Answered step by step

Verified Expert Solution

Question

1 Approved Answer

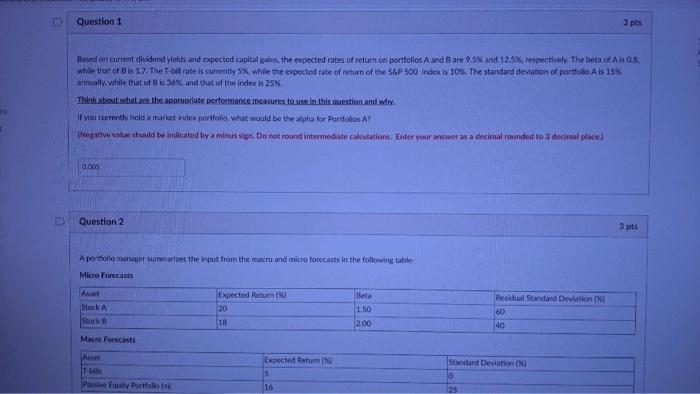

I appreciate it if someone could help me to answer those questions. Question 1 3 pts Tased on current dividend yields and expected capital gains,

I appreciate it if someone could help me to answer those questions.

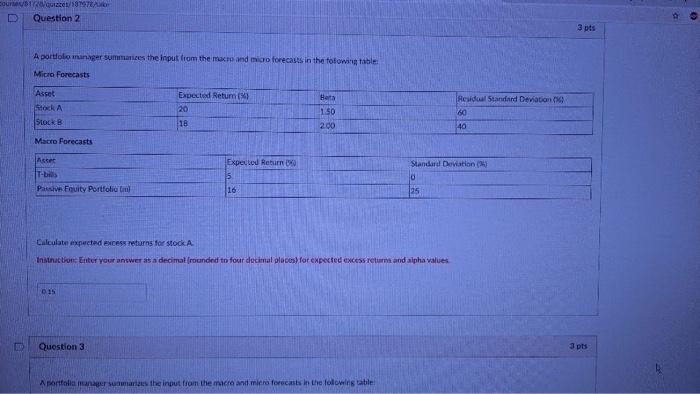

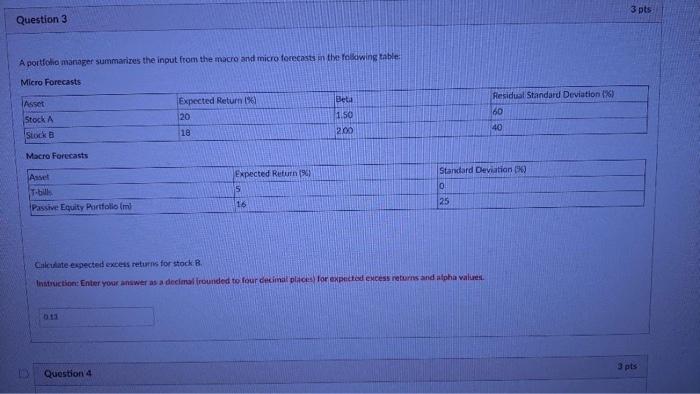

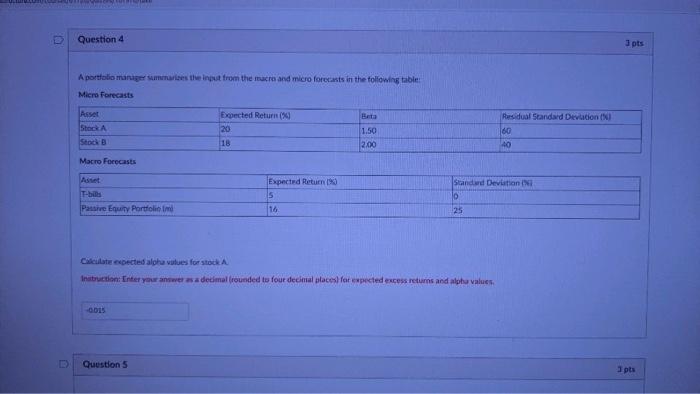

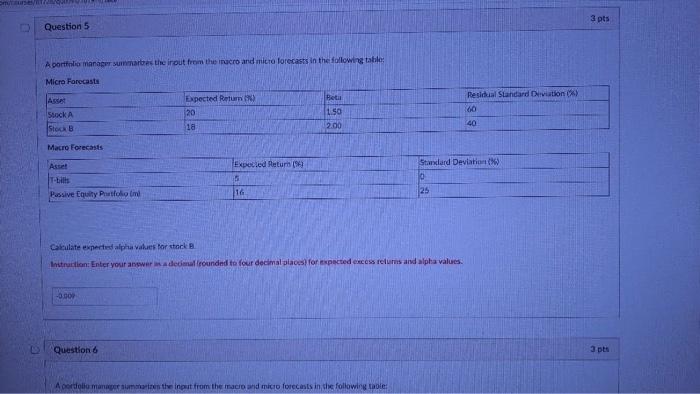

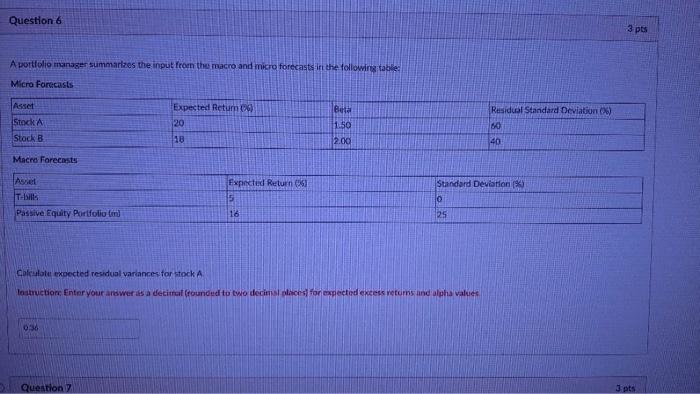

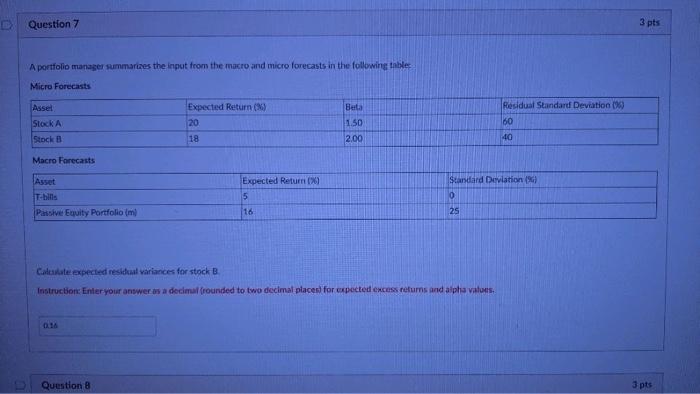

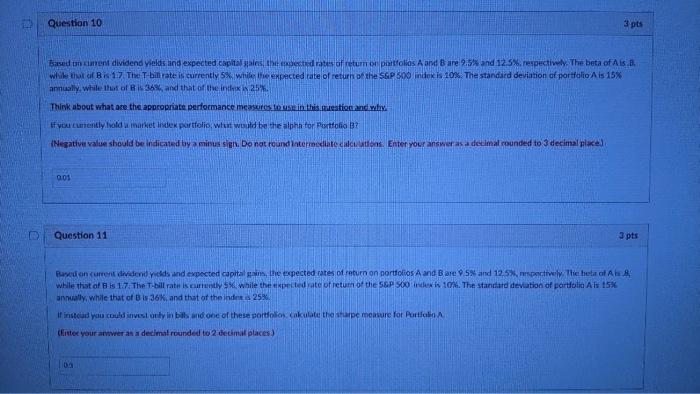

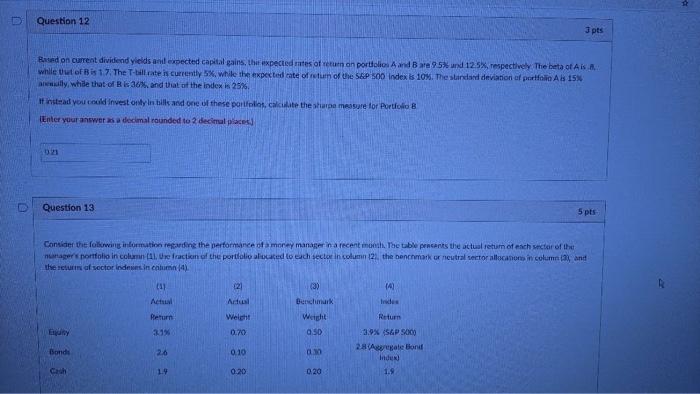

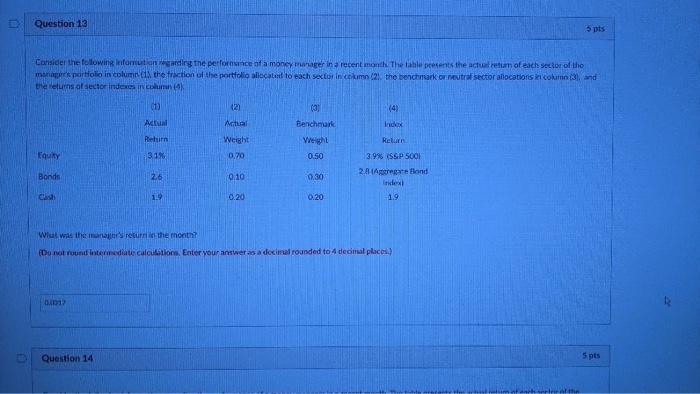

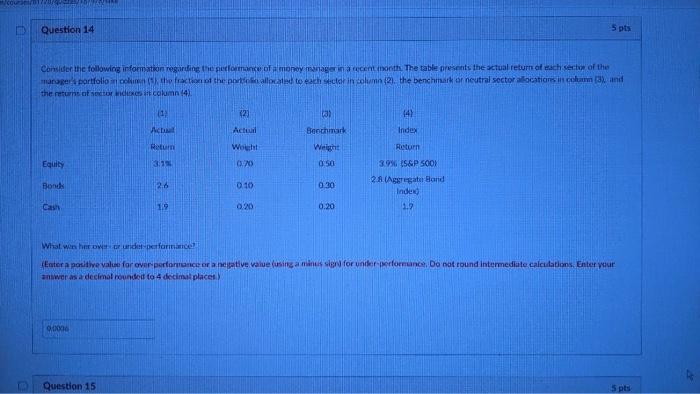

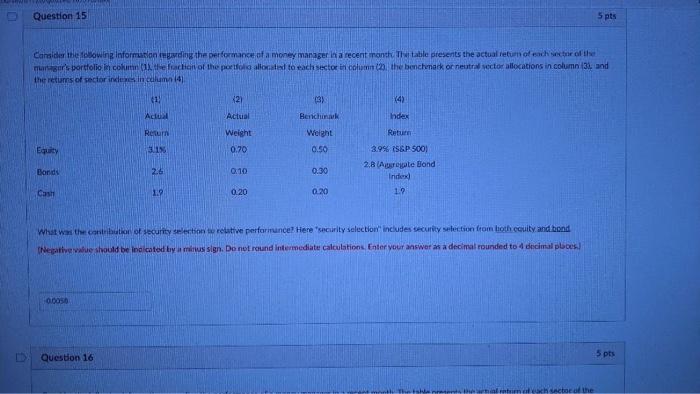

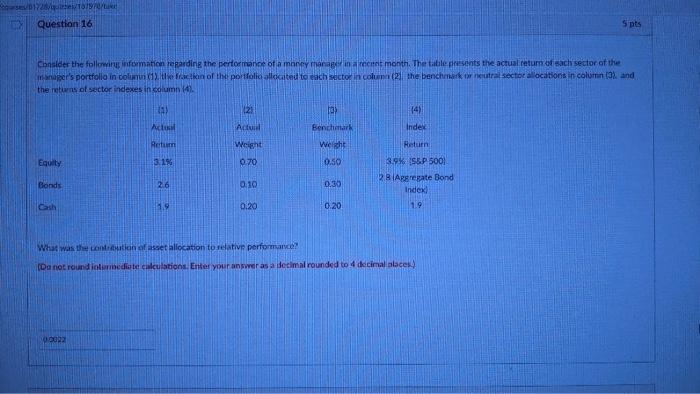

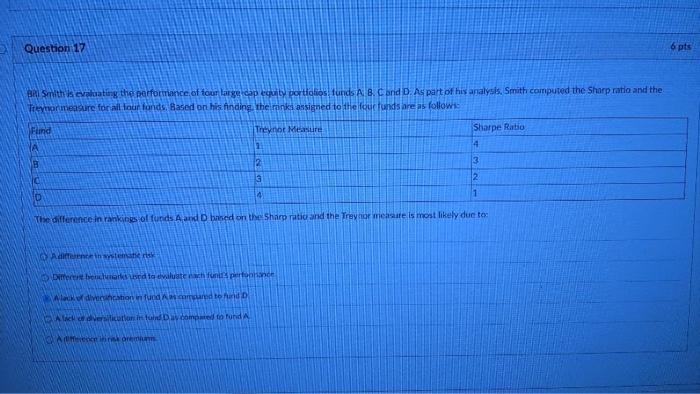

Question 1 3 pts Tased on current dividend yields and expected capital gains, the expected rates of return on portfolios A and B are 9.5% and 12.5%, respectively. The beta of Ads 0.8. while that of 1.7 The T-bilirate is currently, while the expected rate of return of the S&P 500 index is 10%. The standard deviation of portfolio Als 15% annually, while that ofis 36% and that of the Index is 25% Think about what are the awaropriate performance measures to use in this question and why. If your currently holida market index portfolio, what would be the alpha for Portfolios A? depth kat should be indicated by a minus sien. Do not round intermediate calculations. Enter your answer as a decimal rounded to a decimal place ODOS Question 2 3 pts Aportfolio marr Swizes the input from the macro and micro forecasts in the following table Micro Forecasts As Stock Stock Expected Return 20 18 Beta 1.50 2.00 Residual Standard Deviation 60 40 Macro Forecasts Expected