how do i do question 10 using the data from above?

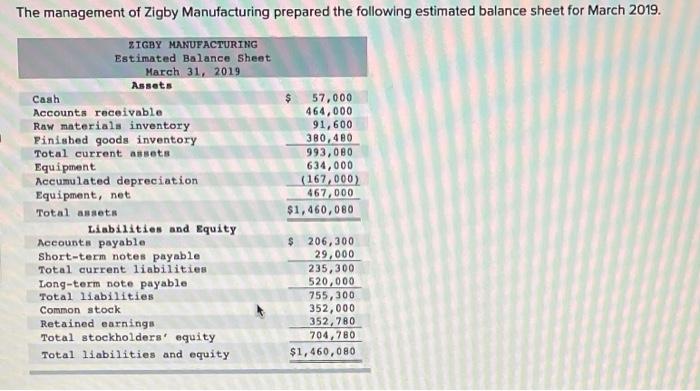

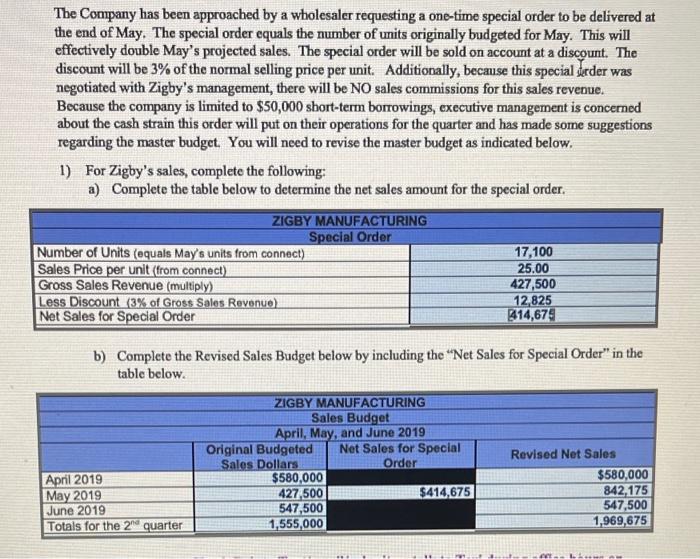

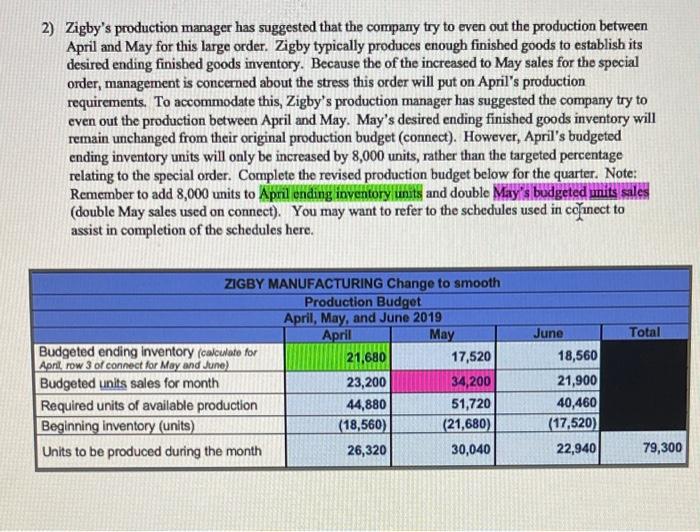

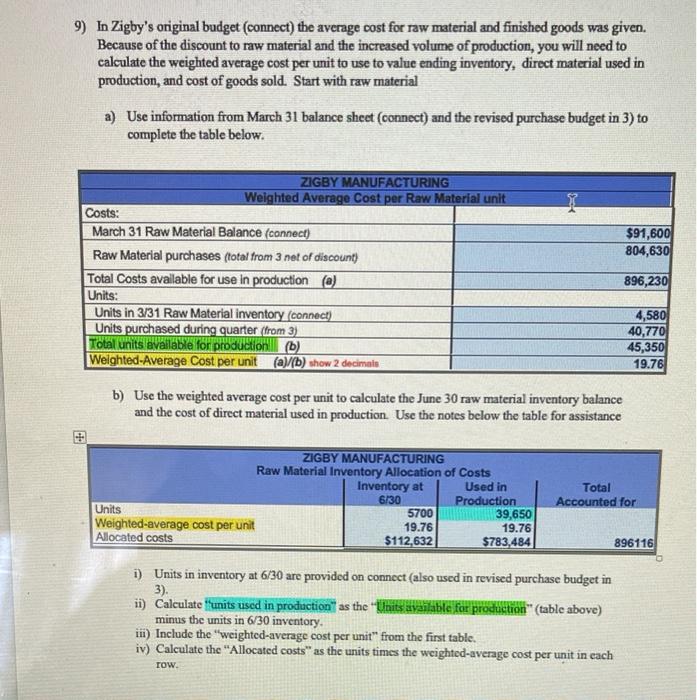

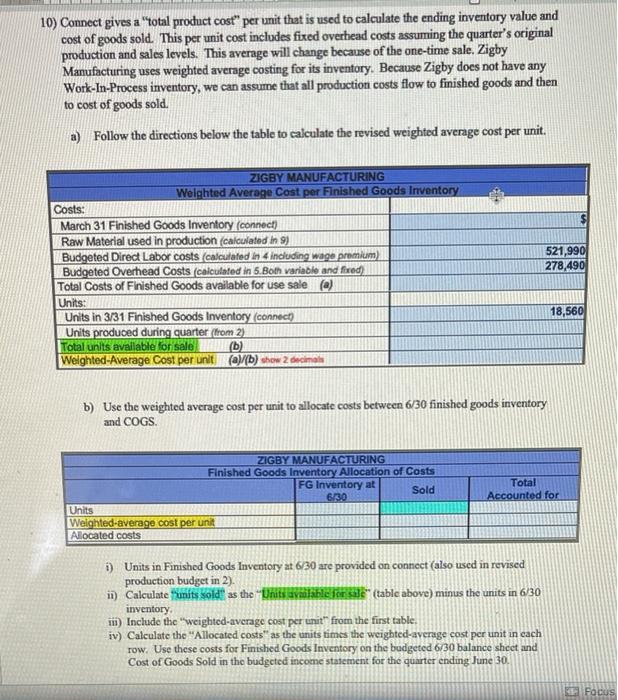

The management of Zigby Manufacturing prepared the following estimated balance sheet for March 2019. ZIGBY MANUFACTURING Estimated Balance Sheet March 31, 2019 Assets Cash 57,000 Accounts receivable 464,000 Raw materials inventory 91,600 Finished goods inventory 380,480 Total current assets 993,080 Equipment 634,000 Accumulated depreciation (167,000) Equipment, net 467,000 Total assets $1,460,080 Liabilities and Equity Accounts payable $ 206,300 Short-term notes payable 29,000 Total current liabilities 235,300 Long-term note payable 520,000 Total liabilities 755,300 Common stock 352,000 Retained earnings 352, 780 Total stockholders' equity 704,780 Total liabilities and equity $1,460,080 To prepare a master budget for April, May, and June of 2019, management gathers the following information a. Sales for March total 23,200 units. Forecasted sales in units are as follows: April, 23,200; May, 17,100; June, 21,900; and July, 23,200. Sales of 257,000 units are forecasted for the entire year. The product's selling price is $25.00 per unit and its total product cost is $20.50 per unit b. Company policy calls for a given month's ending raw materials inventory to equal 50% of the next month's materials requirements. The March 31 raw materials inventory is 4,580 units, which complies with the policy. The expected June 30 ending raw materials Inventory is 5,700 units. Raw materials cost $20 per unit. Each finished unit requires 0.50 units of raw materials. c. Company policy calls for a given month's ending finished goods inventory to equal 80% of the next month's expected unit sales The March 31 finished goods inventory is 18,560 units, which complies with the policy. d. Each finished unit requires 0.50 hours of direct labor ata rate of $13 per hour. e Overhead is allocated based on direct labor hours. The predetermined variable overhead rate is $4.40 per direct labor hour Depreciation of $37,320 per month is treated as fixed factory overhead 1. Sales representatives' commissions are 5% of sales and are paid in the month of the sales. The sales manager's monthly salary is $4,700 9. Monthly general and administrative expenses include $29,000 administrative salaries and 0.8% monthly interest on the long-term h. The company expects 20% of sales to be for cash and the remaining 80% on credit. Receivables are collected in full in the month following the sale (none are collected in the month of the sale) 1. All raw materials purchases are on credit, and no payables arise from any other transactions. One month's raw materials purchases are fully paid in the next month. J. The minimum ending cash balance for all months is $99,000. If necessary, the company borrows enough cash using a short-term note to reach the minimum. Short-term notes require an interest payment of 1% at each month-end (before any repayment). If the ending cash balance exceeds the minimum, the excess will be applied to repaying the short-term notes payable balance. k. Dividends of $27,000 are to be declared and paid in May. 1. No cash payments for income taxes are to be made during the second calendar quarter Income