how to explain to the client based on the question

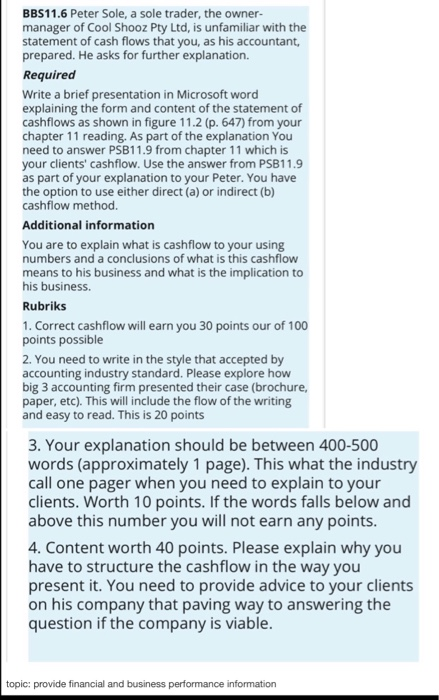

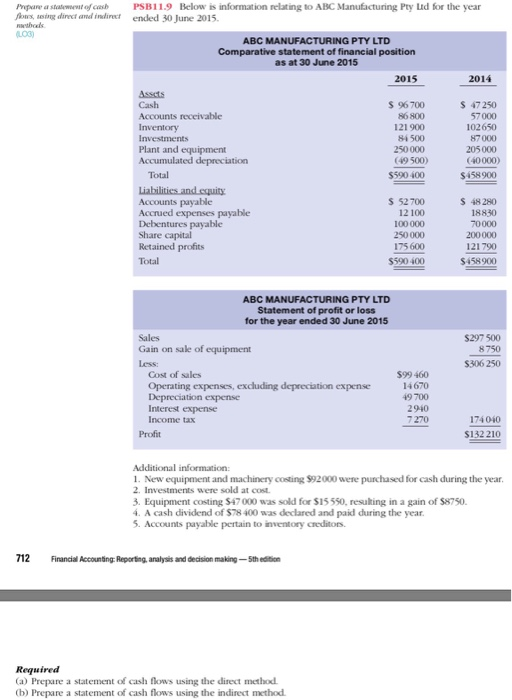

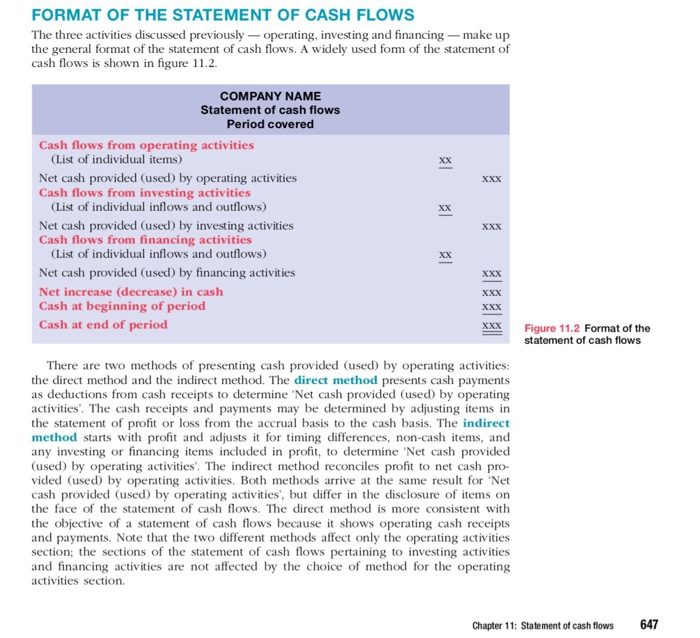

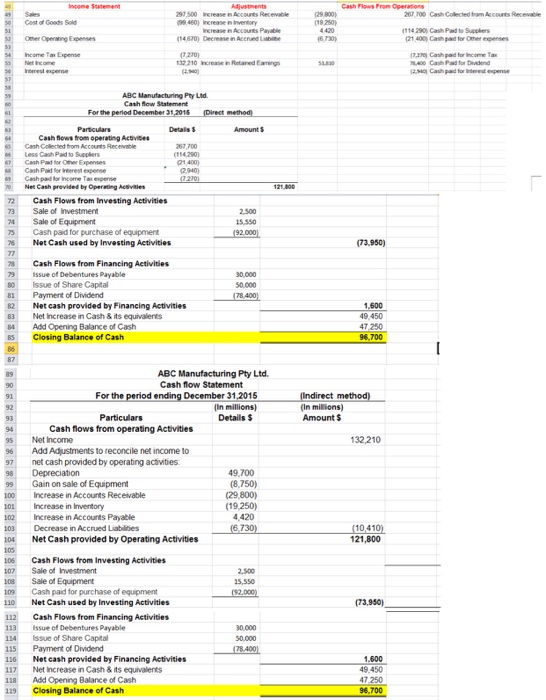

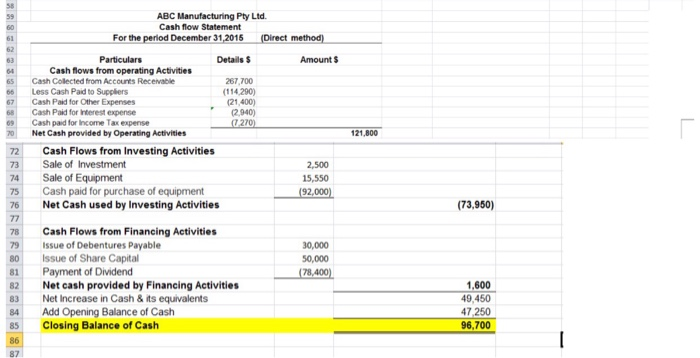

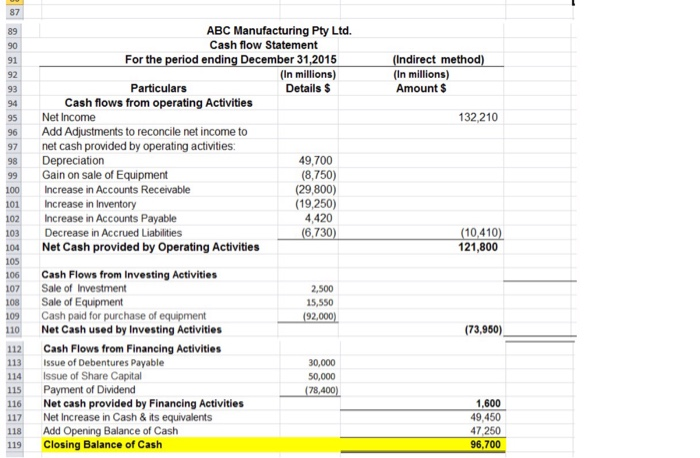

BBS11.6 Peter Sole, a sole trader, the owner- manager of Cool Shooz Pty Ltd, is unfamiliar with the statement of cash flows that you, as his accountant, prepared. He asks for further explanation. Required Write a brief presentation in Microsoft word explaining the form and content of the statement of cashflows as shown in figure 11.2 (p. 647) from your chapter 11 reading. As part of the explanation You need to answer PSB11.9 from chapter 11 which is your clients' cashflow. Use the answer from PSB11.9 as part of your explanation to your Peter. You have the option to use either direct (a) or indirect (b) cashflow method. Additional information You are to explain what is cashflow to your using numbers and a conclusions of what is this cashflow means to his business and what is the implication to his business. Rubriks 1. Correct cashflow will earn you 30 points our of 100 points possible 2. You need to write in the style that accepted by accounting industry standard. Please explore how big 3 accounting firm presented their case (brochure paper, etc). This will include the flow of the writing and easy to read. This is 20 points 3. Your explanation should be between 400-500 words (approximately 1 page). This what the industry call one pager when you need to explain to your clients. Worth 10 points. If the words falls below and above this number you will not earn any points. 4. Content worth 40 points. Please explain why you have to structure the cashflow in the way you present it. You need to provide advice to your clients on his company that paving way to answering the question if the company is viable. topic: provide financial and business performance information PSB11.9 Below is information relating to ABC Manufacturing Pty Ltd for the year ended 30 June 2015 Prpare a stateent of cash- fows, sing dinect and indirect wwthods (LO3) ABC MANUFACTURING PTY LTD Comparative statement of finaneial position as at 30 June 2015 2015 2014 Assets Cash $ 96700 S 47250 Accounts receivable Inventory Investments 86800 57000 121 900 102650 84500 87000 Plant and equipment Accumulated depreciation 250000 205000 (49500) (40000) Total $590 400 $458 900 Liabilitics and equity Accounts payable Accrued expenses payable Debentures payable Share capital Retained profits S 52700 S 48 280 18830 70000 12 100 100 000 250000 200000 175 600 121790 Total $590 400 $458900 ABC MANUFACTURING PTY LTD Statement of profit or loss for the year ended 30 June 