Return Standart Deviation 10 Tbil Pane Et Portfolio 16 25 quizze/TAMO Question 2 3 pts A portfoto manager summarizes the input from the macro and micro forecasts in the folowing tables Micro Forecasts Asset Stock SOLB Expected Retum 20 18 Heta 1.50 2.00 Residual Standard Deviation 60 40 Macro Forecasts Asset T-bis Passive Fruity Portfolio Experlod Robin W 5 Standard DeWation (4) 0 125 16 Calculate expected excess returns for stock A Instruction Enter your answer as a decimal(rounded to four decimal places) for expected excess return and alpha values 015 Question 3 3 pts portfolio Manager an the input from the macro and micro forecasts in the following table 3 pts Question 3 A portfolio manager summarizes the input from the macro and micro forecasts in the following table: Micro Forecasts Residual Standard Deviation (%) 60 Asset Stock Stock Expected Return 120 18 Beta 1.50 200 40 Macro Forecasts Expected Return (%) Standard Deviation 5 Assel bill Passive Equity Portfolio Im 0 25 16 Calculate expected excess returns for stock Instruction Enter your answer as a decimal rounded to four decimal places for expected excess returns and alpha values 3 pts Question 4 Question 4 3 pts A portfolio manager summarizes the input from the macro and micro forests in the following table Micro Forecasts Asset Stock Stock B Expected Return 20 Beta 1.50 2.00 Residual Standard Deviation () 60 40 18 Macro Forecasts Expected Return 5 T-bills Passive Equity Portfolini Standard Deviation IN 10 25 16 Calculate expected alph values for stockA Instruction Enter your answer as a decimal rounded to four decimal places for expected excess returns and alpha values Question 5 pts 3 pts Question 5 A portfolio Manager Smarbete inout from the macro and micro forecasts in the following table Micro Forecast Residual Standard Dviation 160 StockA Stock Expected