Question

How to simulate the following scenario using Stella Architect software ? Insurance First Australia Insurance First Australia (IFA) is an insurance company specialising in the

How to simulate the following scenario using Stella Architect software ?

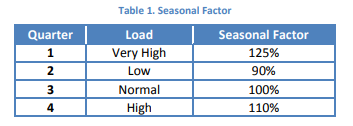

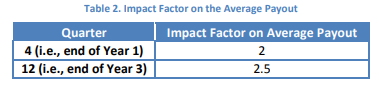

Insurance First Australia Insurance First Australia (IFA) is an insurance company specialising in the sale, management and underwriting of insurance products in Australia. Currently, IFA is offering five types of insurance to Australian households: car, home, landlords, pet, and life insurance. According to an IBISWorlds report on Australia market research, the number of Australians travelling overseas has grown strongly over the past five years; the growth in the number of senior citizen travellers is particularly notable. The IFA senior executive team saw this as a good business opportunity to enter the travel insurance market. You have been employed as a DSS analyst by the IFA CEO to help him plan the establishment of the new insurance product. While the IFA executives have made what they think are sound judgments of the various factors surrounding the new travel insurance, they want a DSS that will allow them to easily vary these estimates in order to see the impact of different assumptions on the insurances operation. A meeting has been held with the executives of the IFA Strategy Committee where they outlined the nature of the insurances operation to you. The area that the committee wants help with is forecasting the travel insurance claims and profit scenario for the first 5 years. To simplify the scenario, the committee is planning at a quarterly level, rather than monthly or weekly. Given the nature of travel insurance and the claim process designed by IFA, there are five types of claims that are of interest to IFA: Initialised claim the travel insurance policy holder has encountered incident(s) during travel, and is thinking of making a claim; Prepared claim the travel insurance policy holder who has started filling the travel insurance claim form and collecting supporting evidence; Lodged claim the travel insurance claim that has been lodged to IFA for assessment; Approved claim the travel insurance claim that has been approved by IFA; Settled claim the approved travel insurance claim that has been settled (i.e. payments have been made in most cases). To set up the new line of insurance product, the IFA Strategy Committee is planning to spend 260,000 AUD from the corporate budget as a oneoff setup fee (including marketing) in the first quarter of the first year. Based on market research from similar businesses, it is estimated that the initial marketing expenses will result in 3,000 travel insurance policies for IFA in the first quarter. However, the number of insurance policies per quarter is also subject to a seasonal factor. This means that the initial number of insurance policies multiplied by the seasonal factor estimates the number of actual insurance policies per quarter. Table 1 below shows the seasonal effect on the number of insurance policies.  Not all the travel insurance holders will make a claim. It is estimated that 9 in 100 policy holders will encounter some kind of issues during travel (e.g., injury, sickness, travel delay, cancellation/additional expenses, damaged/lost/stolen luggage/cash/personal belongings/travel documents, rental vehicle excess, overseas emergencies), and they will seek insurance claim procedure information on the company website or call the IFA claims team to find out how they can make a claim. This group of insurance policy holders is considered as initialised claim by the IFA Strategy Committee. After initial consultation of the claim procedure, the Committee thinks that about 10% of initialised claim policy holders may realise that their issues are not covered by the purchased insurance policy (that is, they are not eligible to make a claim) or the claim process is too much work that is not worth the effort; and those policy holders wont go ahead with making a claim. For those who decide to make a claim will then start to prepare their claims, including filling out the claim form(s) and collecting all the supporting documents and evidence. However, during the preparation process, it is estimated that 1 in 20 insurance policy holders may find it impossible to collect all the required documentation, and as a result, these policy holders will decide not to proceed with the claim. The remaining insurance policy holders who have filled out all the forms and organised all the supporting evidence will then lodge their claims to IFA. The IFA Strategy Committee thinks there are four possible outcomes for those lodged claims, and they illustrate it to you (as the DSS analyst) in the following example using 100 claims as the base, and the outcomes are ordered based on their priority or precedence: (1) Out of 100 lodged claims, about 50 claims will be identified as missing either the required evidence or necessary information after the assessment by an IFA staff. These claims will be sent back to the policy holders for revision and resubmission. (2) For the remaining 50 claims, 3% will be withdrawn due to personal or unknown reasons. (3) For the remaining claims, 22% will be rejected due to reasons like preexisting medical conditions, not providing adequate supporting documentation, illegal or reckless behaviour, events happened before the insurance cover, and the like. (4) The rest will be approved. Answering customer enquiries and assessing insurance claims for the new travel insurance product requires additional human resources. In addition to the financial commitment, IFA will also recruit three staff members initially for the travel insurance line. However, there are different salary oncosts for different types of employees. To simplify the scenario, the Committee only considers two types of employment: full time contract, and casual. In IFA, fulltime contract staff will attract 31% oncost, whereas casual staff will attract 16% oncost. Given the cost implications, the Committee decides to hire two fulltime contract staff for the first five years, and the remaining will be filled by casual positions. In addition, due to the seasonal fluctuations of the number of travel insurance policy purchase, the total number of staff employed at any time will also be adjusted based on the same seasonal factor as shown in Table 1. Such adjustment is only possible with casual employment. Despite the nature of the employment, the average fulltime equivalent (FTE) staffs salary is 67,000 AUD per annum. In IFA, the standard working week for an FTE staff is 37.5 hours per week based on 7.5 hours per day, 5 days per week. On an annual basis, an FTE staff is expected to work 48 weeks, minus 11 days on public holidays or leaves, on average. Out of staffs total available working hours, in their first year, it is estimated that they will spend 60% of their time on processing claims of all kinds, and the remaining 40% time on answering customer enquiries, meetings, training, governance, and other admin/services types of activities. In the subsequent years, the percentage of their time spent on processing claims will increase by 3% per year since the staff will be gaining more experience and becoming more efficient in dealing with admin/services types of work. According to a travel insurance industry report, it is estimated that on average, one staff needs to spend three and a half hours on assessing one travel insurance claim. This time is measured from the point that the staff starts assessing the claim to the point that a decision is made (revise and resubmit, reject, or approve). All the approved claims will be settled, in most cases, in the form of reimbursement. The same group of staff will make the reimbursement to the approved claims. However, their job priority is given to claim assessment. This means, only when they finish assessing all the claims, they will proceed to process the reimbursement. The standard reimbursement duration in IFA is 10 days, subject to staff availability. The industry benchmark for travel insurance reimbursement duration is 20 days. A key variable that the CEO wants to be reported in the model is the real reimbursement duration. Comparing this to the industry benchmark and IFA specified standard will show the CEO how the travel insurance claims overall performance is and whether there is any room for improvement in terms of customer experience. The same travel insurance industry report also indicates that in normal conditions, the average travel insurance payout is 950 AUD per approved claim (after subtracting the insurance excess paid by the policy holder). However, it is estimated that there might be two contingencies during the fiveyear period that will significantly affect the travel insurance industry in Australia it can be severe weather or natural disaster, political tension or crisis, and the like which will lead to a higher than normal average payout during that period. No one can predict exactly when such contingencies will happen. But for the purpose of the DSS, the Committee gave you two arbitrary periods, which are shown below in Table 2, along with their impact factors from the contingencies on the average quarterly payout.

