Question

I am looking for my python script to be interpreted, therefore, please address the following items: Define the null and alternative hypothesis in mathematical terms

I am looking for my python script to be interpreted, therefore, please address the following items:

- Define the null and alternative hypothesis in mathematical terms and in words.

- Report the level of significance.

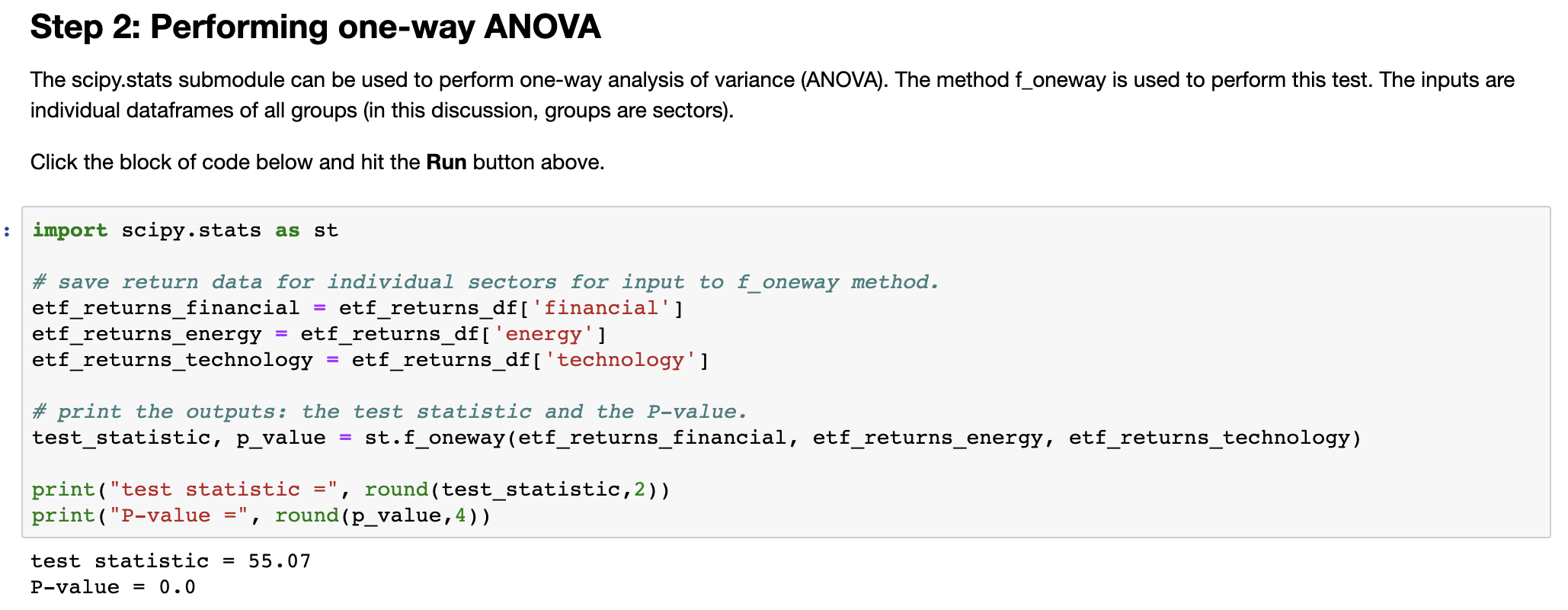

- Include the test statistic and the P-value. See Step 2 in the Python script.

- Provide your conclusion and interpretation of the test. Should the null hypothesis be rejected? Why or why not?

