Answered step by step

Verified Expert Solution

Question

1 Approved Answer

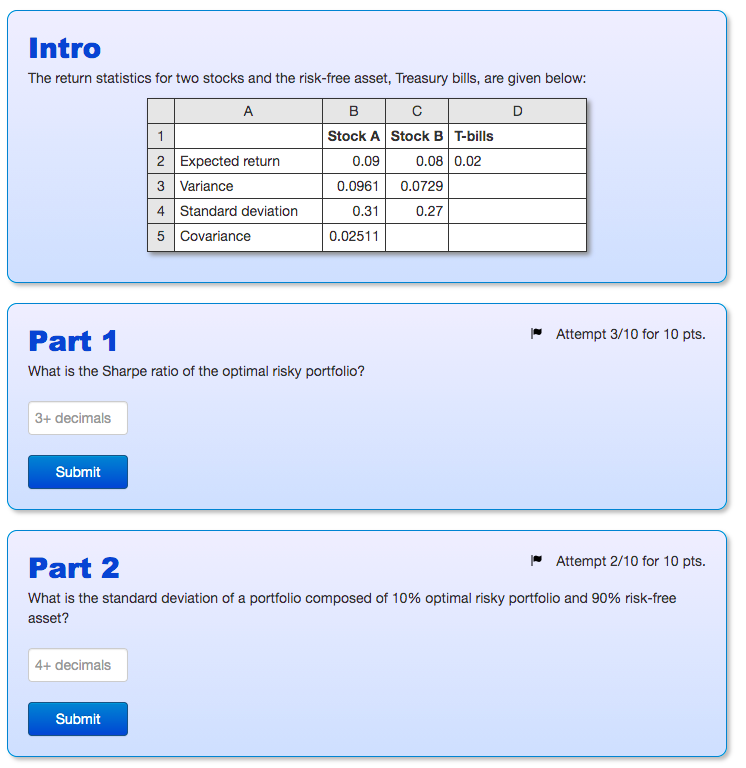

how to solve these two Intro The return statistics for two stocks and the risk-free asset, Treasury bills, are given below: A B D 1

how to solve these two

how to solve these two

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ouch What You Dont Know About Money And Why It Matters More Than You Think

Authors: Paul Knott

1st Edition

0133527077,0273788752