Rum 20 18 150 2.00 40 Macro Forecasts Expected Return (943 Standard Deviation 16 Passive Equity Portfolio 25 Calculate expected alpha values torstock Instruction Enter your answer decimal rounded to four decimal places for expected excess oluns and alpha values -0.00 Question & 3 pts Acortoll manager one the input from the macro and micro forecasts in the following tole: Question 6 3 pts A portfolio Manager summarizes the input from the macro and micro forecasts in the following table: Micro Forecasts Asset Expected Return 20 18 Beta 11.50 Stock Stock B Residual Standard Deviation (6) 80 2.00 40 Macro Forecasts Asset Expected Return 5 16 Standard Deviation 0 25 Passive Equity Portfolium Collate expected residual variances for stock A Tastruction Enter your answer is a decimal(ounded to two decimal places for expected excess retums and alpha values 0:36 Question 3 pts Question 7 3 pts A portfolio manager summarizes the input from the macro and micro forecasts in the following tables Micro Forecasts Bela Asset Stock Expected Return (M) 20 18 Residual Standard Deviation 60 1.50 2.00 Stock B 40 Macro Forecasts Asset Thins Passive Equity Portfolio (m) Expected Return 5 Standard Deviation (9) 0 25 16 Cate expected residua variances for stock B Instruction Enter your answer as a decimal rounded to two decimal places for expected excess returns and alpha valors. 18 Question 3 pts Question 10 3 pts Based on intent dividend yields and expected capitales, the rates of return on folios A and B are 9.5% and 12.5%, respectively. The beta of As.. While al Bis 17 The T-biltrate is currently 5%, while the expected rate of return of the S&P 500 indekis 10%. The standard deviation of portfolio Ais 15% annually. While that of Bis 36% and that of the index 25%. Think about what are the appropriate performance measures to use in