tax will be assessed at 40% in the quarter and paid in the third calendar quarter. m. Equipment purchases of $147,000 are budgeted for the last day of June. The Company has been approached by a wholesaler requesting a one-time special order to be delivered at the end of May. The special order equals the number of units originally budgeted for May. This will effectively double May's projected sales. The special order will be sold on account at a discount. The discount will be 3% of the normal selling price per unit. Additionally, because this special serder was negotiated with Zigby's management, there will be NO sales commissions for this sales revenue. Because the company is limited to $50,000 short-term borrowings, executive management is concerned about the cash strain this order will put on their operations for the quarter and has made some suggestions regarding the master budget. You will need to revise the master budget as indicated below, 1) For Zigby's sales, complete the following: a) Complete the table below to determine the net sales amount for the special order. ZIGBY MANUFACTURING Special Order Number of Units (equals May's units from connect) 17,100 Sales Price per unit (from connect) 25.00 Gross Sales Revenue (multiply) 427,500 Less Discount (3% of Gross Sales Revenue) 12,825 Net Sales for Special Order 14,675 b) Complete the Revised Sales Budget below by including the Net Sales for Special Order" in the table below. ZIGBY MANUFACTURING Sales Budget April, May, and June 2019 Original Budgeted Net Sales for Special Revised Net Sales Sales Dollars Order April 2019 $580,000 $580,000 May 2019 427,500 $414,675 842,175 June 2019 547,500 547,500 Totals for the 2 quarter 1,555,000 1,969,675 - LE 2) Zigby's production manager has suggested that the company try to even out the production between April and May for this large order. Zigby typically produces enough finished goods to establish its desired ending finished goods inventory. Because the of the increased to May sales for the special order, management is concerned about the stress this order will put on April's production requirements. To accommodate this, Zigby's production manager has suggested the company try to even out the production between April and May. May's desired ending finished goods inventory will remain unchanged from their original production budget (connect). However, April's budgeted ending inventory units will only be increased by 8,000 units, rather than the targeted percentage relating to the special order. Complete the revised production budget below for the quarter. Note: Remember to add 8,000 units to April ending inventory units and double May's budgeted units sales (double May sales used on connect). You may want to refer to the schedules used in coinect to assist in completion of the schedules here. Total ZIGBY MANUFACTURING Change to smooth Production Budget April, May, and June 2019 April May Budgeted ending inventory (calculate for 21.680 17,520 April, row 3 of connect for May and June) Budgeted units sales for month 23,200 34,200 Required units of available production 44,880 51,720 Beginning inventory (units) (18,560) (21,680) Units to be produced during the month 26,320 30,040 June 18,560 21,900 40,460 (17,520) 22,940 79,300 3) To conserve cash, the purchasing manager has asked to reduce April and May's ending raw materials