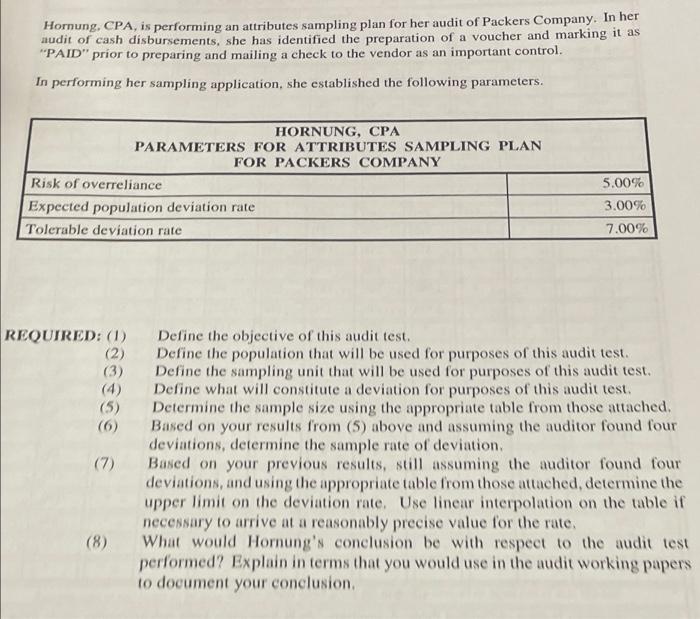

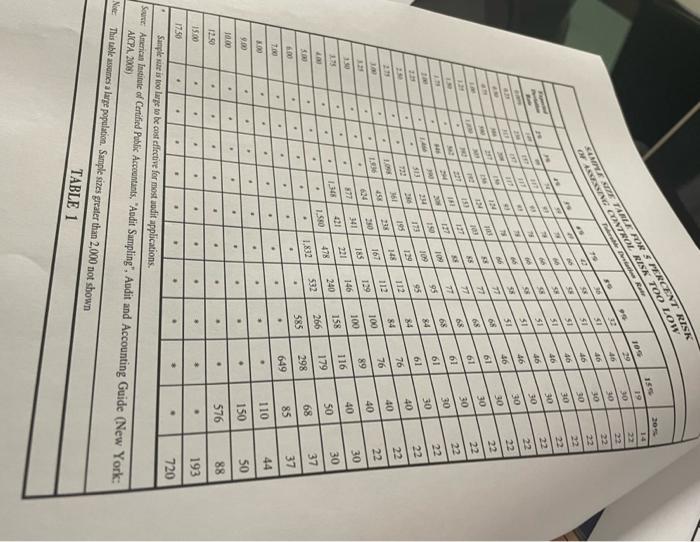

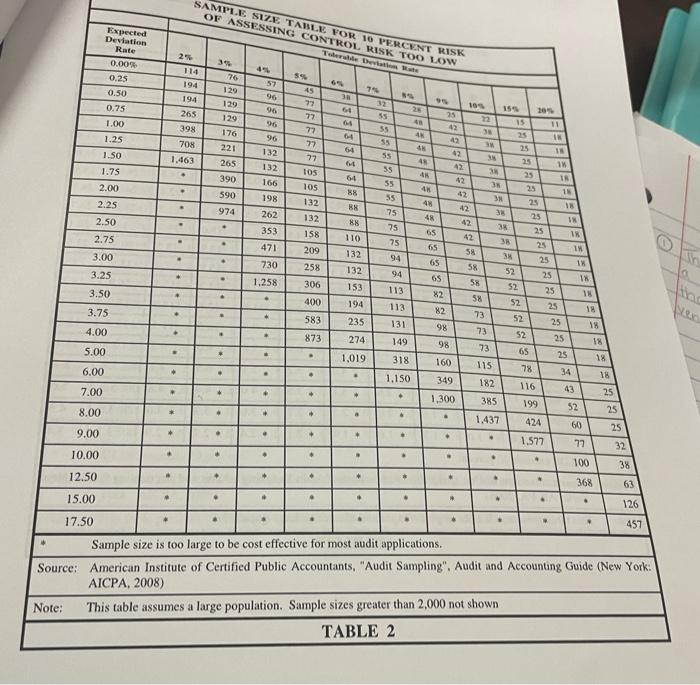

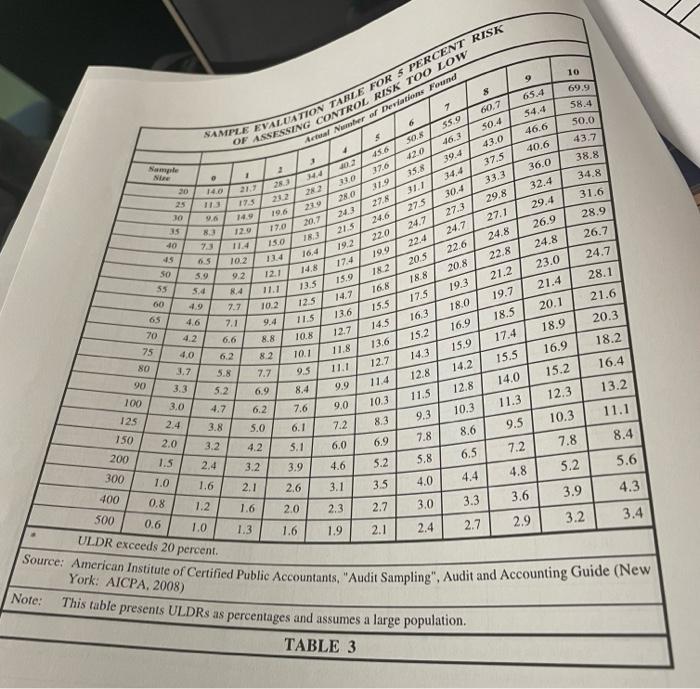

Hornung, CPA, is performing an attributes sampling plan for her audit of Packers Company. In her audit of cash disbursements, she has identified the preparation of a voucher and marking it as "PAID" prior to preparing and mailing a check to the vendor as an important control. In performing her sampling application, she established the following parameters. HORNUNG, CPA PARAMETERS FOR ATTRIBUTES SAMPLING PLAN FOR PACKERS COMPANY Risk of overreliance Expected population deviation rate Tolerable deviation rate 5.00% 3.00% 7.00% REQUIRED: (1) (2) (3) (4) (6) (7) Define the objective of this audit test. Define the population that will be used for purposes of this audit test. Define the sampling unit that will be used for purposes of this audit test. Define what will constitute a deviation for purposes of this audit test. Determine the sample size using the appropriate table from those attached. Based on your results from (5) above and assuming the auditor found four deviations, determine the sample rate of deviation Based on your previous results, still assuming the auditor found four deviations, and using the appropriate table from those attached, determine the upper limit on the deviation rate. Use linear interpolation on the table if necessary to arrive at a reasonably precise value for the rate: What would Hornung's conclusion be with respect to the audit test performed? Explain in terms that you would use in the audit working papers to document your conclusion, (8) 20 PE sor 61 26 0 19 46 22 30 22 SI 10 9F BO 22 OFERING CONTROL RISK TOO LOW SAMPLE SEE TABLE FOR S PERCENT RISK P. Rate 16 30 51 $1 97 OL 22 22 SF S 97 30 SI 16 46 31 31 30 30 30 36 9 22 22 12 39 61 CH 77 77 77 30 99 61 22 57 30 68 127 THE 22 61 77 68 30 100 $ 61 22 ME 84 30 ES 19 333 I 18 40 22 22 72 . 76 M AT . 40 195 23 20 109 05 129 95 145 112 167 112 185 146 84 100 76 1. 22 40 89 341 100 30 377 40 221 . 21 293 116 158 1.345 30 . 240 . 478 50 UT 179 2.5D . . TES 266 585 1,832 37 89 . 298 . . . 6.00 TO 37 85 . . 649 . . . . . . 110 44 . . . 006 . 150 50 10.00 . . . . . . 