Not all the travel insurance holders will make a claim. It is estimated that 9 in 100 policy holders will encounter some kind of issues during travel (e.g., injury, sickness, travel delay, cancellation/additional expenses, damaged/lost/stolen luggage/cash/personal belongings/travel documents, rental vehicle excess, overseas emergencies), and they will seek insurance claim procedure information on the company website or call the IFA claims team to find out how they can make a claim. This group of insurance policy holders is considered as initialised claim by the IFA Strategy Committee. After initial consultation of the claim procedure, the Committee thinks that about 10% of initialised claim policy holders may realise that their issues are not covered by the purchased insurance policy (that is, they are not eligible to make a claim) or the claim process is too much work that is not worth the effort; and those policy holders wont go ahead with making a claim. For those who decide to make a claim will then start to prepare their claims, including filling out the claim form(s) and collecting all the supporting documents and evidence. However, during the preparation process, it is estimated that 1 in 20 insurance policy holders may find it impossible to collect all the required documentation, and as a result, these policy holders will decide not to proceed with the claim. The remaining insurance policy holders who have filled out all the forms and organised all the supporting evidence will then lodge their claims to IFA. The IFA Strategy Committee thinks there are four possible outcomes for those lodged claims, and they illustrate it to you (as the DSS analyst) in the following example using 100 claims as the base, and the outcomes are ordered based on their priority or precedence: (1) Out of 100 lodged claims, about 50 claims will be identified as missing either the required evidence or necessary information after the assessment by an IFA staff. These claims will be sent back to the policy holders for revision and resubmission. (2) For the remaining 50 claims, 3% will be withdrawn due to personal or unknown reasons. (3) For the remaining claims, 22% will be rejected due to reasons like preexisting medical conditions, not providing adequate supporting documentation, illegal or reckless behaviour, events happened before the insurance cover, and the like. (4) The rest will be approved. Answering customer enquiries and assessing insurance claims for the new travel insurance product requires additional human resources. In addition to the financial commitment, IFA will also recruit three staff members initially for the travel insurance line. However, there are different salary oncosts for different types of employees. To simplify the scenario, the Committee only considers two types of employment: full time contract, and casual. In IFA, fulltime contract staff will attract 31% oncost, whereas casual staff will attract 16% oncost. Given the cost implications, the Committee decides to hire two fulltime contract staff for the first five years, and the remaining will be filled by casual positions. In addition, due to the seasonal fluctuations of the number of travel insurance policy purchase, the total number of staff employed at any time will also be adjusted based on the same seasonal factor as shown in Table 1. Such adjustment is only possible with casual employment. Despite the nature of the employment, the average fulltime equivalent (FTE) staffs salary is 67,000 AUD per annum. In IFA, the standard working week for an FTE staff is 37.5 hours per week based on 7.5 hours per day, 5 days per week. On an annual basis, an FTE staff is expected to work 48 weeks, minus 11 days on public holidays or leaves, on average. Out of staffs total available working hours, in their first year, it is estimated that they will spend 60% of their time on processing claims of all kinds, and the remaining 40% time on answering customer enquiries, meetings, training, governance, and other admin/services types of activities. In the subsequent years, the percentage of their time spent on processing claims will increase by 3% per year since the staff will be gaining more experience and becoming more efficient in dealing with admin/services types of work. According to a travel insurance industry report, it is estimated that on average, one staff needs to spend three and a half hours on assessing one travel insurance claim. This time is measured from the point that the staff starts assessing the claim to the point that a decision is made (revise and resubmit, reject, or approve). All the approved claims will be settled, in most cases, in the form of reimbursement. The same group of staff will make the reimbursement to the approved claims. However, their job priority is given to claim assessment. This means, only when they finish assessing all the claims, they will proceed to process the reimbursement. The standard reimbursement duration in IFA is 10 days, subject to staff availability. The industry benchmark for travel insurance reimbursement duration is 20 days. A key variable that the CEO wants to be reported in the model is the real reimbursement duration. Comparing this to the industry benchmark and IFA specified standard will show the CEO how the travel insurance claims overall performance is and whether there is any room for improvement in terms of customer experience. The same travel insurance industry report also indicates that in normal conditions, the average travel insurance payout is 950 AUD per approved claim (after subtracting the insurance excess paid by the policy holder). However, it is estimated that there might be two contingencies during the fiveyear period that will significantly affect the travel insurance industry in Australia it can be severe weather or natural disaster, political tension or crisis, and the like which will lead to a higher than normal average payout during that period. No one can predict exactly when such contingencies will happen. But for the purpose of the DSS, the Committee gave you two arbitrary periods, which are shown below in Table 2, along with their impact factors from the contingencies on the average quarterly payout.  On top of the salary expenses and insurance payouts, there are other expenses, such as facility, equipment, utility, maintenance, and the like, which are approximately 200,000 AUD per year in total. All these expenses (salary, payouts, and other expenses) are expected to increase in line with the Australian Consumer Price Index (CPI), which is about 2% per year. IFA is planning to offer three major classes of travel insurance: Saver, Basic, and Comprehensive. Different classes of travel insurance will attract different premiums; however, on average, each customer will be charged 12 AUD per day as premium. The average length of active travel insurance policy is 6.5 days, and is subject to the same seasonal factor as detailed in Table 1. In addition, the premium is also subject to a CPI 2% increase every year. As any other businesses, IFA requires its new travel insurance products revenues to be higher than its costs to be profitable. The CEO of IFA would like to understand the forecasted financial position of the travel insurance in terms of its profit per quarter. In addition to the seasonally adjusted insurance policy number, market research shows that 1 in 1000 of IFA travel insurance policy holders are likely to cause another person to buy a travel insurance from IFA the word of mouth factor. In addition, successful insurance claimants are likely to repeat their travel insurance purchase with IFA in the future at a rate of 6%, whereas only 1% of customers who had not encountered any issues and thus never made a claim may buy travel insurance from IFA again. However, 2 in 100 customers who have had bad customer experiences with IFA will spread negative wordofmouth. Bad customer experiences include those who wanted to make a claim but either didnt due to various reasons or being rejected.