inventory to equal 30% (down from 50%) of next month's materials requirements. June ending raw materials inventory will remain unchanged (same as on connect). Note - This % changes the calculation of required ENDING INVENTORY of raw material (row 4 of the table) and DOES NOT change the raw material required per unit of production (row 2). This table is completed similarly to the budget table in connect. Additionally, the purchase department has negotiated a 5% discount on raw material if they purchases exceed 10,000 pounds in any given month. The 5% will be only for the pounds purchased over 10,000. (Pounds of material purchased - 10,000 pounds x S20 per pound x 5% Calculate the Discount for each month and calculate the "net" purchase amount. I Project 4: Page 2 of 11 .50 .50 ZIGBY MANUFACTURING Revised Raw Materials Budget April May June Total Production budget (units) 26,320 30,040 22,940 Materials requirements per unit .50 unchanged from connect) Materials needed for production 13,160 15,020 11,470 Budgeted ending inventory 4,506 3,441 5,700 Total materials requirements (units) 17,666 18,461 17,170 Beginning inventory (4,580) (4,506) R(3.441) Materials to be purchased 13,086 13,955 13,72940,770 Material price per unit $20.00 $20.00 $20.00 $20.00 Raw Material purchases before $261,720 $279,100 $274,580 $815,400 Discount Discount (5% of purchases exceeding $3,086 $3,955 $3,729 $10,770.00 10,000 lbs) Budgeted raw material purchases $258,634 $275,145 $270,851 $804,630 4) To maintain moral among their employees, Zigby has agreed to pay employees a wage premium of $3 an bour for excess overtime. Excess overtime has been defined as any hours in excess of 13,000 bours in a month. The Direct Labor Budget will need to be updated for the changes to the production budget and the wage premium added for each month. This table is completed similarly to the budget table in connect Total Budgeted production (units) Labor requirements per unit (hours) Total labor hours needed Direct labor rate (per hour) Base direct labor cost Wage premium (3xhours over 13.000) Total Budgeted direct labor costs ZIGBY MANUFACTURING Revised Direct Labor Budget April May 26,320 30,040 .50 .50 13,160 15,020 13 13 171,080 195,260 480 6,060 171,560 201,320 June 22,940 .50 11,475 13 149, 110 0 149,110 521,990 5) Factory Overhead Budget will need to be updated for the production and labor requirement changes. This table is completed similarly to the budget table in connect. Total Labor hours needed Variable factory overhead rate Budgeted variable overhead Budgeted fixed overhead Budgeted total overhead ZIGBY MANUFACTURING Revised Factory Overhead Budget April May 13,160 15,020 4.20 4.20 55, 272 63,084 37,320 37,320 92,592 100,404 June 11,470 4.20 48,174 37,320 85,494 166,530 111,960 278,490 6) The special order will be on account and the customer is not expected to pay until June. Zigby's management plans to compensate by intensifying collections efforts on their other customers by sending bills out sooner. Management feels these efforts will result in collection of 20% of the credit sales in the month of sale. (This will be in addition to the cash sales for the month). The remainder of credit sales will be collected in the subsequent month. All of March 31 receivables are expected to be collected in April. May special order is expected to be collected in June. Complete