576 . . . . . 88 12.50 193 15.00 17.50 720 Sample size is too large so be cost effective for most odit applications Ser American Institute of Certified Public Accountants, "Audit Sampling". Audit and Accounting Guide (New York: . Nice AICPA, 2008) This table assumes a large population Sample sizes greater than 2,000 not shown TABLE 1 SAMPLE SIZE TABLE VOR 10 PERCENT RISK OF ASSESSING CONTROL RISK TOO LOW orale talartlantats Expected Deviation Rate 0.00% 0.25 0.50 25 114 76 129 7 129 0.75 194 194 265 398 57 96 96 56 96 129 20 25 1.00 06 22 15 45 77 77 72 77 77 105 55 SIE 11 IN 1.25 176 221 64 SS 3 48 G 708 1.463 /// 25 1.50 1.75 55 265 66 25 42 1 55 . 06 390 45 132 132 166 198 262 DIE 42 55 105 33 TR 16 2.00 2.25 590 42 55 25 25 25 25 48 B SN 38 IN 974 42 75 2.50 88 353 75 35 132 132 158 209 258 IN 18 65 25 2.75 110 42 38 65 25 SX 18 3.00 . 3 471 730 1.258 132 132 75 94 94 113 65 18 58 52 E 3.25 3.50 25 25 25 65 82 306 58 58 18 18 . 400 153 194 235 52 52 52 the Nex 113 82 3.75 18 73 583 131 25 25 25 98 18 4.00 73 873 52 274 149 98 18 5.00 73 65 1,019 25 318 160 115 6.00 . 34 1.150 349 182 78 116 18 18 25 25 7.00 43 . 1,300 385 52 8.00 + . . 1,437 199 424 1.577 8/3/3/9/*/ 25 9.00 + . . . 77 32 10.00 100 38 12.50 368 63 15.00 . 126 17.50 457 Sample size is too large to be cost effective for most audit applications. Source: American Institute of Certified Public Accountants, "Audit Sampling". Audit and Accounting Guide (New York: AICPA, 2008) Note: This table assumes a large population. Sample sizes greater than 2,000 not shown TABLE 2 10 9 $ 65.4 69.9 58.4 59 deal Namber of Deviations Found SAMPLE EVALUATION TABLE FOR S PERCENT RISK OF ASSESSING CONTROL RISK TOO LOW 54.4 46.6 40.6 36.0 Namysle 2 50.0 43.7 38.8 34.8 31.6 28.9 26.7 30 25 10 15 1.6 8 28 14.4 282 282 219 207 183 213 16.4 19.2 7 6 5 . 60,7 1022 50.8 56 50.4 -16.3 37.6 TO 12.0 280 43.0 15.8 319 39.4 243 27.8 31.1 14.4 37.5 24.6 275 30.4 33.3 24.7 27.3 29.8 22.4 24.7 27.1 182 205 24.8 18.8 20.8 32.4 29.4 26.9 24.8 23.0 220 40 73 0.5 19.9 22.6 15 22.8 24.7 SO 1 14.0 27,7 195 149 19.6 12.9 17.0 114 15.0 10.2 134 9.2 12.1 11.1 10.2 9.4 11.5 8.8 10.8 10.1 9.5 15.9 21.2 28.1 55 5.9 5.4 4.9 21.4 8.4 19.3 19.7 21.6 00 180 20.1 65 4.6 