this.estion and why If you currently Ivod a market index portfolio, who would be the alpha tor Portfolio B? Negative value should be indicated by a minus sien. Do not round intermediate clowns. Enter your answers a decimal rounded to 3 decimal pixel 001 Question 11 3 pts Based on current dividend yields and expected capital, the expected rates of return on portfolios A and B are 95 and 12.5%, respectively. The heat of AB, while that of B 17. The Twill rate rently 5 while the expectedyate of return of the S&P 500 ind is 10%. The standard deviation of portfolio Als 15% annually, while that of Bis 36%, and that of the indet i 25% If instead you could investoints and one of these portfolios Kakulate the shape measure for Portal (Enter your awer as a decimal rounded to decimal places) Da Question 12 3 pts Based on current dividend yields and expected capital gains, the expected rates of return on portfolios A and B 95% und 12.5%, respectively. The beta of Ais while of Bis 1.7. The T-bill rate is currently 5%, while the expected rate of return of the S&P 500 Index is 10%. The standard deviation of portfolio Al 15% aneilly, while that of Rs 30 and that of the index is 25% It instead you could invest only in hills and one of these portfolios, calcite the shape masure for Portfolio B Enter your answer as a decimal rounded to 2 decimal places Question 13 5 pts Consider the following information marding the performance of money manager in a recent mon the table pracants the actual return of each sector of the managers portfolio in column (Al. Une fraction of the portfolio located to each sector in column 121 the benchmark or neutral sector allocations in column, and the return of vector idees in com 14) ( (3) 121 Artual Benchmark Return Welcht 0.70 Weight 0.50 2.1% 142 Indes Reum 39% S&P 500 28 Agate Bond Inden 1.9 Bonds 26 0.10 00 