Question

How to Proceed Develop your investment proposal business case draft: Calculate the bond yield to utilize as your required return. Prepare a summary narrative (i.e.,

How to Proceed

Develop your investment proposal business case draft:

- Calculate the bond yield to utilize as your required return.

- Prepare a summary narrative (i.e., a detailed description) of each proposal with detailed elements on the initial investment, as well as the costs/revenues over the life of each of the projects. Identify which revenues and costs are relevant to your analysis, and which costs are irrelevant. Identify the time horizon for each investment.

- Calculate the after-tax cash flows during the life of each of the projects. Be sure to identify the total costs of ownership and deduct those costs from the benefits to arrive at the net cash inflow per year.

- Utilizing the after-tax cash flows from Part 4, evaluate each investment proposal utilizing the following criteria (unless directed otherwise):

- changes in payments from beginning of period to end;

- Payback;

- Discounted payback;

- NPV;

- Profitability index.

- Clearly indicate whether any of the above criteria support each of the project proposals, and what the company should ultimately decide to do.

Pear Computer Horizons Case Study

Investment Proposals

Amanda Morrison, CEO of PCH, wants you to evaluate two investment proposals that the company is considering:

- The acquisition of a Canadian camera company; and

- The launch of a new product for government and business enterprises.

Ms. Morrison reminds you that only relevant costs and revenues should be considered. "Relevant costs have to be occurring in the future," explained Ms. Morrison. "And have to differ from the status quo. For example, if we choose to buy the Canadian camera company, it is only the incremental revenue and costs related to the purchase that should be considered. We also need to take into account the opportunity costs associated with the alternatives. For example, for the new product launch, we need to factor in the lost sales from some of our current products in catering to those customers."

More details on each investment proposal are included below. Ms. Morrison wants you to recommend if PCH should invest in one, both, or none of the investment proposals.

Required Return

Ms. Morrison wants you to use the weighted average bond yield for your required return. The total market value of debt PCH is expected to have going into this investment is $200M, which includes the current amount of bonds on the financial statements of $150M at a 6% interest rate and a planned new debt issuance of $50M at a higher 8% rate. All long-term debt is in the form of bonds. Ignore income tax effects when calculating the required return (i.e., do not take the after-tax cost of debt). Use current interest rates as a proxy for bond yield.

