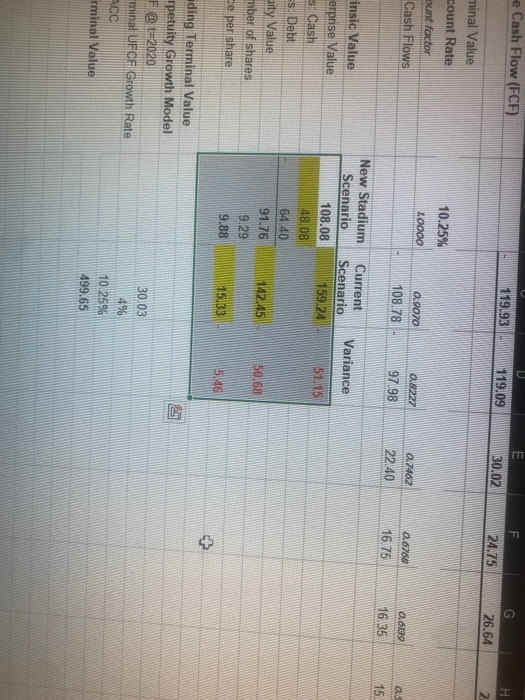

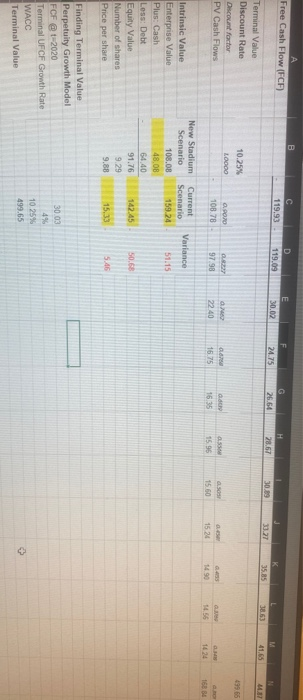

how did we get the yellow highlighted numbers?

