I am having trouble with this excel journal entry for the proposed question.

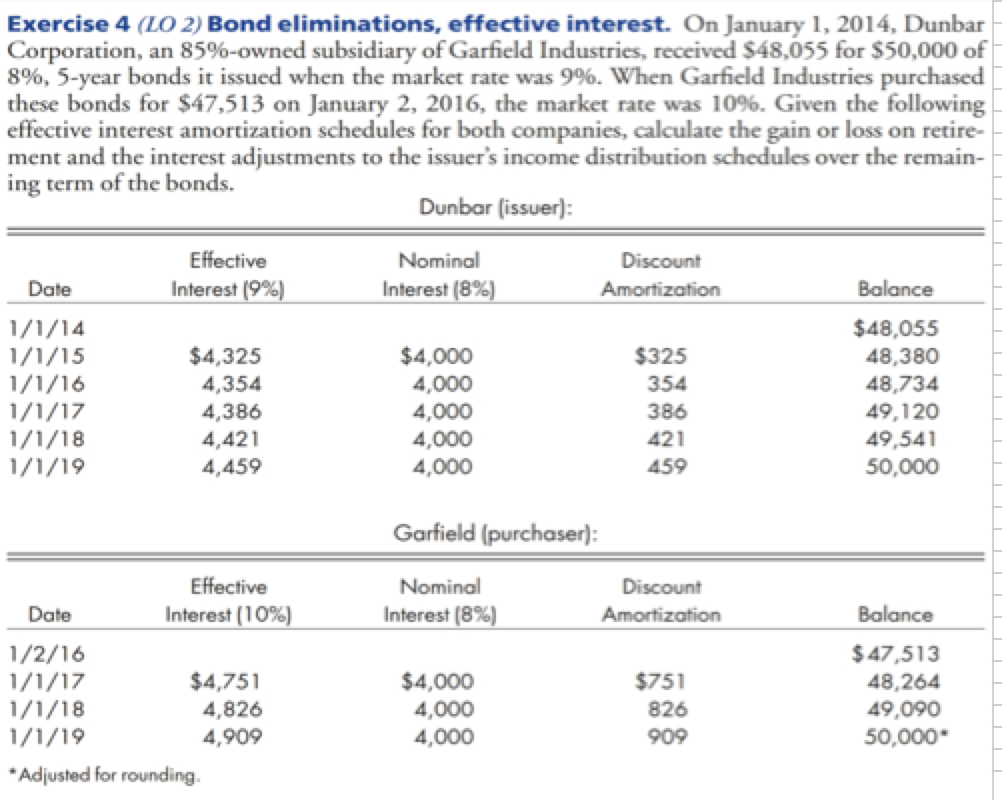

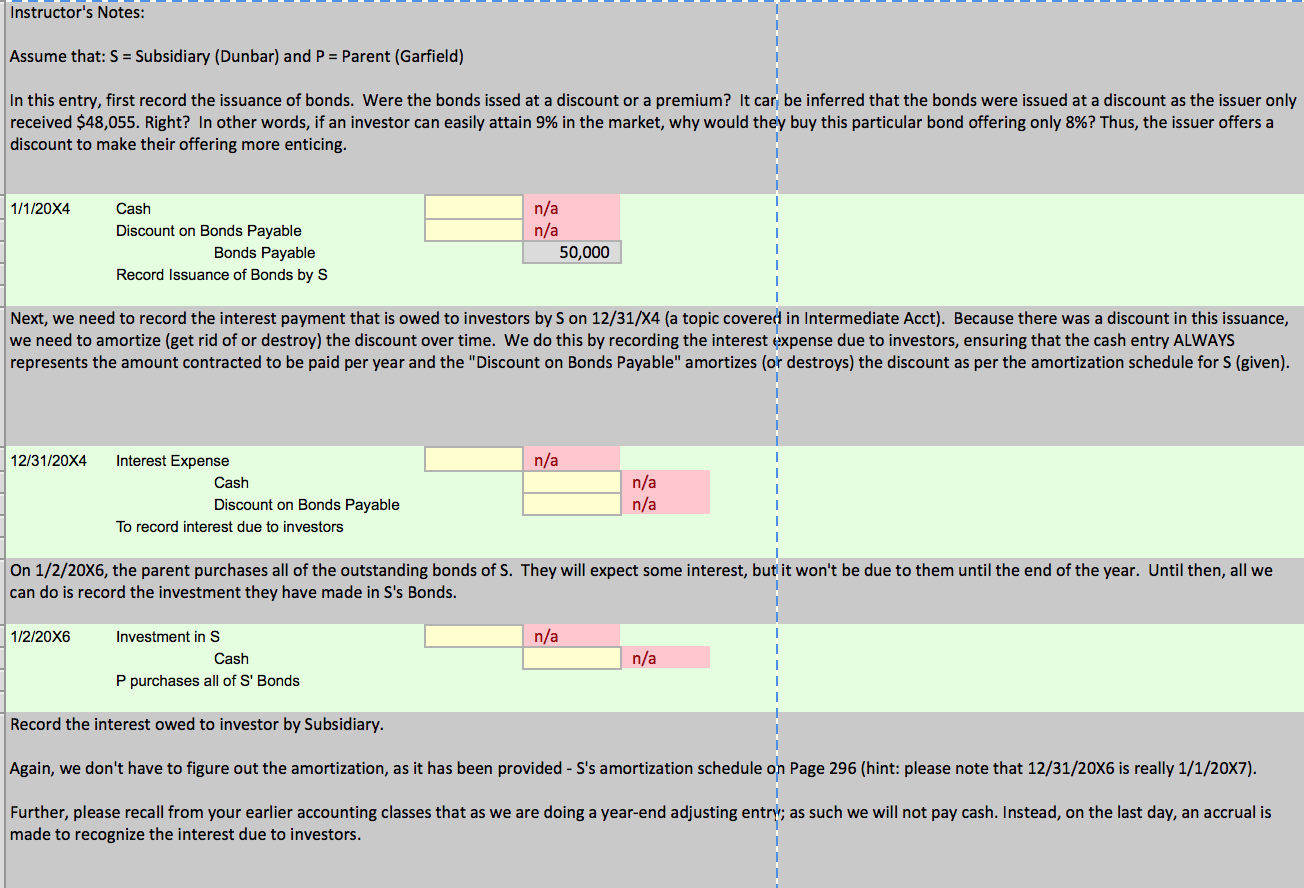

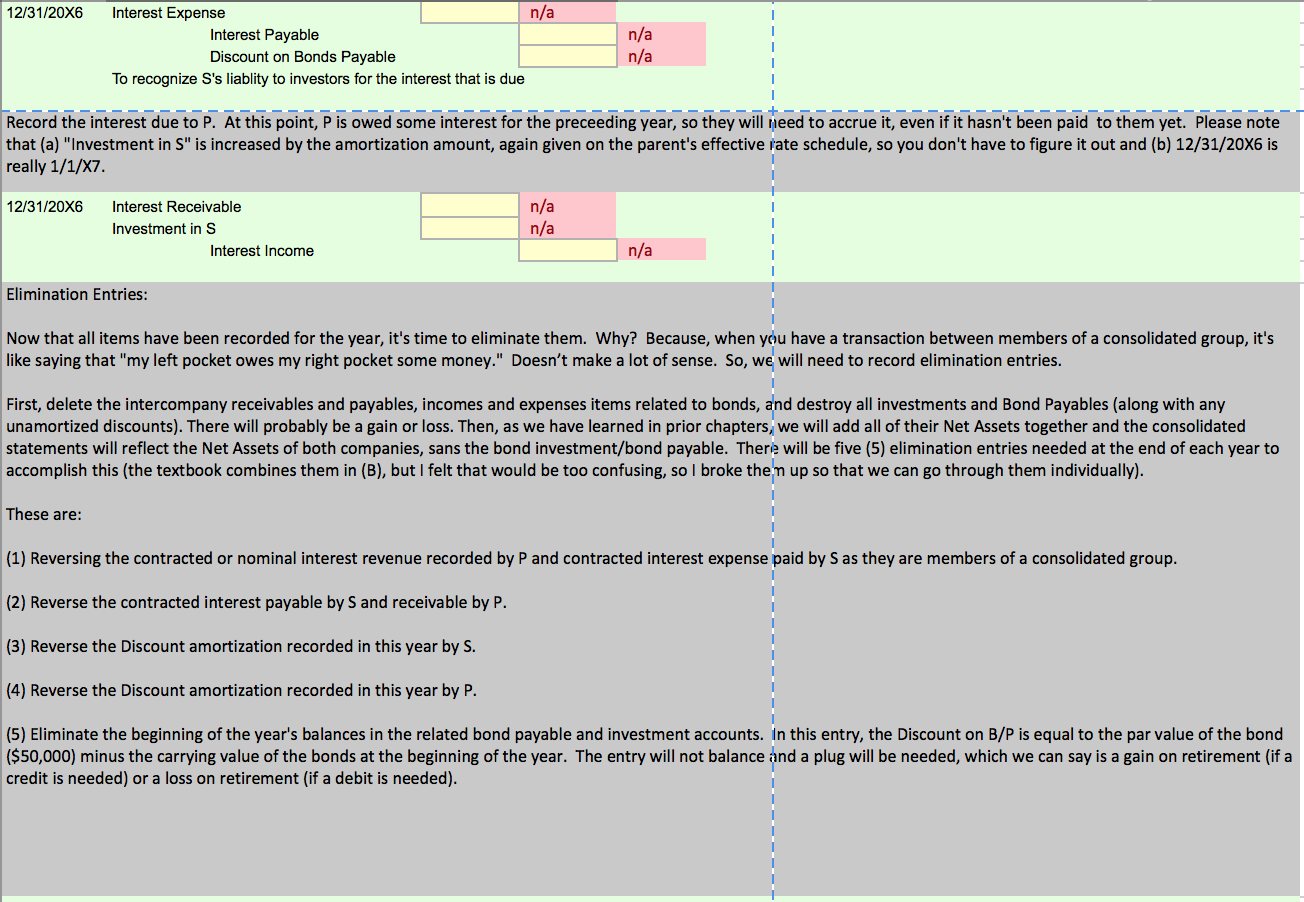

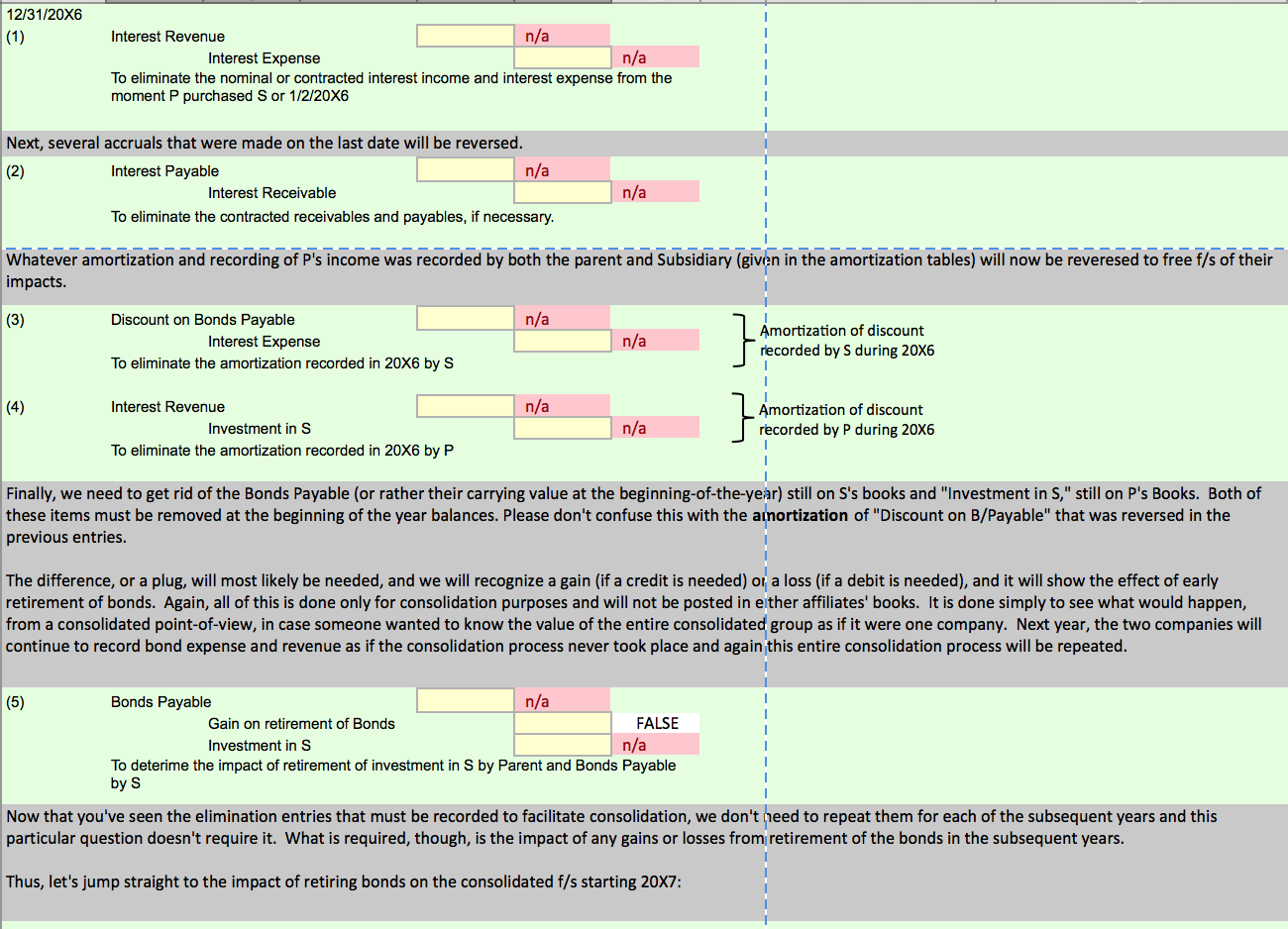

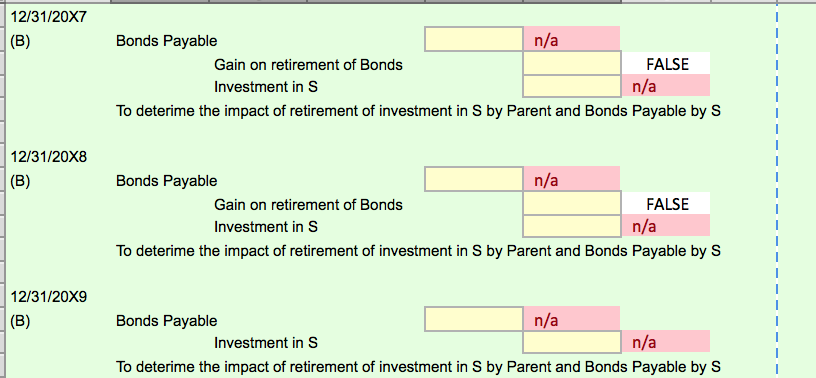

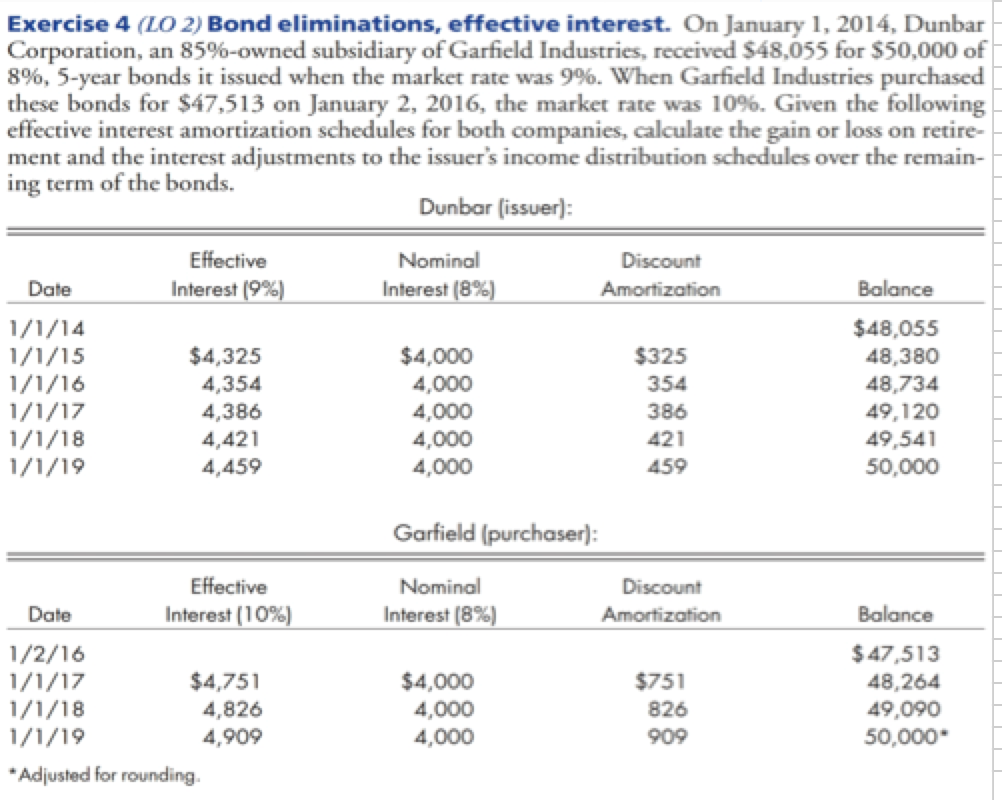

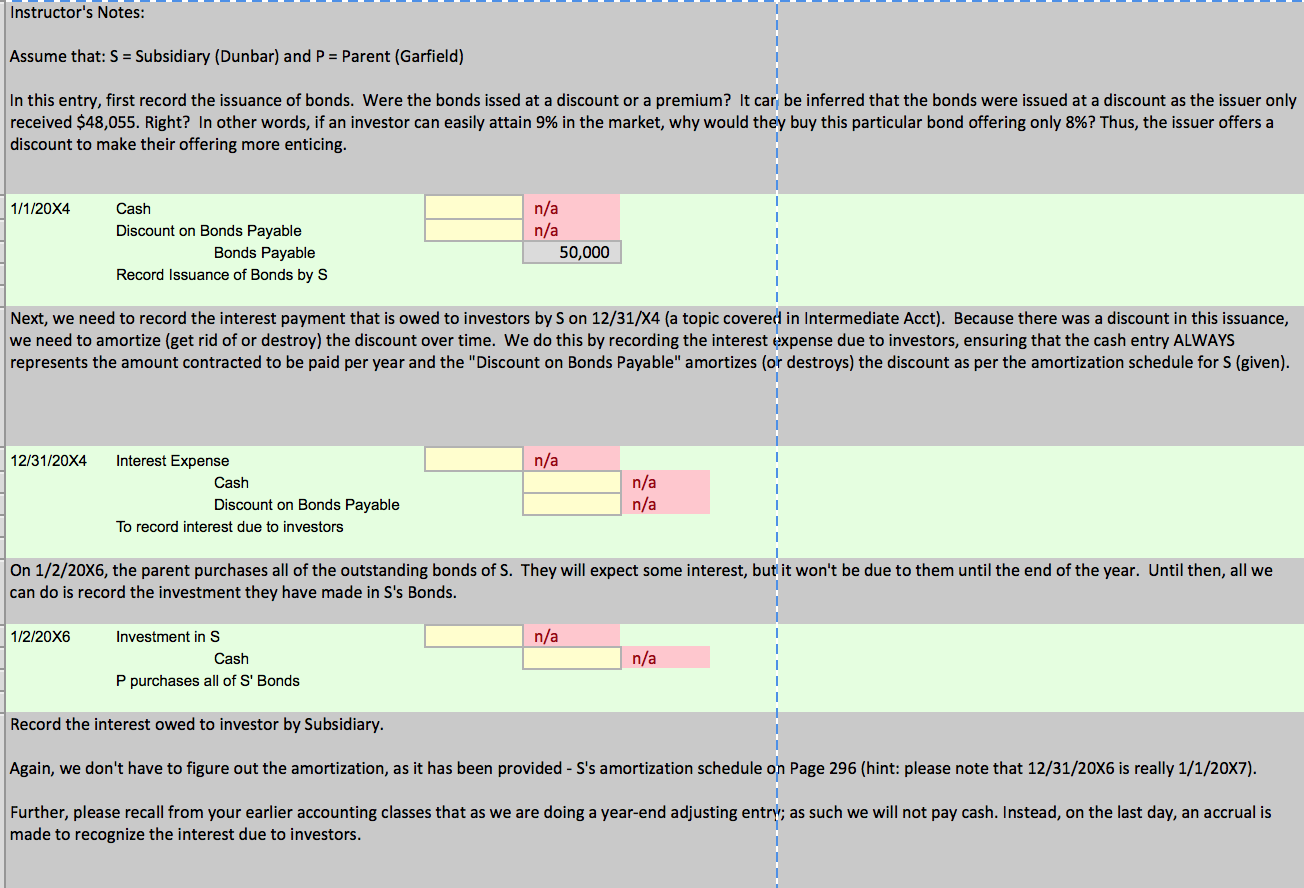

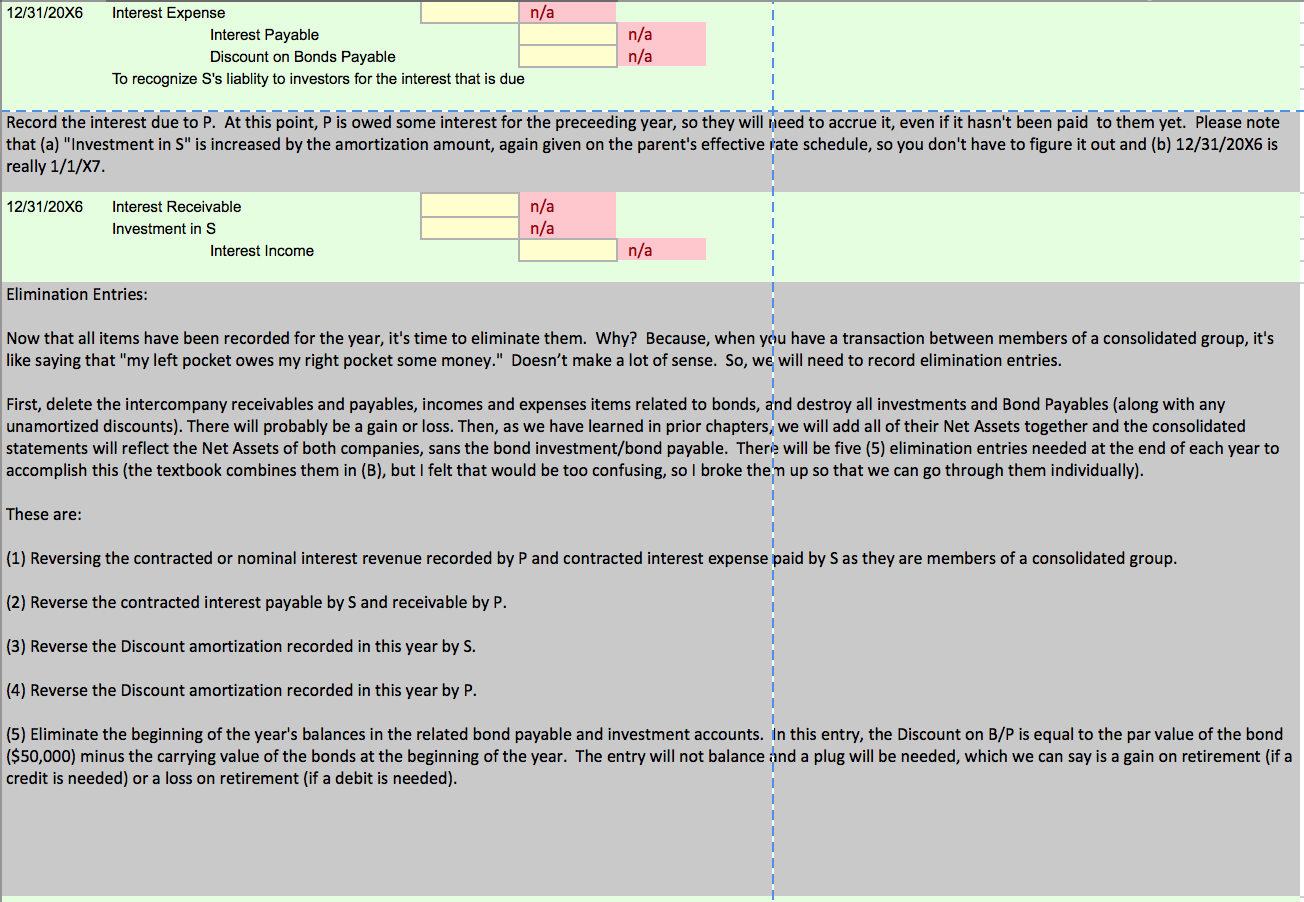

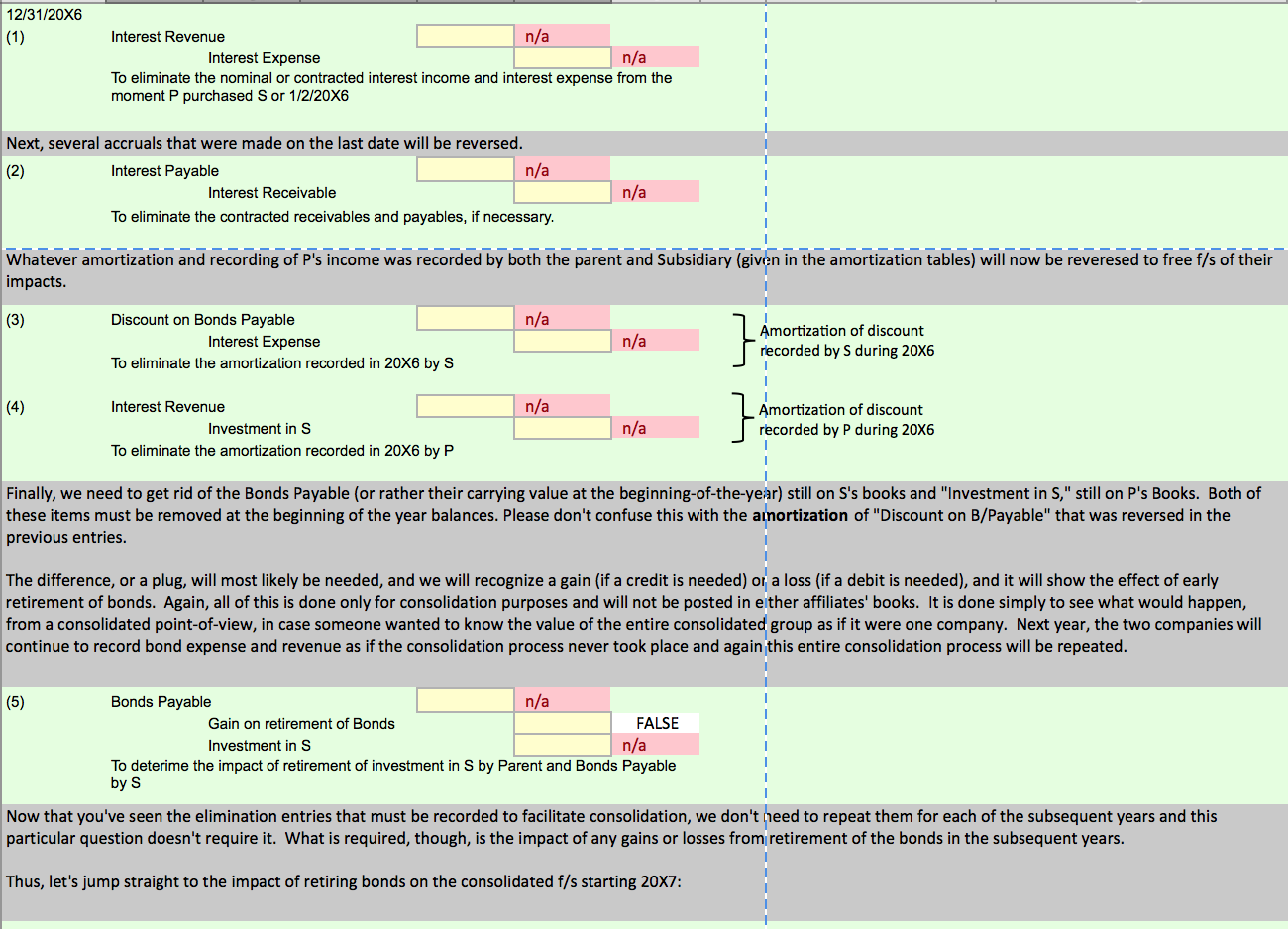

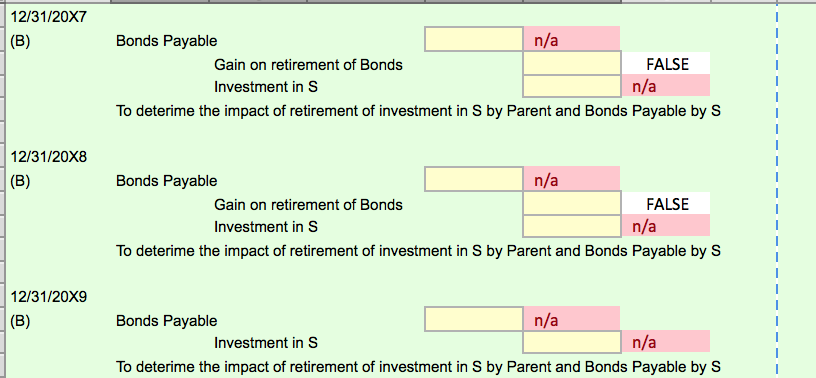

Exercise 4 (LO 2) Bond eliminations, effective interest. On January 1, 2014, Dunbar Corporation, an 85%-owned subsidiary of Garfield Industries, received $48,055 for $50,000 of 8%, 5-year bonds it issued when the market rate was 9%. When Garfield Industries purchased these bonds for $47,513 on January 2, 2016, the market rate was 10%. Given the following effective interest amortization schedules for both companies, calculate the gain or loss on retire- ment and the interest adjustments to the issuer's income distribution schedules over the remain- ing term of the bonds. Dunbar (issuer): Effective Nominal