Acquisition of Canadian Camera Company

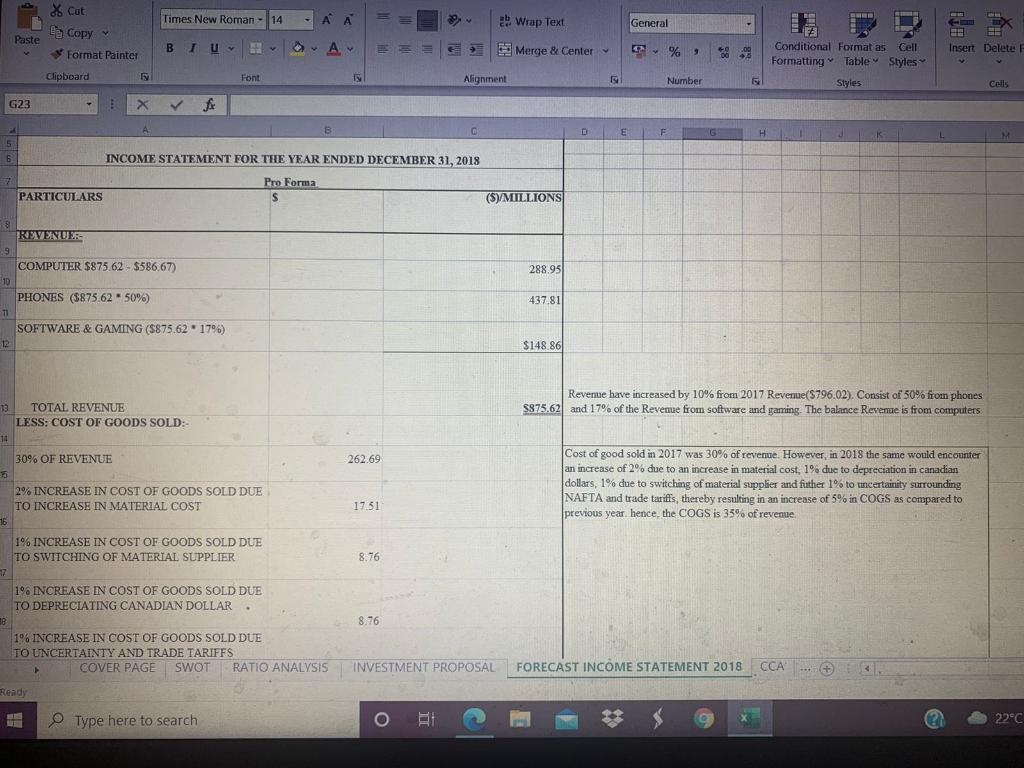

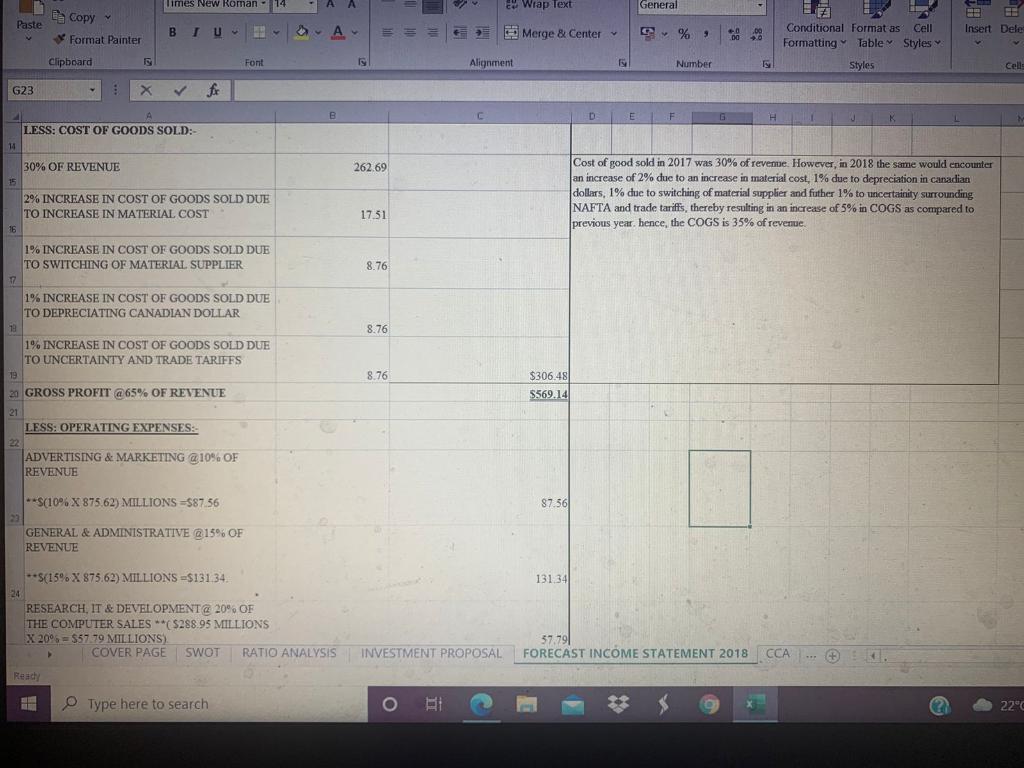

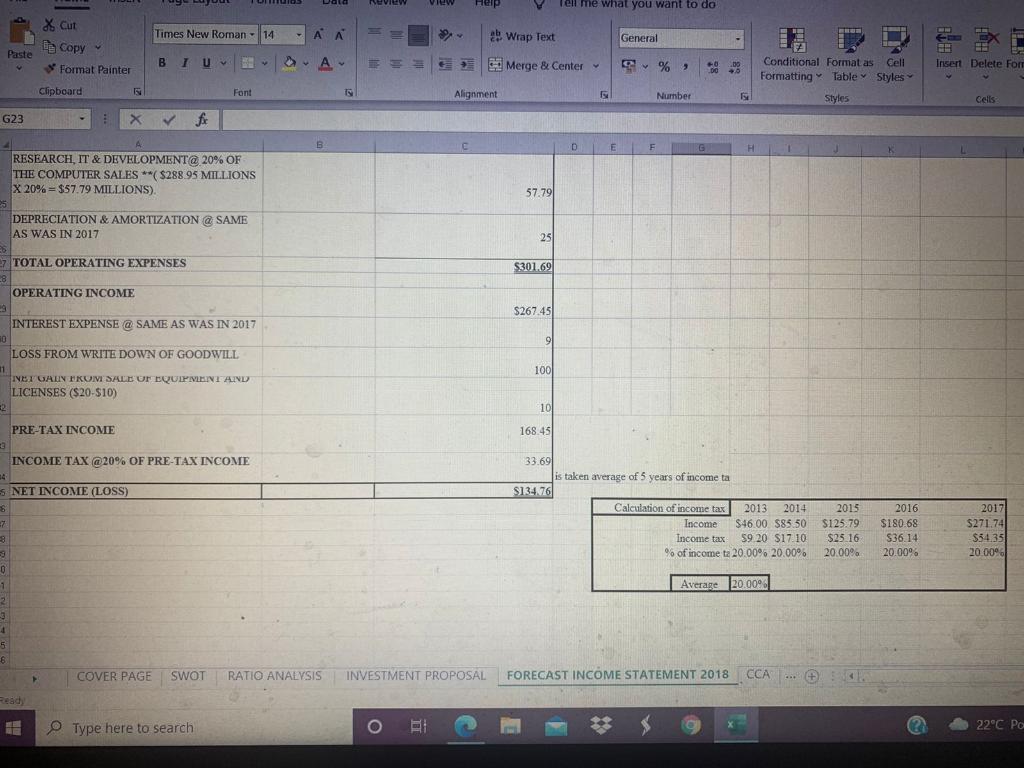

Ms. Morrison is considering acquiring a high-tech Canadian camera company for $50M in cash consideration. The camera phones that the target company is developing are only in the prototype stage, and would need an initial investment of $10M for development costs (to be expensed immediately) and $6M for production equipment. The camera company currently only has $1M of available tax shield left, excluding any tax shield related to the additional equipment to be purchased, for equipment that was originally purchased for $10M. Furthermore, PCH plans on spending an additional $2.025M in research and development (R&D) costs every year to continue to innovate with the camera phones and adopt new advancements in technology, as they are internally developed or externally acquired.

The manufacturing costs for the camera phones are expected to be 45% of sales, once the phone passes the prototype stage into the final product stage when the phones can start to be sold. Software support costs for upgrades and warranty & repair costs are expected to be 6% and 5% of sales, respectively. These costs, as a percentage of sales, are expected to remain consistent over the time horizon. It is anticipated that twenty employees from the camera company will be absorbed into PCH, with the average employee having a salary (including benefits) of $100,000. Other incremental manufacturing overhead costs (property taxes, maintenance, security, etc.), excluding depreciation, are estimated to be $1M annually. Wages are expected to increase with inflation (estimated at 2%) over the time period, while other fixed costs are expected to remain steady.

Due to the integration process of the camera company into PCH operations and the additional development required for the prototype camera phones, initial sales are only expected to reach a volume of 50,000 units in the first year. However, production is expected to double in Year 2, Year 3, and Year 4, before stabilizing at 400,000 units per year. Additional marketing costs of $3M per year will be spent to promote the product among the millennial segment through a social media campaign and promotional events.

The camera phone's retail price to consumers is $500, but that includes the 30% markup that retailers apply to the phone to make a profit. Thus, the sales price for PCH would be 70% of the retail price, and this price is expected to increase by inflation over the time horizon.