1.4 0.20 0.20 Question 13 pts Consider the following infomutogarding the performance of a money manager in a recent month The table presents the actual return of each sector of the man par Holio in column the fraction of the portfolio sliecated to each sex in Cokim (2. the benchmark or neutral sector allocations com and the returns al sector indexes incolumn 12 4) Act Art Index (3) Benchmark Weight 0.50 Return 31% Weight 0.70 ty Bonde 2.6 0.10 0.30 3.99 (SSP 5001 2. Agregate Band Inicent 1.9 Cash 1.9 0.20 0.20 Wiut was the man's return the mont? Do not found intermediate calculations. Enter your answer as a decimal rounded to 4 decimal places) 1012 Question 14 5 pts re Question 14 5 pts Consider the following information regarding the performance of money manager in a recent month. The table presents the actual return of each sector of the managers portfolio con the fraction of the porto allocated to each sector in column (2) the benchmark or neutral sector a locations in charm 3 and the returns to sector de calumn 4) 0 12 ca) 44) Actu Actiu Benchmark Index Return Return Wout 0:20 Equity 050 Bonde 12.6 0.10 030 3.9% S&P SOON 2.8 (Aggregate Hand Indeld 1.9 Cash 119 0.20 0.20 What wen het weer under performance Enter a positive value for over performance or a negative value (using a mission for under-erformance. Do not found intermediate calculations. Enter your niwer as a decimal rounded to 4 decimal places 0.000 Question 15 5 pts Question 15 5 pts Consider the blowing information wing the performance of a money manager in a recent month Twitable presents the actual return of each sector of the margar's portfolio income lachten of the portfolio allocated to each sector in column 2 the benchmark or neutr sector allocations in column 131, and the retums of sector inde inculum 141 (1) X21 3 14) Actu Actual Index Return