Discount Date Interest (9%) Interest (8%) Amortization Balance 1/1/14 $48,055 1/1/15 $4,325 $4,000 $325 48,380 1/1/16 4,354 4,000 354 48,734 1/1/17 4,386 4,000 386 49,120 1/1/18 4,421 4,000 421 49,541 1/1/19 4,459 4,000 459 50,000 Garfield (purchaser): Effective Nominal Discount Date Interest (10%) Interest (8%) Amortization Balance 1/2/16 $47,513 1/1/17 $4,751 $4,000 $751 48,264 1/1/18 4,826 4,000 826 49,090 1/1/19 4,909 4,000 909 50,000* *Adjusted for rounding.Instructor's Notes: Assume that: S = Subsidiary (Dunbar) and P = Parent (Garfield) In this entry, first record the issuance of bonds. Were the bonds issed at a discount or a premium? It car be inferred that the bonds were issued at a discount as the issuer only received $48,055. Right? In other words, if an investor can easily attain 9% in the market, why would they buy this particular bond offering only 8%? Thus, the issuer offers a discount to make their offering more enticing. 1/1/20X4 Cash n/a Discount on Bonds Payable n/a Bonds Payable 50,000 Record Issuance of Bonds by S Next, we need to record the interest payment that is owed to investors by S on 12/31/X4 (a topic covered in Intermediate Acct). Because there was a discount in this issuance, we need to amortize (get rid of or destroy) the discount over time. We do this by recording the interest expense due to investors, ensuring that the cash entry ALWAYS represents the amount contracted to be paid per year and the "Discount on Bonds Payable" amortizes (or destroys) the discount as per the amortization schedule for S (given). 12/31/20X4 Interest Expense n/a Cash n/a Discount on Bonds Payable n/a To record interest due to investors On 1/2/20X6, the parent purchases all of the outstanding bonds of S. They will expect some interest, but it won't be due to them until the end of the year. Until then, all we can do is record the investment they have made in S's Bonds. 1/2/20X6 Investment in S n/a Cash n/a P purchases all of S' Bonds Record the interest owed to investor by Subsidiary. Again, we don't have to figure out the amortization, as it has been provided - S's amortization schedule on Page 296 (hint: please note that 12/31/20X6 is really 1/1/20X7). Further, please recall from