Processing activity 70% 10% Production support activity Print Done y number in the edit fields and then click Check Answer Clear All ining ls Colmpally makes just two product lines, plastic casings for pens The company has implemented an Activity-Based asings for cell phones. i (Click the icon to view data about the business age of he icor i More Info nt sched epo The process map depicts a two-stage ABC system, which uses two stages of allocation to get from a sched the original indirect resource cost to the final product or service cost (At this point, Ramirez Plastics uses the ABC system only for production costs, so the $70,000 of non-production value-chain costs remains unallocated.) The first stage allocates indirect resource costs to activity-cost pools, in this case two activities, processing activity and production support activity. The second stage allocates activity costs to the products or services. In essence, the cost objects in the first stage are the nachine activities, and the cost objects in the second stage are the products. Ramirez Plastics has only two indirect resources, (1) plant and machinery and (2) engineers and CAD equipment, and only two ocating ctivit g costsactivities, (1) processing and (2) production support activity The cost of engineers and CAD equipment depends mainly on the amount of time engineers spend on a product Engineers spend, on average, about 48 minutes each hour performing production-support activities, such as designing casings. They spend the other 12 minutes supervising the processing activity Thus, we allocate (4860)-80% and (1260) 20% of the cost of engineers and CAD equipment to the production-support and processing activities, respectively The l cost of plant and machinery depends mostly on the square feet of space used. Processing uses 75% of the space and production support uses 25%, so processing gets 75% of the plant and machinery cost and production support gets 25%. PrintDone number l Clear All More Info and Plant and CAD Equipment Vale Chain Costs $70,000 Machinery $178,000 Production Support Activity $44,500 Activity $133,500 9,200 $142,700 36,800 $81,300 Allocation Base Allocation Base Direct Labor Hours Distinet Parts Ditect Materials for Pen Casings Direct Labor for Cell Phone Cas for Pen Unallocated $70,000 Sales $370,000 Sales $90,000 PrintDone Clear All Financial Reports for Ramirez Plastics Company Activity Based Cost Allocation System Panel B Panel A Contribution to Corporate Costs and Profit ct r Statement of Operating Income Internal Strategic Decision-Making and 901 % [External Reporting Purposel Operational-Control Purpose 30 % Pen Casings Cell Phone Casings Sales S 460.000 S370,000 90,000 Cost of goods sold: Direct material 35.100 22,300 12,800 Direct labor 147,700 15,700 1 132.000 128.430 16.260 Process activity 142,700 14,270 81,300 65,040 Production-support activity 298,990 07,810 406,800 Cost of goods sold 1,010 (17,810) 3,200 Gross profit Corporate expenses 70,000 (Unallocated) (16.800) Operating loss (19.79) % 19.19 11.57 Gross profit margin The cost driver is direct labor hours. The company used 4500/(4500+500) direct labor to produce pen casings + The cost driver is distinct parts The company used 5/(20+5) distinct parts to produce pen casings Print Done nd plasti the Data Table Financial Reports for Ramirez Plastics Company Traditional Cost Allocation System Panel B Panel A Contribution to Corporate Costs and Profit la labels Statement of Operating Income [Internal Strategic Decision -Making and [External Reporting Purposel ct resourc Operational.Control Purposel % Pen Casings Cell Phone Casings S460,000 S370,000 % | | Sales 90,000 Cost of goods sold Direct material 35,100 22,300 12,800 Direct labor 47,700 132,000 15,700 Indirect 201,600 224.000 22,400 Manufacturing 355,900 406,800 50,900 Cost of goods sold 14,100 53,200 39,100 Gross profit Corporate expenses 70,000 (Unallocated) S(16,800) Operating loss 3.81 43.44 11.57 Gross profit margin " Of the $224,000 total indirect manufacturing costs, engineering related costs are $46,000 Print Done Homework: Week #2 Chapter #4 Homework Save Score: 0.1 of 2 pts 20 of 21 (21 complete) HW Score: 93 52%, 31.8 of 34 pts & E4-40 (similar to) Question Help * Ramirez Plastics Company makes just two product lines, plastic casings for pens The company has implemented an Activity-Based Cost allocation system. and plastic casings for cell phones Based on new information, management has adjusted the percentages that apply to the first stage of the ABC system as shown below EEB (Click the icon to view the new data) (Cick the icon to view data about the business ) i (Click the icon to view the process map) EEB (Click the icon to view the ABC reports) EB (Click the icon to view the traditional cost reports ) Requirement 1. Prepare a schedule that shows the gross margin for both products 1. Prepare a schedule that shows the