Answered step by step

Verified Expert Solution

Question

1 Approved Answer

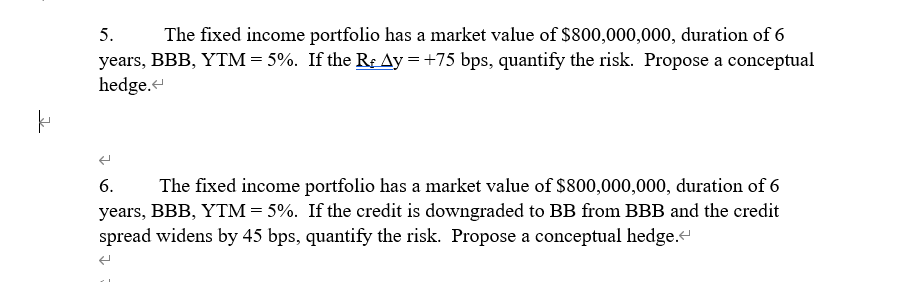

How to quantify the risk when credit spread widens? Can you help me with the questions below? Thx 5. The fixed income portfolio has a

How to quantify the risk when credit spread widens? Can you help me with the questions below? Thx

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Developments In Entrepreneurial Finance And Technology

Authors: David B. Audretsch, Maksim Belitski, Nada Rejeb, Rosa Caiazza

1st Edition

1800884338,1800884346