Weight 0.70 Benchmak Weight 0.50 Equity 30196 Return 3.9% S&P 500 2.8 Arte Bond Index 1.9 Bonds 2.6 0.10 0.30 Cash 1.0 020 0.20 What the contribution of security selection relative performance? Here security selection includes security Selection from both couity and bond Negative value should be in cated by a mission. Do not round intermediate calculations Enter your answer as a decimal rounded to 4 decimal places 0.0050 Question 16 5 pts a actor of the 720 Question 16 S pts Consider the following information reparding the performance of a money manager in a recret month. The table presents the actual return of sach sector of the per's portfolio in colonisation of the portfolio allocated to each sector in coluna (2the benchmark or neutral sector allocations in column (3) and the returns of sector indexes in column (4) 1) 123 3) 14) Ac Adil Benchmark Index Reum Weight Return Wright 0.70 Equity 3.1% 0.50 Bonds 26 0:10 0.36 9 SEP 5001 2. Agregate Bond Index 19 11. 0.20 0,20 What was the contration of asset allocation to relative performance (Do not round intermediate calculations. Enter your answer as a decimal rounded to 4 decimal places 0.0002 Question 17 6 pts BAI Smith is evakuating the performance of our large cap equity portfolios tunds A B.Card D. As part of his analysis. Smith computed the Sharp ratio and the Teymon measure for all lour fonds. Based on his finding the minklassigned to the fou funds are as follow Flind They not Measure Sharpe Ratio 4 1 is a 3 B 2 G 2 1 D 4 The difference in rankings of funds and based on the Sharp ratio and the Traynor measte is most likely due to Adwenerisk Der er to teach funt perfor Aladdition in fundarned to Delication in and Day home to tund O noun Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: J. Chris Leach, Ronald W. Melicher

7th Edition

0357442040, 978-0357442043