On top of the salary expenses and insurance payouts, there are other expenses, such as facility, equipment, utility, maintenance, and the like, which are approximately 200,000 AUD per year in total. All these expenses (salary, payouts, and other expenses) are expected to increase in line with the Australian Consumer Price Index (CPI), which is about 2% per year. IFA is planning to offer three major classes of travel insurance: Saver, Basic, and Comprehensive. Different classes of travel insurance will attract different premiums; however, on average, each customer will be charged 12 AUD per day as premium. The average length of active travel insurance policy is 6.5 days, and is subject to the same seasonal factor as detailed in Table 1. In addition, the premium is also subject to a CPI 2% increase every year. As any other businesses, IFA requires its new travel insurance products revenues to be higher than its costs to be profitable. The CEO of IFA would like to understand the forecasted financial position of the travel insurance in terms of its profit per quarter. In addition to the seasonally adjusted insurance policy number, market research shows that 1 in 1000 of IFA travel insurance policy holders are likely to cause another person to buy a travel insurance from IFA the word of mouth factor. In addition, successful insurance claimants are likely to repeat their travel insurance purchase with IFA in the future at a rate of 6%, whereas only 1% of customers who had not encountered any issues and thus never made a claim may buy travel insurance from IFA again. However, 2 in 100 customers who have had bad customer experiences with IFA will spread negative wordofmouth. Bad customer experiences include those who wanted to make a claim but either didnt due to various reasons or being rejected.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Implementing Standardized Work Training And Auditing

Authors: Alain Patchong

1st Edition

146656363X, 978-1466563636