2015 Sales Gain on sale of equipment Less $297 500 8750 $306 250 Cost of sales $99 460 14670 Operating expenses, excluding depreciation expense Depreciation expense Interest expense Income tax 49700 2940 7 270 174040 Profit $132 210 Additional information: 1. New equipment and machinery costing $92000 were purchased for cash during the year. 2. Investments were sold at cost 3. Equipment costing $47000 was sold for $15 550, resuking in a gain of $8750. 4. A cash dividend of $78 400 was declared and paid during the year. 5. Accounts payable pertain to inventory creditors. 712 Financial Accounting: Reporting, analysis and decision making-5th edition Required (a) Prepare a statement of cash flows using the direct method (b) Prepare a statement of cash flows using the indirect method. FORMAT OF THE STATEMENT OF CASH FLOWS The three activities discussed previously-operating, investing and financing -make up the general format of the statement of cash flows. A widely used form of the statement of cash flows is shown in figure 11.2 COMPANY NAME Statement of cash flows Period covered Cash flows from operating activities (List of individual items) xx Net cash provided (used) by operating activities Cash flows from investing activities (List of individual inflows and outflows) XXX Xx Net cash provided (used) by investing activities Cash flows from financing activities (List of individual inflows and outflows) Net cash provided (used) by financing activities Xxx XX XXx Net increase (decrease) in cash Cash at beginning of period Cash at end of period Xxx Figure 11.2 Format of the statement of cash flows Xxx There are two methods of presenting cash provided (used) by operating activities: the direct method and the indirect method. The direct method presents cash payments as deductions from cash receipts to determine 'Net cash provided (used) by operating activities. The cash receipts and payments may be determined by adjusting items in the statement of profit or loss from the accrual basis to the cash basis. The indirect method starts with profit and adjusts it for timing differences, non-cash items, and any investing or financing items included in profit, to determine 'Net cash provided (used) by operating activities. The indirect method recconciles profit to net cash pro- vided (used) by operating activities. Both methods arrive at the same result for Net cash provided (used) by operating activities, but differ in the disclosure of items on the face of the statement of cash flows. The direct method is more consistent with the objective of a statement of cash flows because it shows operating cash receipts and payments. Note that the two different methods affect only the operating activities section; the sections of the statement of cash flows pertaining to investing activities and financing activities are not affected by the choice of method for the operating activities section. 