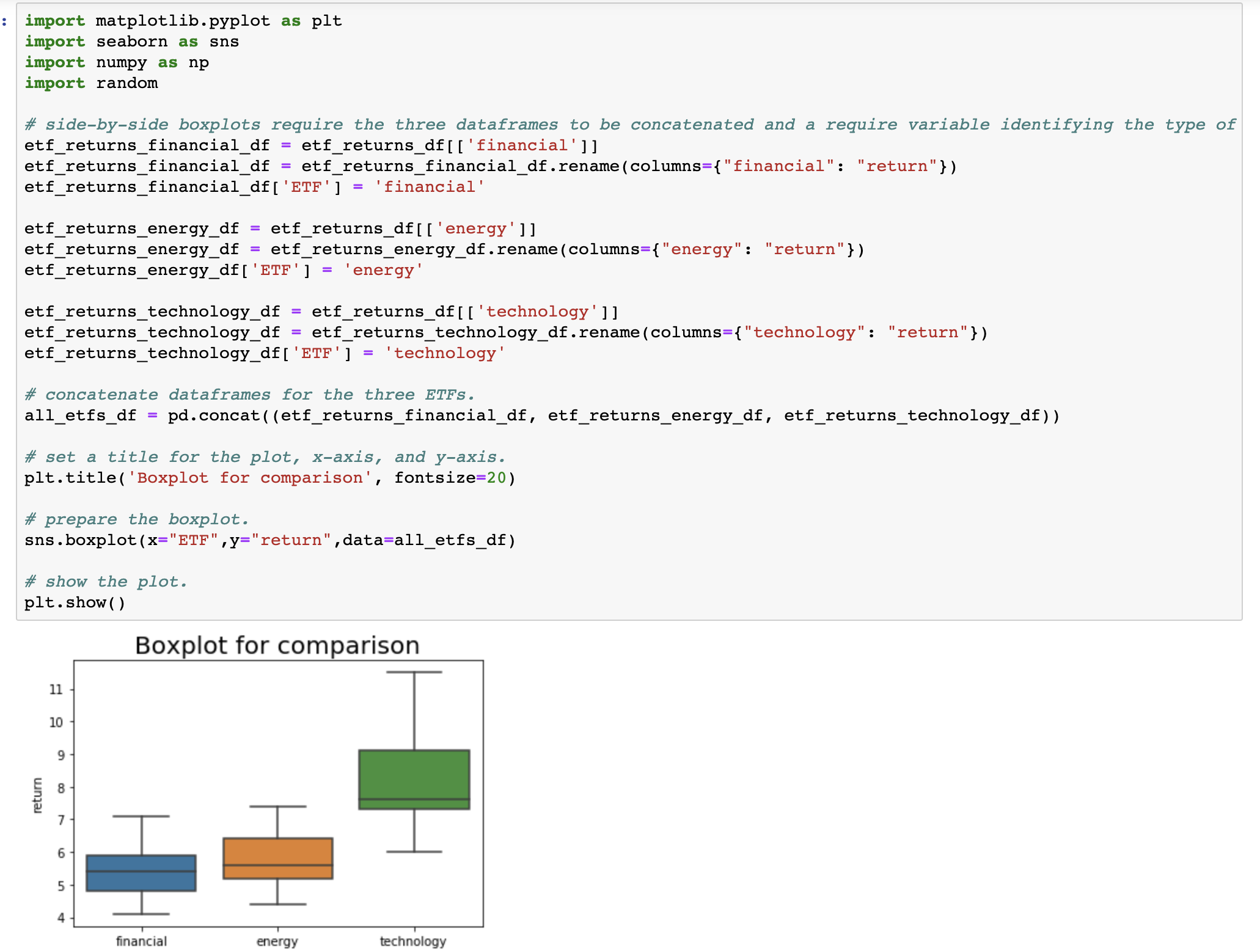

- Does a side-by-side boxplot of the 10-year returns of ETFs from the three sectors confirm your conclusion of the hypothesis test? Why or why not? See Step 3 in the Python script.

