Answered step by step

Verified Expert Solution

Question

1 Approved Answer

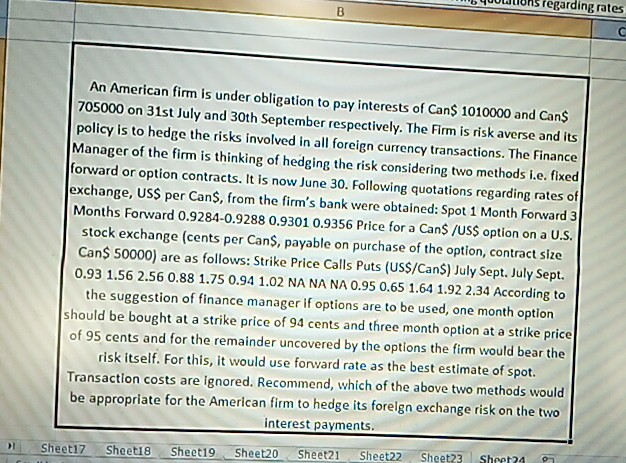

hs fegarding rates An American firm is under obligation to pay interests of Cans 1010000 and Cans 705000 on 31st July and 30th September respectively.

hs fegarding rates An American firm is under obligation to pay interests of Cans 1010000 and Cans 705000 on 31st July and 30th September respectively. The Firm is risk averse andi policy is to hedge the risks involved in all foreign currency transactions. The Finance Manager of the firm is thinking of hedging the risk considering two methods i.e. fixed forward or option contracts. It is now June 30. Following quotations regarding rates of exchange, USS per Cans, from the firm's bank were obtained: Spot 1 Month Forward 3 Months Forward 0.9284-0.9288 0.9301 0.9356 Price for a CanS/USS option on a U.S. stock exchange (cents per CanS, payable on purchase of the option, contract size Can$ 50000) are as follows: Strike Price Calls Puts (US$/Cans) July Sept. July Sept. 0.93 1.56 2.56 0.88 1.75 0.94 1.02 NA NA NA 0.95 0.65 1.64 1.92 2.34 According to the suggestion of finance manager if options are to be used, one month option should be bought at a strike price of 94 cents and three month option at a strike price of 95 cents and for the remainder uncovered by the options the firm would bear the risk itself. For this, it would use forward rate as the best estimate of spot. Transaction costs are ignored. Recommend, which of the above two methods would be appropriate for the American fim to hedge its forelgn exchange risk on the two interest payments. t23 Sheet24 Sheeti7 Sheet18 Sheet19 Sheet20 Sheet21 Sheet22 Sheet?? s

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Auditing Real Issues And Cases

Authors: Michael C. Knapp

6th Edition

0324303254, 9780324303254