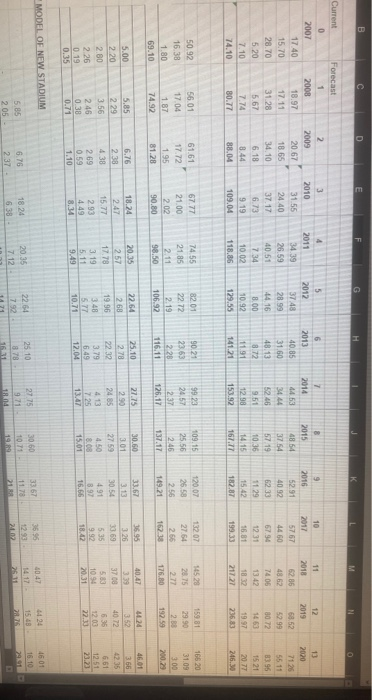

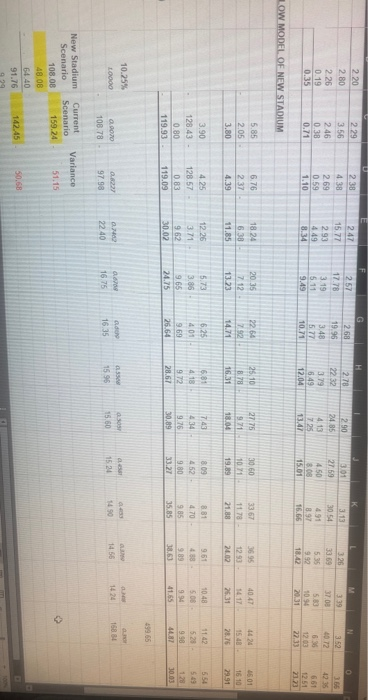

e Cash Flow (FCF) F 119.93 119.09 E 30.02 H 24.75 26.64 2 minal Value count Rate ount factor Cash Flows 10.25% LO000 0.9070 108.78 0.8227 97.98 0.7462 22.40 0.6708 16.75 0.809 16.35 0.5 15 Current Scenario 159.24 Variance 5115 insic Value erprise Value s. Oash Si Debt Jity Value mber of shares Se per share New Stadium Scenario 108.08 48.08 64.40 91.76 9.29 9.88 142.45 50168 15.33 5.46 + ading Terminal Value rpetuity Growth Model F@t-2020 minal UFCF Growth Rate rminal Value 30.03 4.9% 10.25% 499.65 c L 0 7 2014 4453 10 2017 2015 Current 0 2007 17.40 15.70 28.70 5.20 7.10 74.10 Forecast 1 2008 18.97 17.11 3123 5.67 7.74 80.77 2 2009 20 67 18 65 34.10 6.18 8.44 88.04 2010 31.55 24.40 37.17 6.73 9.19 109.04 2011 34 39 26.59 40.51 7.34 10.02 118.86 6 2013 40.85 31 60 48.13 8.72 11.91 141.21 2012 37 48 28.99 14 16 8.00 10.92 129.55 4460 9 2016 5291 An 5233 1129 15.42 182.87 11 2018 52 48.62 740 13.42 12 2019 68.52 52.99 8072 1463 1997 236.83 2000 7125 5511 8396 1521 20.77 246.90 9.51 12 153.92 10.36 14.15 167.17 12.31 16.31 199.33 217 21 50.92 61.61 17.72 NS 56.01 17.04 1.87 74.92 89 3 3 8 109.15 25.56 2.45 137.17 132 07 27.64 266 162.38 120.07 26.58 256 149.21 152 2975 27 1760 159.81 29 90 28 1.80 69.10 237 126,11 2.28 116.11 2002 81.28 106.92 40.47 46.01 31 27.75 290 2435 325 3369 37 00 5.85 2.29 3.50 2.46 0.30 0.71 5.00 2.20 2.80 2.26 0.19 0.35 18.24 247 15.77 2.93 6.76 2.39 4.38 269 0.59 1.10 25.10 278 2232 3.79 20.35 257 17.78 3.19 5.11 9.49 22.64 268 1996 343 577 10.71 30.60 301 2759 4.50 80 15.01 40.72 635 42.35 661 12.31 89 BS 104 2031 li 134 12.04 8.34 MODEL OF NEW STADIUM 2775 60 3367 424 15.43 1601 16.10 584 25 10 732378 16 BE M 2.20 2.80 2.26 0.19 0.35 2.29 3.56 2.46 0.38 0.71 2.38 4.38 2.69 0.59 1.10 2.47 15.77 2.93 4.49 8.34 F G 257 268 17.78 3.19 5.11 9.49 10.7 2.78 22.32 3.79 6.49 12.04 2.90 24.85 4.13 72 131 301 27.59 4.50 8.08 15.01 3.13 30 54 491 39 33 339 37.00 53 10.94 352 10.12 4235 63 66 1200 27.33 212 18.42 LOW MODEL OF NEW STADIUM 18.24 4047 88 6.76 2.37 419 20 35 7.12 13.23 25.10 8.78 16.31 27.75 971 10 30 60 10 1920 33 67 1178 21.88 36 95 12.50 2002 1501 16.10 29.91 15.48 28.75 11.85 26.31 524 1043 11.42 523 554 549 128.57 0.83 119.09 681 4.18 972 28.61 741 34 9.76 30.89 8.09 452 9.80 33.2 8181 470 GAS 35.85 951 439 OR 38.63 24.78 41.65 4087 30.03 19965 10.25% L0000 0.240 . 16.75 0.6221 97.98 AN 16.35 G.NO 22.40 30 15.50 a. 152 1684 1424 1456 159 1490 Variance 51.18 New Stadium Scenario 108.08 48.08 6440 B Free Cash Flow (FCF) C D 119.93.119.09 F 24.75 H 30.02 26.64 28.57 30.89 3327 K 35.85 38.63 M 41.65 Terminal Value Discount Rate Discount factor PV Cash Flows 10.25% 95 LOOOO O.RORO 108.78 97 98 22.40 16.75 16.35 a. 15.60 15.96 . 