647 Chapter 11: Statement of cash flows Income Satement Adjustments ncrease n Accounts Recevable ncrease n inventory Increase in Accounts Payable Decrease in Accrued Liabite Cash Flows From Operanons 297 500 267 700 Cash Colected fram Accounts Recevables Sales (29 800) (19250) 0 Cost of Goods Soldi 99460) 4420 (114 290 Cash Pad to Supplers Oner Operatirg Expenses (14670) (6730) (21 400) Cash pad for Other expenses (220 Cash pad for income Ta n400 Cash Pad for Dedend ncome Ta Expense (7270) 32210 ncrease in Retaned Eamngs Net ncomer sas30 Interest experse (2 Cash pad for nterest epense ABC Manufacturing Pty Ltd. Cash low Statement For the period December 31,2014 (Direct method) 62 Particulars Cash flows from operating Activites Cash Collected from Accounts Recevable Less Cash Pad to Supplers Cash Pad for Oner Expenses Cash Pad for erest expense Cash pad for Income Tax espense Net Cash previded by Operating Activitles Details Amount 65 267.700 (114 290) 67 21400) (2940) (7270) 121800 70 Cash Flows from Investing Activities 72 Sale of Investment 2.500 73 24 Sale of Equipment Cash paid for purchase of equipment Net Cash used by Investing Activities 15.550 75 (92.000) 76 (73,950) 77 Cash Flows from Financing Activities 70 issue of Debentures Payable Issue of Share Capital Payment of Dividend Net cash provided by Financing Activities Net Increase in Cash & its equivalents Add Opening Balance of Cash Closing Balance of Cash 30.000 50.000 81 (78,400) 82 1,600 49,450 83 47,250 96.700 8 86 87 ABC Manufacturing Pty Ltd Cash flow Statement 90 For the period ending December 31,2015 (Indirect method) (In millions) Amount $ 91 92 (In millions) Details Particulars 93 Cash flows from operating Activities Net Income 94 132,210 95 Add Adjustments to reconcile net income to net cash provided by operating activities Depreciation Gain on sale of Equipment 96 97 49,700 (8.750) 98 99 100 (29.800) Increase in Accounts Receivable (19,250) 4.420 Increase in Inventory 101 Increase in Accounts Payable 102 (6,730) Decrease in Accrued Liabilities (10,410) 103 121,800 Net Cash provided by Operating Activities 104 105 Cash Flows from investing Activities Sale of Investment 106 107 2,500 Sale of Equipment 108 15.550 Cash paid for purchase of equipment Net Cash used by Investing Activities (92,000) 109 (73,950) 110 Cash Flows from Financing Activities Issue of Debentures Payable Issue of Share Capital Payment of Dividend Net cash provided by Financing Activities 112 113 30.000 114 50,000 115 (78.400) 1,600 116 Net Increase in Cash & its equivalents Add Opening Balance of Cash 49.450 47.250 117 