14.8 17.4 13.5 12.5 14.7 13.6 12.7 11.8 12.7 168 15.5 14.5 13.6 7.7 7.1 6.6 18.5 17.5 16,3 15.2 20.3 16.9 18.9 70 4.2 17.4 15.9 16.9 6.2 14.3 18.2 16.4 75 80 90 15.5 8.2 7.7 14,2 11.1 9.9 12.8 15.2 11.4 4.0 3.7 3.3 3.0 2.4 14.0 5.8 5.2 4.7 6.9 8.4 12.8 13.2 11.5 12.3 10.3 11.3 9.0 100 125 6.2 7.6 10.3 9.3 11.1 10.3 8.3 3.8 5.0 6.1 7.2 9.5 8.6 150 7.8 2.0 8.4 3.2 7.8 5.1 6.9 6.0 7.2 200 4.2 3.2 6.5 1.5 2.4 5.8 3 4.6 3.9 5.2 5.6 5.2 N 4.8 300 4.4 1.0 1.6 1 4.0 2.1 2.6 3.1 3.5 3.9 4.3 400 0.8 3.6 1.2 3.3 1.6 2.0 2.3 2.7 3.0 2.4 3.2 3.4 2.9 500 0.6 1.0 ULDR exceeds 20 percent 1.3 1.6 1.9 2.7 2.1 Source: American Institute of Certified Public Accountants, "Audit Sampling", Audit and Accounting Guide (New Note: York: AICPA, 2008) This table presents ULDRs as percentages and assumes a large population. TABLE 3 SAMPLE EVALUATION TABLE FOR 10 PERCENT RISK OF ASSESSING CONTROL RISK TOO LOW Actual Number of Deviations Found Sample Size 20 25 30 35 1 0 10.9 18.1 4 4 8.8 14.7 6 7.4 463 36.1 29.5 24.9 12.4 10.7 56.5 7 51.9 426 6.4 5 415 140 28. 24.9 38.4 40 5.6 36.2 21.6 32.5 28.2 45 P 2 3 24.5 30.5 20.0 24.9 16.8 21.0 14.5 18.2 12.8 16.0 11.4 14.3 10.3 12.9 9.4 11.8 8.7 10.8 8.0 7.5 5.0 4.6 8.4 SO 249 7.6 SS 19.0 17.0 15.4 14.1 4.2 22.0 19.7 17.8 16.3 6.9 60 3.8 6.4 65 3.5 70 223 20.2 18.4 16.9 15.7 14.6 13.7 5.9 S.S 10.0 IRIR 3.3 12.9 12.0 11.1 15.0 13.9 12.9 12.1 9.3 19.6 75 3.1 5.1 8.7 9 10 61.6 46. SON 548 39.7 43.2 46.7 31.4 34.5 37.6 40.6 27.7 30.5 33.2 35.9 24.8 27.3 29.8 32.2 22.5 24.7 27.0 29.2 20.5 22.6 24.6 26.7 18.9 20.8 22.7 24.6 17.5 19.3 21.0 22.8 16.3 18.0 21.2 15.2 16.8 18.3 19.8 14.3 15.8 17.2 18.7 12.8 14.1 15.4 16.7 11.5 12.7 13.9 15.0 9.3 10.2 11.2 12.1 7.8 8.6 9.4 10.1 5.9 7.1 7.6 3.9 4.3 4.7 5.1 3.0 3.3 3.6 3.9 2.4 2.6 2.9 3.1 80 10.4 2.9 4.8 8.2 11.3 12.8 90 7.0 6.6 5.9 5.3 2.6 4.3 7.3 9.8 8.7 7.9 10.1 100 2.3 3.9 6.6 9.1 125 11.5 10.3 8.3 7.0 1.9 3.1 5.3 6.3 7.3 150 4.3 3.6 1.6 2.6 4.4 5.3 6.1 6.5 200 1.2 2.0 2.7 3.4 4.0 4.6 5.3 300 0.8 1.3 1.8 2.3 2 2.7 3.1 3.5 400 0.6 1.0 2.7 1.4 1.7 2.0 2.4 500 0.8 2.1 1.4 1.6 1.9 + 0.5 1.1 ULDR exceeds 20 percent. Source: American Institute of Certified Public Accountants. "Audit Sampling", Audit and Accounting Guide (New York: AICPA, 2008) Note: This table presents ULDRs as percentages and assumes a large population, TABLE 4 Hornung, CPA, is performing an attributes sampling plan for her audit of Packers Company. In her audit of cash disbursements, she has identified the preparation of a voucher and marking it as "PAID" prior to preparing and mailing a check to the vendor as an important control. In performing her sampling application, she established the following parameters. HORNUNG, CPA PARAMETERS FOR ATTRIBUTES SAMPLING PLAN FOR PACKERS COMPANY Risk of overreliance Expected population deviation rate Tolerable deviation rate 5.00% 3.00% 7.00% REQUIRED: (1) (2) (3) (4) (6) (7) Define the objective of this audit test. Define the population that will be used for purposes of this audit test. Define the sampling unit that will be used for purposes of this audit test. Define what will constitute a deviation for purposes of this audit test. Determine the sample size using the appropriate table from those attached. Based on your results from (5) above and assuming the auditor found four deviations, determine the sample rate of deviation Based on your previous results, still assuming the auditor found four deviations, and using the appropriate table from those attached, determine the upper limit on the deviation rate. Use linear interpolation on the table if necessary to arrive at a reasonably precise value for the rate: What would Hornung's conclusion be with respect to the audit test performed? Explain in terms that you would use in the audit working papers to document your conclusion, (8) 20 PE sor 61 26 0 19 46 22 30 22 SI 10 9F BO 22 OFERING CONTROL RISK TOO LOW SAMPLE SEE TABLE FOR S PERCENT RISK P. Rate 16 30 51 $1 97 OL 22 22 SF S 97 30 SI 16 46 31 31 30 30 30 36 9 22 22 12 39 61 CH 77 77 77 30 99 61 22 57 30 68 127 THE 22 61 77 68 30 100 $ 61 22 ME 84 30 ES 19 333 I 18 40 22 22 72 . 76 M AT . 40 195 23 20 109 05 129 95 145 112 167 112 185 146 84 100 76 1. 22 40 89 341 100 30 377 40 221 . 21 293 116 158 1.345 30 . 240 . 478 50 UT 179 2.5D . . TES 266 585 1,832 37 89 . 298 . . . 6.00 TO 37 85 . . 649 . . . . . . 110 44 . . . 006 . 150 50 10.00 . . . . . . 576 . . . . . 