gross margin for both products Begin by allocating the indirect resources to the cost pools. First identify the formula labels, then compute the allocated processing activity cost x Percent of indirect resource used - Allocated cost Total indirect costx 901 % Plant and machinery Engineering costs o Processing activity cost bo Enter any number in the edit fields and then click Check Answer Check Answer Clear All o parts ho percenild ges that apply st stage of the ABC system as shown below ck the icon to view the new data.) 1 (Click the icon to view the process ma (click the icon to view the ABC repo ment EEB (Click the icon to view the traditional re a schedule that shows the gross margin for both products re i Data Table Indirect Resource Engineers and CAD Equipment Plant and Machinery Resource Used In 30% 90% n Processing activity 70% 10% Production support activity Print Done y number in the edit fields and then click Check Answer Clear All ining ls Colmpally makes just two product lines, plastic casings for pens The company has implemented an Activity-Based asings for cell phones. i (Click the icon to view data about the business age of he icor i More Info nt sched epo The process map depicts a two-stage ABC system, which uses two stages of allocation to get from a sched the original indirect resource cost to the final product or service cost (At this point, Ramirez Plastics uses the ABC system only for production costs, so the $70,000 of non-production value-chain costs remains unallocated.) The first stage allocates indirect resource costs to activity-cost pools, in this case two activities, processing activity and production support activity. The second stage allocates activity costs to the products or services. In essence, the cost objects in the first stage are the nachine activities, and the cost objects in the second stage are the products. Ramirez Plastics has only two indirect resources, (1) plant and machinery and (2) engineers and CAD equipment, and only two ocating ctivit g costsactivities, (1) processing and (2) production support activity The cost of engineers and CAD equipment depends mainly on the amount of time engineers spend on a product Engineers spend, on average, about 48 minutes each hour performing production-support activities, such as designing casings. They spend the other 12 minutes supervising the processing activity Thus, we allocate (4860)-80% and (1260) 20% of the cost of engineers and CAD equipment to the production-support and processing activities, respectively The l cost of plant and machinery depends mostly on the square feet of space used. Processing uses 75% of the space and production support uses 25%, so processing gets 75% of the plant and machinery cost and production support gets 25%. PrintDone number l Clear All More Info and Plant and CAD Equipment Vale Chain Costs $70,000 Machinery $178,000 Production Support Activity $44,500 Activity $133,500 9,200 $142,700 36,800 $81,300 Allocation Base Allocation Base Direct Labor Hours Distinet Parts Ditect Materials for Pen Casings Direct Labor for Cell Phone Cas for Pen Unallocated $70,000 Sales $370,000 Sales $90,000 PrintDone Clear All Financial Reports for Ramirez Plastics Company Activity Based Cost Allocation System Panel B Panel A Contribution to Corporate Costs and Profit ct r Statement of Operating Income Internal Strategic Decision-Making and 901 % [External Reporting Purposel Operational-Control Purpose 30 % Pen Casings Cell Phone Casings Sales S 460.000 S370,000 90,000 Cost of goods sold: Direct material 35.100 22,300 12,800 Direct labor 147,700 15,700 1 132.000 128.430 16.260 Process activity 142,700 14,270 81,300 65,040 Production-support activity 298,990 07,810 406,800 Cost of goods sold 1,010 (17,810) 3,200 Gross profit Corporate expenses 70,000 (Unallocated) (16.800) Operating loss (19.79) % 19.19 11.57 Gross profit margin The cost driver is direct labor hours. The company used 4500/(4500+500) direct labor to produce pen casings + The cost driver is distinct parts The company used 5/(20+5) distinct parts to produce pen casings Print Done nd plasti the Data Table Financial Reports for Ramirez Plastics Company Traditional Cost Allocation System Panel B Panel A Contribution to Corporate Costs and Profit la labels Statement of Operating Income [Internal Strategic Decision -Making and [External Reporting Purposel ct resourc Operational.Control Purposel % Pen Casings Cell Phone Casings S460,000 S370,000 % | | Sales 90,000 Cost of goods sold Direct material 35,100 22,300 12,800 Direct labor 47,700 132,000 15,700 Indirect 201,600 224.000 22,400 Manufacturing 355,900 406,800 50,900 Cost of goods sold 14,100 53,200 39,100 Gross profit Corporate expenses 70,000 (Unallocated) S(16,800) Operating loss 3.81 43.44 11.57 Gross profit margin " Of the $224,000 total indirect manufacturing costs, engineering related costs are $46,000 Print Done