Answered step by step

Verified Expert Solution

Question

1 Approved Answer

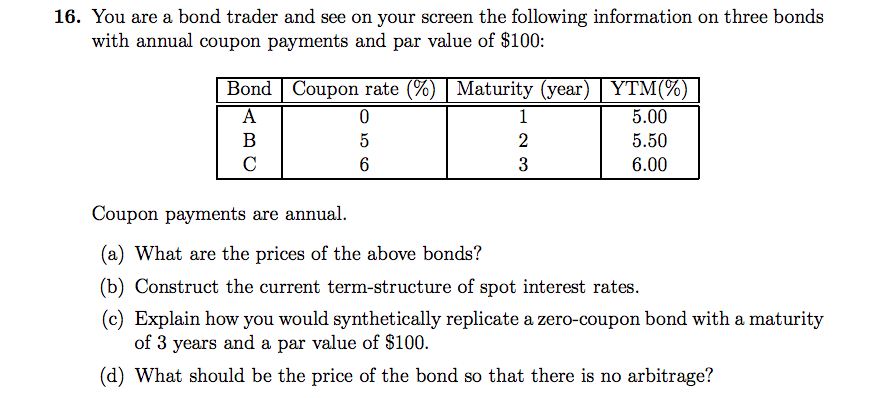

How to solve (c) and (d) ? 16. You are a bond trader and see on your screen the following information on three bonds with

How to solve (c) and (d) ?

16. You are a bond trader and see on your screen the following information on three bonds with annual coupon payments and par value of $100: Bond Coupon rate (% Oto Maturity (year) YTM(%) 5.00 5.50 6.00 WNL Coupon payments are annual. (a) What are the prices of the above bonds? (b) Construct the current term-structure of spot interest rates. (c) Explain how you would synthetically replicate a zero-coupon bond with a maturity of 3 years and a par value of $100. (d) What should be the price of the bond so that there is no arbitrage? 16. You are a bond trader and see on your screen the following information on three bonds with annual coupon payments and par value of $100: Bond Coupon rate (% Oto Maturity (year) YTM(%) 5.00 5.50 6.00 WNL Coupon payments are annual. (a) What are the prices of the above bonds? (b) Construct the current term-structure of spot interest rates. (c) Explain how you would synthetically replicate a zero-coupon bond with a maturity of 3 years and a par value of $100. (d) What should be the price of the bond so that there is no arbitrageStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dividend Growth Investing Machine

Authors: Andrew P.C.

1st Edition

1521728461, 978-1521728468