118 Closing Balance of Cash 96.700 119 Cash Flows From Operations Income Statement Adjustments 297.500 Increase in Accounts Recevable Sales (29,800) 267 700 Cash Collected from Accounts Receivable (99,460) Increase in Inventory 50 Cost of Goods Sold (19,250) 4,420 Increase in Accounts Payable Decrease in Accrued Liabitie (114290) Cash Paid to Suppliers (21,400) Cash paid for Other expenses 51 Other Operating Expenses (14670) (6,730) 52 53 (7,270) Cash pad for Income Tax 78,400 Cash Paid for Dividend (2,940) Cash pad for Interest expense Income Tax Expense Net Income (7270) 54 132.210 Increase in Retained Eamings 53.810 56 Interest expense (2,940) 58 ABC Manufacturing Pty Ltd. Cash flow Statement 60 For the period December 31,2015 (Direct method) 61 62 Details Amount Particulars 63 Cash flows from operating Activities 64 Cash Collected from Accounts Receivable 267.700 65 Less Cash Paid to Suppliers Cash Paid for Other Expenses Cash Paid for nterest expense (114290) 66 (21,400) (2,940) (7.270) 67 68 Cash paid for Income Tax expense Net Cash provided by Operating Activities 69 121.800 70 Cash Flows from Investing Activities Sale of Investment 72 73 2,500 Sale of Equipment Cash paid for purchase of equipment Net Cash used by Investing Activities 74 15,550 (92,000) 75 (73,950) 76 77 Cash Flows from Financing Activities Issue of Debentures Payable Issue of Share Capital Payment of Dividend Net cash provided by Financing Activities 78 30,000 79 80 50,000 (78,400) 81 1,600 82 49,450 Net Increase in Cash & its equivalents Add Opening Balance of Cash Closing Balance of Cash 83 47.250 84 96,700 85 86 87 87 ABC Manufacturing Pty Ltd. 89 Cash flow Statement 90 (Indirect method) For the period ending December 31,2015 (In millions) Details $ 91 (In millions) Amount $ 92 Particulars 93 Cash flows from operating Activities 94 132,210 Net Income 95 Add Adjustments to reconcile net income to net cash provided by operating activities: Depreciation Gain on sale of Equipment 96 97 49,700 98 (8,750) (29,800) (19,250) 4,420 (6,730) 99 Increase in Accounts Receivable 100 Increase in Inventory Increase in Accounts Payable 101 102 Decrease in Accrued Liabilities (10410) 121,800 103 Net Cash provided by Operating Activities 104 105 Cash Flows from Investing Activities Sale of Investment Sale of Equipment Cash paid for purchase of equipment 106 107 2,500 108 15,550 109 (92,000) Net Cash used by Investing Activities (73,950) 110 Cash Flows from Financing Activities Issue of Debentures Payable Issue of Share Capital Payment of Dividend Net cash provided by Financing Activities Net Increase in Cash & its equivalents Add Opening Balance of Cash 112 113 30,000 114 50,000 (78,400) 115 1,600 116 49,450 117 47,250 118 Closing Balance of Cash 96,700 119