88 12.50 193 15.00 17.50 720 Sample size is too large so be cost effective for most odit applications Ser American Institute of Certified Public Accountants, "Audit Sampling". Audit and Accounting Guide (New York: . Nice AICPA, 2008) This table assumes a large population Sample sizes greater than 2,000 not shown TABLE 1 SAMPLE SIZE TABLE VOR 10 PERCENT RISK OF ASSESSING CONTROL RISK TOO LOW orale talartlantats Expected Deviation Rate 0.00% 0.25 0.50 25 114 76 129 7 129 0.75 194 194 265 398 57 96 96 56 96 129 20 25 1.00 06 22 15 45 77 77 72 77 77 105 55 SIE 11 IN 1.25 176 221 64 SS 3 48 G 708 1.463 /// 25 1.50 1.75 55 265 66 25 42 1 55 . 06 390 45 132 132 166 198 262 DIE 42 55 105 33 TR 16 2.00 2.25 590 42 55 25 25 25 25 48 B SN 38 IN 974 42 75 2.50 88 353 75 35 132 132 158 209 258 IN 18 65 25 2.75 110 42 38 65 25 SX 18 3.00 . 3 471 730 1.258 132 132 75 94 94 113 65 18 58 52 E 3.25 3.50 25 25 25 65 82 306 58 58 18 18 . 400 153 194 235 52 52 52 the Nex 113 82 3.75 18 73 583 131 25 25 25 98 18 4.00 73 873 52 274 149 98 18 5.00 73 65 1,019 25 318 160 115 6.00 . 34 1.150 349 182 78 116 18 18 25 25 7.00 43 . 1,300 385 52 8.00 + . . 1,437 199 424 1.577 8/3/3/9/*/ 25 9.00 + . . . 77 32 10.00 100 38 12.50 368 63 15.00 . 126 17.50 457 Sample size is too large to be cost effective for most audit applications. Source: American Institute of Certified Public Accountants, "Audit Sampling". Audit and Accounting Guide (New York: AICPA, 2008) Note: This table assumes a large population. Sample sizes greater than 2,000 not shown TABLE 2 10 9 $ 65.4 69.9 58.4 59 deal Namber of Deviations Found SAMPLE EVALUATION TABLE FOR S PERCENT RISK OF ASSESSING CONTROL RISK TOO LOW 54.4 46.6 40.6 36.0 Namysle 2 50.0 43.7 38.8 34.8 31.6 28.9 26.7 30 25 10 15 1.6 8 28 14.4 282 282 219 207 183 213 16.4 19.2 7 6 5 . 60,7 1022 50.8 56 50.4 -16.3 37.6 TO 12.0 280 43.0 15.8 319 39.4 243 27.8 31.1 14.4 37.5 24.6 275 30.4 33.3 24.7 27.3 29.8 22.4 24.7 27.1 182 205 24.8 18.8 20.8 32.4 29.4 26.9 24.8 23.0 220 40 73 0.5 19.9 22.6 15 22.8 24.7 SO 1 14.0 27,7 195 149 19.6 12.9 17.0 114 15.0 10.2 134 9.2 12.1 11.1 10.2 9.4 11.5 8.8 10.8 10.1 9.5 15.9 21.2 28.1 55 5.9 5.4 4.9 21.4 8.4 19.3 19.7 21.6 00 180 20.1 65 4.6 14.8 17.4 13.5 12.5 14.7 13.6 12.7 11.8 12.7 168 15.5 14.5 13.6 7.7 7.1 6.6 18.5 