1524 14.90 14.56 1424 168 84 Variance Current Scenario 159.24 51.15 Intrinsic Value Enterprise Value Plus: Cash Less: Debt Equity Value Number of shares Price per share New Stadium Scenario 108.08 48.08 64.40 91.76 9.29 9.88 142.45 50.8 15.13 5.46 Finding Terminal Value Perpetuity Growth Model FCF @t-2020 Terminal UFCF Growth Rate WACC Terminal Value 30.03 4% 10.25% 499.65 e Cash Flow (FCF) F 119.93 119.09 E 30.02 H 24.75 26.64 2 minal Value count Rate ount factor Cash Flows 10.25% LO000 0.9070 108.78 0.8227 97.98 0.7462 22.40 0.6708 16.75 0.809 16.35 0.5 15 Current Scenario 159.24 Variance 5115 insic Value erprise Value s. Oash Si Debt Jity Value mber of shares Se per share New Stadium Scenario 108.08 48.08 64.40 91.76 9.29 9.88 142.45 50168 15.33 5.46 + ading Terminal Value rpetuity Growth Model F@t-2020 minal UFCF Growth Rate rminal Value 30.03 4.9% 10.25% 499.65 c L 0 7 2014 4453 10 2017 2015 Current 0 2007 17.40 15.70 28.70 5.20 7.10 74.10 Forecast 1 2008 18.97 17.11 3123 5.67 7.74 80.77 2 2009 20 67 18 65 34.10 6.18 8.44 88.04 2010 31.55 24.40 37.17 6.73 9.19 109.04 2011 34 39 26.59 40.51 7.34 10.02 118.86 6 2013 40.85 31 60 48.13 8.72 11.91 141.21 2012 37 48 28.99 14 16 8.00 10.92 129.55 4460 9 2016 5291 An 5233 1129 15.42 182.87 11 2018 52 48.62 740 13.42 12 2019 68.52 52.99 8072 1463 1997 236.83 2000 7125 5511 8396 1521 20.77 246.90 9.51 12 153.92 10.36 14.15 167.17 12.31 16.31 199.33 217 21 50.92 61.61 17.72 NS 56.01 17.04 1.87 74.92 89 3 3 8 109.15 25.56 2.45 137.17 132 07 27.64 266 162.38 120.07 26.58 256 149.21 152 2975 27 1760 159.81 29 90 28 1.80 69.10 237 126,11 2.28 116.11 2002 81.28 106.92 40.47 46.01 31 27.75 290 2435 325 3369 37 00 5.85 2.29 3.50 2.46 0.30 0.71 5.00 2.20 2.80 2.26 0.19 0.35 18.24 247 15.77 2.93 6.76 2.39 4.38 269 0.59 1.10 25.10 278 2232 3.79 20.35 257 17.78 3.19 5.11 9.49 22.64 268 1996 343 577 10.71 30.60 301 2759 4.50 80 15.01 40.72 635 42.35 661 12.31 89 BS 104 2031 li 134 12.04 8.34 MODEL OF NEW STADIUM 2775 60 3367 424 15.43 1601 16.10 584 25 10 732378 16 BE M 2.20 2.80 2.26 0.19 0.35 2.29 3.56 2.46 0.38 0.71 2.38 4.38 2.69 0.59 1.10 2.47 15.77 2.93 4.49 8.34 F G 257 268 17.78 3.19 5.11 9.49 10.7 2.78 22.32 3.79 6.49 12.04 2.90 24.85 4.13 72 131 301 27.59 4.50 8.08 15.01 3.13 30 54 491 39 33 339 37.00 53 10.94 352 10.12 4235 63 66 1200 27.33 212 18.42 LOW MODEL OF NEW STADIUM 18.24 4047 88 6.76 2.37 419 20 35 7.12 13.23 25.10 8.78 16.31 27.75 971 10 30 60 10 1920 33 67 1178 21.88 36 95 12.50 2002 1501 16.10 29.91 15.48 28.75 11.85 26.31 524 1043 11.42 523 554 549 128.57 0.83 119.09 681 4.18 972 28.61 741 34 9.76 30.89 8.09 452 9.80 33.2 8181 470 GAS 35.85 951 439 OR 38.63 24.78 41.65 4087 30.03 19965 10.25% L0000 0.240 . 16.75 0.6221 97.98 AN 16.35 G.NO 22.40 30 15.50 a. 152 1684 1424 1456 159 1490 Variance 51.18 New Stadium Scenario 108.08 48.08 6440 B Free Cash Flow (FCF) C D 119.93.119.09 F 24.75 H 30.02 26.64 28.57 30.89 3327 K 35.85 38.63 M 41.65 Terminal Value Discount Rate Discount factor PV Cash Flows 10.25% 95 LOOOO O.RORO 108.78 97 98 22.40 16.75 16.35 a. 15.60 15.96 . 1524 14.90 14.56 1424 168 84 Variance Current Scenario 159.24 51.15 Intrinsic Value Enterprise Value Plus: Cash Less: Debt Equity Value Number of shares Price per share New Stadium Scenario 108.08 48.08 64.40 91.76 9.29 9.88 142.45 50.8 15.13 5.46 Finding Terminal Value Perpetuity Growth Model FCF @t-2020 Terminal UFCF Growth Rate WACC Terminal Value 30.03 4% 10.25% 499.65