your earlier accounting classes that as we are doing a year-end adjusting entry; as such we will not pay cash. Instead, on the last day, an accrual is made to recognize the interest due to investors.12/31/20X6 Interest Expense n/a Interest Payable n/a Discount on Bonds Payable n/a To recognize S's liablity to investors for the interest that is due Record the interest due to P. At this point, P is owed some interest for the preceeding year, so they will need to accrue it, even if it hasn't been paid to them yet. Please note that (a) "Investment in S" is increased by the amortization amount, again given on the parent's effective rate schedule, so you don't have to figure it out and (b) 12/31/20X6 is really 1/1/X7. 12/31/20X6 Interest Receivable n/a Investment in S n/a Interest Income n/a Elimination Entries: Now that all items have been recorded for the year, it's time to eliminate them. Why? Because, when you have a transaction between members of a consolidated group, it's like saying that "my left pocket owes my right pocket some money." Doesn't make a lot of sense. So, we will need to record elimination entries. First, delete the intercompany receivables and payables, incomes and expenses items related to bonds, and destroy all investments and Bond Payables (along with any unamortized discounts). There will probably be a gain or loss. Then, as we have learned in prior chapters, we will add all of their Net Assets together and the consolidated statements will reflect the Net Assets of both companies, sans the bond investment/bond payable. There will be five (5) elimination entries needed at the end of each year to accomplish this (the textbook combines them in (B), but I felt that would be too confusing, so I broke them up so that we can go through them individually). These are: (1) Reversing the contracted or nominal interest revenue recorded by P and contracted interest expense paid by S as they are members of a consolidated group. (2) Reverse the contracted interest payable by S and receivable by P. (3) Reverse the Discount amortization recorded in this year by S. (4) Reverse the Discount amortization recorded in this year by P. (5) Eliminate the beginning of the year's balances in the