Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I added the information from the chart i was provided, with the information on the 10 yr US treasury contract :) Im not quite sure

I added the information from the chart i was provided, with the information on the 10 yr US treasury contract :)

Im not quite sure how to do this problem. Any help would be greatly appreciated! :)

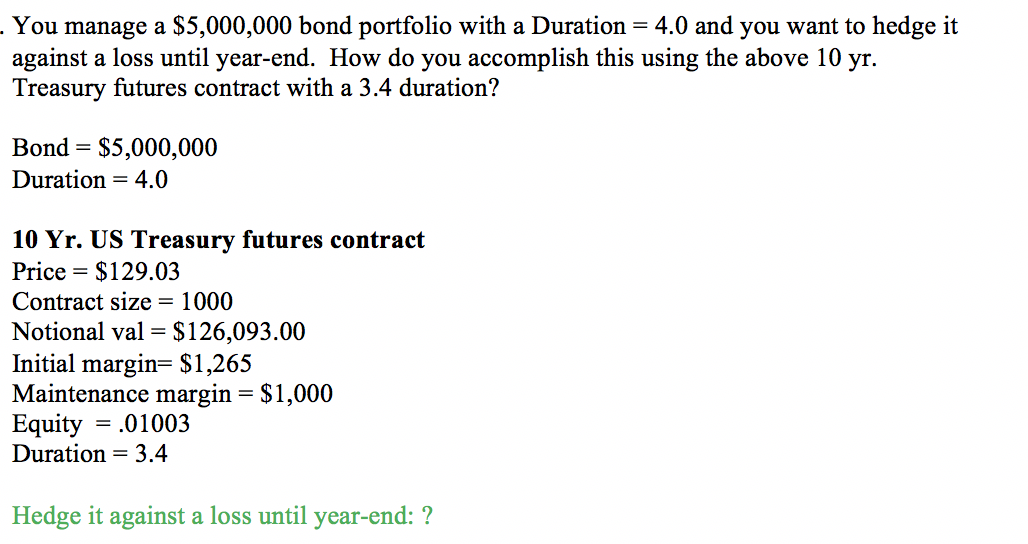

. You manage a $5,000,000 bond portfolio with a Duration = 4.0 and you want to hedge it against a loss until year-end. How do you accomplish this using the above 10 yr. Treasury futures contract with a 3.4 duration? Bond = $5,000,000 Duration 4.0 = 10 Yr. US Treasury futures contract Price = $129.03 Contract size = 1000 Notional val = $126,093.00 Initial margin= $1,265 Maintenance margin = $1,000 Equity = .01003 Duration = 3.4 Hedge it against a loss until year-end: ? . You manage a $5,000,000 bond portfolio with a Duration = 4.0 and you want to hedge it against a loss until year-end. How do you accomplish this using the above 10 yr. Treasury futures contract with a 3.4 duration? Bond = $5,000,000 Duration 4.0 = 10 Yr. US Treasury futures contract Price = $129.03 Contract size = 1000 Notional val = $126,093.00 Initial margin= $1,265 Maintenance margin = $1,000 Equity = .01003 Duration = 3.4 Hedge it against a loss until year-endStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Client Acceptance And Retention Decisions Of Audit Firms In Nigeria

Authors: Richard Iyere Oghuma

1st Edition

6138946715, 978-6138946717