the tables below to revise the estimate of credit sales. The one-time sale is considered credit ZIGBY MANUFACTURING Revised Cash Receipts from Customers April May June Current month's cash sales (from connect) 116,000 85,500 109,500 Current month's credit sales collected 92,800 68,400 87,600 (20% of current months credit sales) Previous month's credit sales collected 464,000 371,200 273,600 (80% of previous months sales) Special order collected in June 414,675 Total cash receipts 672,800 525,100 885,375 7) Additionally, to conserve cash, the company has decided to delay payment for their raw material purchases. The company previously paid 100% of their raw material purchases (revised budget in 3) in the month after the purchase was made. Starting with March purchases (Accounts Payable balance at 3/31), Zigby plans to only pay 80% of their purchases in the first month after the purchases are made. The remaining 20% will be paid in the second month after purchase (Example: 80% of accounts payable on March 31 will be paid in April and the remaining 20% will be paid in May. April sales will be paid in May and June, etc.) Remember: Purchases budgeted in 3 increased accounts payable (credit) while estimated payments here decreases accounts payable (debit). ZIGBY MANUFACTURING Estimated Payments for Raw Material Purchases June 30 Accounts April May June Payable March 31 Accounts Payable 165,040 41,260 April purchases 206,907 51,727 May Purchases 220,116 55,029 June Purchases 270,851 Total cash payments 165,040 248,167 271,843 325,880 8) Using the revised budgets, complete the revised cash budget. Remember, Zigby Manufacturing will need to maintain the indicated minimum cash balance (given on connect) at the end of each month. Outstanding short-term notes require an interest payment of 1% at each month-end (before any repayment). Repayments of short-term notes payable balance will be made only to the extend the ending cash balance exceeds the minimum required. This table is completed similarly to the budget table in connect. Z May June 256,746 200,056 525,100 885,375 781,8461,085,431 ZIGBY MANUFACTURING Revised Cash Budget April Beginning cash balance 57,000 Cash receipts from customers 672,800 Total cash available 729,800 Cash payments for: Raw materials 165,040 Direct labor 171,560 Variable overhead 40,304 Sales commissions 29,000 Sales salaries 4,700 General & administrative salaries 29,000 Dividends Loan interest 290 Long-term note interest 4,160 Purchases of equipment Total cash payments 444,054 Preliminary cash balance 285,746) Additional loan (loan repayment) (29,000) Ending cash balance 256 746 248,167 201,320 46,068 21,375 4,700 29,000 27,000 0 4,160 271,843 149.110 50,468 27,375 4,700 29,000 581,790 200,056 0 200,056 4160 147,000 683,656 401,775 0 401,775 June Revised Loan balance: ST note payable April May Loan balance - Beginning of month 29,000 Additional loan (loan repayment) (29,000) Loan balance - End of month 0 OOO ololo 9) In Zigby's original budget (connect) the average cost for raw material and finished goods was given. Because of the discount to raw material and the increased volume of production, you will need to calculate the weighted average cost per unit to use to value ending inventory, direct material used in production, and cost of goods sold. Start with raw material a) Use information from March 