Ms. Morrison wants to see if the project will reach profitability after 5 years, so she wants you to evaluate the return on investment in that period using the investment criteria of payback period, discounted payback period, NPV, IRR, and profitability index. The following table will help in the calculations of the tax shield for the new equipment:

| Class | CCA Rate | Description |

|---|---|---|

| 43 | 30% | Machine and equipment to manufacture and process goods for sale |

Tax Shield Formula:

Assume no salvage value when calculating the tax shield, and that the half-year rule applies for each class. The tax rate Ms. Morrison wants you to utilize is 20%. When calculating the tax shield, the present value should be in the same period as the initial investment (Year 0), which also means that deprecation (i.e., CCA) should not be taken from the cash flows in subsequent years, since their tax shelter effects are already accounted for in the tax shield.

New Product Launch

Ms. Morrison also wants you to evaluate if PCH should go forward with a new product launch for business and government enterprises. Over the past several years, PCH has spent over

$50M on R&D on a new laptop and associated software. An additional investment of $20M is required before the product is ready to launch. There are 40 universities and 25 government ministries across Canada that are interested in entering ten-year contracts with PCH, which would lead to $75K in before-tax cash flow from each client. However, the interested parties are also existing clients of PCH, which means that the current contracts (with ten years remaining) that lead to $15K in before-tax cash flow per client would be nullified. Ms. Morrison wants you to evaluate the profitability of this investment after a ten-year period using the investment criteria of NPV and profitability index.

You will be assessed in accordance with the following rubric:

| Q1 | Bond Yield | Marks | Student | ||

|---|---|---|---|---|---|

| Bond Yield | 2 | ||||

| Attempt to use weighted average of debt | 2 | ||||

| Q2 | Summary Narrative | Marks | Student | ||

| Description of Investment 1 | 4 | ||||

| Description of Investment 2 | 4 | ||||

| Time horizons identified | 4 | ||||

| Irrelevant and relevant costs identified | 4 | ||||

| Q3 | After-tax Cash Flows | Marks | Student | ||

| Investment 1: Acquisition of Camera Company | |||||

| Initial Investment Including Equipment & development | 3 | ||||

| Old tax shield included | 1 | ||||

| Investment horizon utilized | 2 | ||||

| Reasonable inclusion of inflation | 1 | ||||

| Correct volume for phone sales | 1 | ||||

| Correct sales price for phones | 1 | ||||

| Warranty Costs Considered | 1 | ||||

| Manufacturing Costs Considered | 2 | ||||

| Software support costs considered | 2 | ||||

| Incremental Marketing costs included | 2 | ||||

| Salary of twenty employees considered | 2 | ||||

| Other overhead costs considered | 2 | ||||

| Incremental R&D costs included | 2 | ||||

| After-tax cash flows (ATCF) calculated | 4 | ||||

| Attempt at Tax Shield | 2 | ||||

| Investment 2: New Product Launch | |||||

| Initial Investment Calculation (ignore sunk costs) | 2 | ||||

| Correct amount of clients identified | 1 | ||||

| After-tax cash flows (ATCF) calculated | 2 | ||||

| Ten-year horizon utilized | 1 | ||||

| Opportunity cost of lost cash flow included | 2 | ||||

| Q4 | Investment Criteria Calculated | Marks | Student | ||

| Investment 1: Acquisition of Camera Company | |||||

| Payback Period | 2 | ||||

| Discounted Payback Period | 2 | ||||

| Net Present Value | 6 | ||||

| Internal Rate of Return | 2 | ||||

| Profitability Index | 2 | ||||

| Investment 2: New Product Launch | |||||

| Net Present Value | 4 | ||||

| Profitability Index | 2 | ||||

| Q6 | Evaluation of Two Investment Proposals | Marks | Student | ||

| Investment 1 Recommendation | 6 | ||||

| Investment 2 Recommendation | 6 | ||||

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Karen Braun, Wendy Tietz, Louis Beaubien

4th Canadian Edition

013544344X, 9780135443446