Step 1: Uploading the dataset

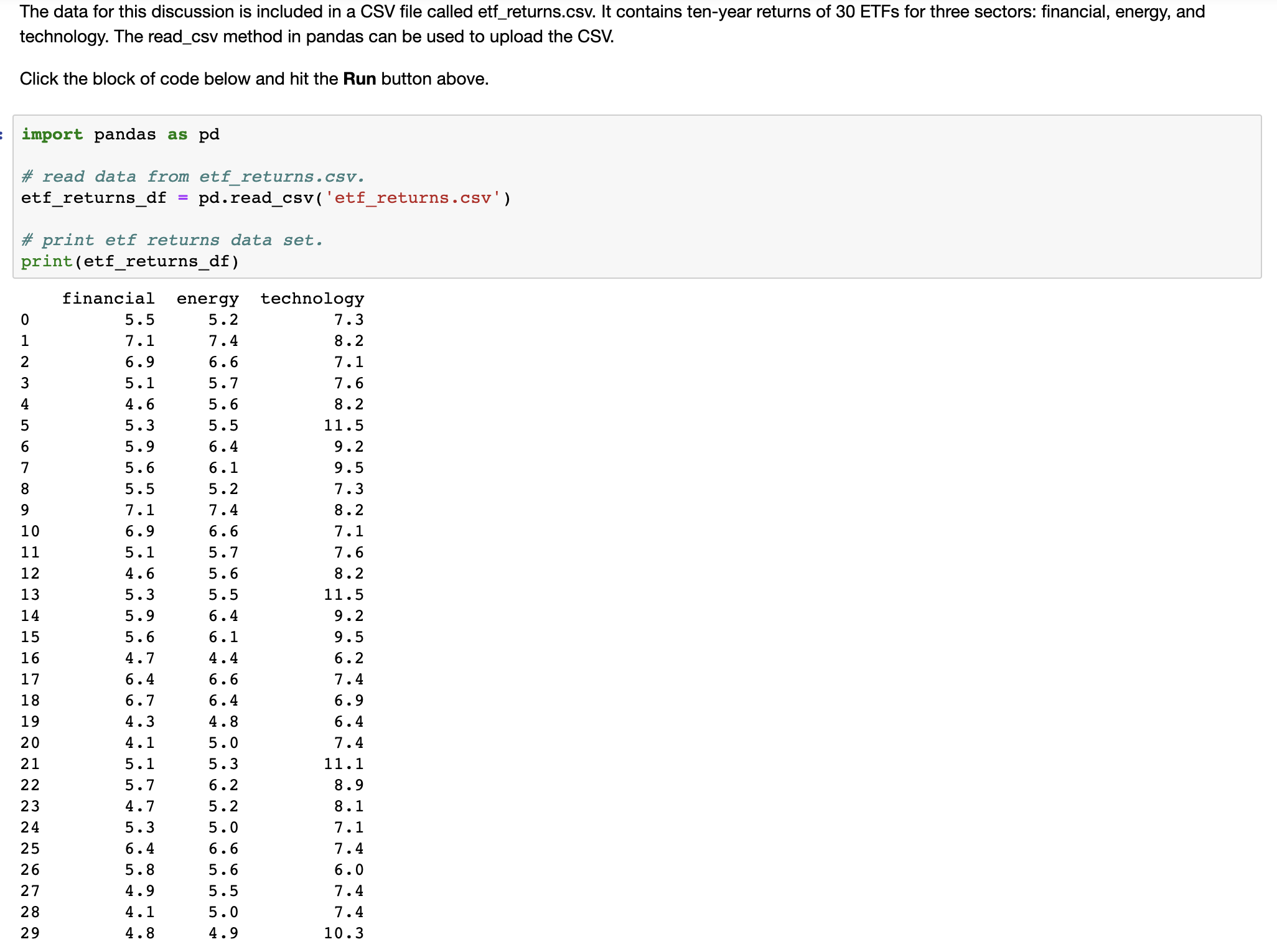

The data for this discussion is included in a CSV file called etf_returns.csv. It contains ten-year returns of 30 ETFs for three sectors: financial, energy, and technology. The read_csv method in pandas can be used to upload the CSV.

import pandas as pd

?

# read data from etf_returns.csv.

etf_returns_df = pd.read_csv('etf_returns.csv')

?

# print etf returns data set.

print(etf_returns_df)

financialenergytechnology

05.55.27.3

17.17.48.2

26.96.67.1

35.15.77.6

44.65.68.2

55.35.511.5

65.96.49.2

75.66.19.5

85.55.27.3

97.17.48.2

106.96.67.1

115.15.77.6

124.65.68.2

135.35.511.5

145.96.49.2

155.66.19.5

164.74.46.2

176.46.67.4

186.76.46.9

194.34.86.4

204.15.07.4

215.15.311.1

225.76.28.9

234.75.28.1

245.35.07.1

256.46.67.4

265.85.66.0

274.95.57.4

284.15.07.4

294.84.910.3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Structure Of Groups With A Quasiconvex Hierarchy (AMS-209)

Authors: Daniel T Wise

1st Edition

069121350X, 9780691213507