related bond payable and investment accounts. In this entry, the Discount on B/P is equal to the par value of the bond ($50,000) minus the carrying value of the bonds at the beginning of the year. The entry will not balance and a plug will be needed, which we can say is a gain on retirement (if a credit is needed) or a loss on retirement (if a debit is needed).12/31/20X6 (1) Interest Revenue n/a Interest Expense n/a To eliminate the nominal or contracted interest income and interest expense from the moment P purchased S or 1/2/20X6 Next, several accruals that were made on the last date will be reversed. (2) Interest Payable n/a Interest Receivable n/a To eliminate the contracted receivables and payables, if necessary. Whatever amortization and recording of P's income was recorded by both the parent and Subsidiary (given in the amortization tables) will now be reveresed to free f/s of their impacts. (3) Discount on Bonds Payable n/a Interest Expense n/a Amortization of discount To eliminate the amortization recorded in 20X6 by S recorded by S during 20X6 (4) Interest Revenue n/a Amortization of discount Investment in S n/a recorded by P during 20X6 To eliminate the amortization recorded in 20X6 by P Finally, we need to get rid of the Bonds Payable (or rather their carrying value at the beginning-of-the-year) still on S's books and "Investment in S," still on P's Books. Both of these items must be removed at the beginning of the year balances. Please don't confuse this with the amortization of "Discount on B/Payable" that was reversed in the previous entries. The difference, or a plug, will most likely be needed, and we will recognize a gain (if a credit is needed) or a loss (if a debit is needed), and it will show the effect of early retirement of bonds. Again, all of this is done only for consolidation purposes and will not be posted in either affiliates' books. It is done simply to see what would happen, from a consolidated point-of-view, in case someone wanted to know the value of the entire consolidated group as if it were one company. Next year, the two companies will continue to record bond expense and revenue as if the consolidation process never took place and again this entire consolidation process will be repeated. (5) Bonds Payable n/a Gain on retirement of Bonds FALSE Investment in S n/a To deterime the impact of retirement of investment in S by Parent and Bonds Payable by S Now that you've seen the elimination entries that must be recorded to facilitate consolidation, we don't need to repeat them for each of the subsequent years and this particular question doesn't require it. What is required, though, is the impact of any gains or losses from retirement of the bonds in the subsequent years. Thus, let's jump straight to the impact of retiring bonds on the consolidated f/s starting 20X7:12/31/20X7 (B) Bonds Payable n/a Gain on retirement of Bonds FALSE Investment in S 1/a To deterime the impact of retirement of investment in S by Parent and Bonds Payable by S 12/31/20X8 (B) Bonds Payable n/a Gain on retirement of Bonds FALSE Investment in S n/a To deterime the impact of retirement of investment in S by Parent and Bonds Payable by S 12/31/20X9 (B) Bonds Payable n/a Investment in S /a To deterime the impact of retirement of investment in S by Parent and Bonds Payable by S