31 balance sheet (connect) and the revised purchase budget in 3) to complete the table below. I $91,600 804,630 ZIGBY MANUFACTURING Weighted Average Cost per Raw Material unit Costs: March 31 Raw Material Balance (connect) Raw Material purchases (total from 3 net of discount) Total Costs available for use in production (@) Units: Units in 3/31 Raw Material inventory (connect) Units purchased during quarter (from 3) Total units available for production (b) Weighted Average Cost per unit (a) (b) show 2 decimals 896,230 4,580 40,770 45,350 19.76 b) Use the weighted average cost per unit to calculate the June 30 raw material inventory balance and the cost of direct material used in production. Use the notes below the table for assistance ZIGBY MANUFACTURING Raw Material Inventory Allocation of Costs Inventory at Used in Production Units 5700 39,650 Weighted average cost per unit 19.76 19.76 Allocated costs $112,632 $783,484 6/30 Total Accounted for 896116 1) Units in inventory at 6/30 are provided on connect (also used in revised purchase budget in 3). ii) Calculate units used in production as the "Units available for production (table above) minus the units in 6/30 inventory. ii) Include the "weighted average cost per unit from the first table. iv) Calculate the "Allocated costs" as the units times the weighted average cost per unit in cach row 10) Connect gives a total product cost" per unit that is used to calculate the ending inventory value and cost of goods sold. This per unit cost includes fixed overhead costs assuming the quarter's original production and sales levels. This average will change because of the one-time sale. Zigby Manufacturing uses weighted average costing for its inventory. Because Zigby does not have any Work-In-Process inventory, we can assume that all production costs flow to finished goods and then to cost of goods sold. a) Follow the directions below the table to calculate the revised weighted average cost per unit. GH ZIGBY MANUFACTURING Weighted Average Cost per Finished Goods Inventory Costs: March 31 Finished Goods Inventory (connect) Raw Material used in production (calculated in 9) Budgeted Direct Labor costs calculated in 4 including wage premium) Budgeted Overhead Costs (calculated in 5. Both variable and fixed) Total Costs of Finished Goods available for use sale ) Units: Units in 3/31 Finished Goods Inventory connect) Units produced during quarter (from 2) Total units available for sale (b) Welghted Average Cost per unit (a)(b) show 2 decimal 521,990 278,490 18,560 b) Use the weighted average cost per unit to allocate costs between 6/30 finished goods inventory and COGS ZIGBY MANUFACTURING Finished Goods Inventory Allocation of Costs FG Inventory at Sold 6130 Units Weighted average cost per unit Alocated costs Total Accounted for 1) Units in Finished Goods Inventory at 6/30 are provided on connect (also used in revised production budget in 2). ii) Calculate units sold as the Units available for sale (table above) minus the units in 6/30 inventory. in Include the "weighted average cost per unit from the first table. iv) Calculate the "Allocated costs" as the units times the weighted average cost per unit in each row. Use these costs for Finished Goods Inventory on the budgeted 6/30 balance sheet and Cost of Goods Sold in the budgeted income statement for the quarter ending June 30. FOCUS