17.5 16,3 15.2 20.3 16.9 18.9 70 4.2 17.4 15.9 16.9 6.2 14.3 18.2 16.4 75 80 90 15.5 8.2 7.7 14,2 11.1 9.9 12.8 15.2 11.4 4.0 3.7 3.3 3.0 2.4 14.0 5.8 5.2 4.7 6.9 8.4 12.8 13.2 11.5 12.3 10.3 11.3 9.0 100 125 6.2 7.6 10.3 9.3 11.1 10.3 8.3 3.8 5.0 6.1 7.2 9.5 8.6 150 7.8 2.0 8.4 3.2 7.8 5.1 6.9 6.0 7.2 200 4.2 3.2 6.5 1.5 2.4 5.8 3 4.6 3.9 5.2 5.6 5.2 N 4.8 300 4.4 1.0 1.6 1 4.0 2.1 2.6 3.1 3.5 3.9 4.3 400 0.8 3.6 1.2 3.3 1.6 2.0 2.3 2.7 3.0 2.4 3.2 3.4 2.9 500 0.6 1.0 ULDR exceeds 20 percent 1.3 1.6 1.9 2.7 2.1 Source: American Institute of Certified Public Accountants, "Audit Sampling", Audit and Accounting Guide (New Note: York: AICPA, 2008) This table presents ULDRs as percentages and assumes a large population. TABLE 3 SAMPLE EVALUATION TABLE FOR 10 PERCENT RISK OF ASSESSING CONTROL RISK TOO LOW Actual Number of Deviations Found Sample Size 20 25 30 35 1 0 10.9 18.1 4 4 8.8 14.7 6 7.4 463 36.1 29.5 24.9 12.4 10.7 56.5 7 51.9 426 6.4 5 415 140 28. 24.9 38.4 40 5.6 36.2 21.6 32.5 28.2 45 P 2 3 24.5 30.5 20.0 24.9 16.8 21.0 14.5 18.2 12.8 16.0 11.4 14.3 10.3 12.9 9.4 11.8 8.7 10.8 8.0 7.5 5.0 4.6 8.4 SO 249 7.6 SS 19.0 17.0 15.4 14.1 4.2 22.0 19.7 17.8 16.3 6.9 60 3.8 6.4 65 3.5 70 223 20.2 18.4 16.9 15.7 14.6 13.7 5.9 S.S 10.0 IRIR 3.3 12.9 12.0 11.1 15.0 13.9 12.9 12.1 9.3 19.6 75 3.1 5.1 8.7 9 10 61.6 46. SON 548 39.7 43.2 46.7 31.4 34.5 37.6 40.6 27.7 30.5 33.2 35.9 24.8 27.3 29.8 32.2 22.5 24.7 27.0 29.2 20.5 22.6 24.6 26.7 18.9 20.8 22.7 24.6 17.5 19.3 21.0 22.8 16.3 18.0 21.2 15.2 16.8 18.3 19.8 14.3 15.8 17.2 18.7 12.8 14.1 15.4 16.7 11.5 12.7 13.9 15.0 9.3 10.2 11.2 12.1 7.8 8.6 9.4 10.1 5.9 7.1 7.6 3.9 4.3 4.7 5.1 3.0 3.3 3.6 3.9 2.4 2.6 2.9 3.1 80 10.4 2.9 4.8 8.2 11.3 12.8 90 7.0 6.6 5.9 5.3 2.6 4.3 7.3 9.8 8.7 7.9 10.1 100 2.3 3.9 6.6 9.1 125 11.5 10.3 8.3 7.0 1.9 3.1 5.3 6.3 7.3 150 4.3 3.6 1.6 2.6 4.4 5.3 6.1 6.5 200 1.2 2.0 2.7 3.4 4.0 4.6 5.3 300 0.8 1.3 1.8 2.3 2 2.7 3.1 3.5 400 0.6 1.0 2.7 1.4 1.7 2.0 2.4 500 0.8 2.1 1.4 1.6 1.9 + 0.5 1.1 ULDR exceeds 20 percent. Source: American Institute of Certified Public Accountants. "Audit Sampling", Audit and Accounting Guide (New York: AICPA, 2008) Note: This table presents ULDRs as percentages and assumes a large population, TABLE 4