Answered step by step

Verified Expert Solution

Question

1 Approved Answer

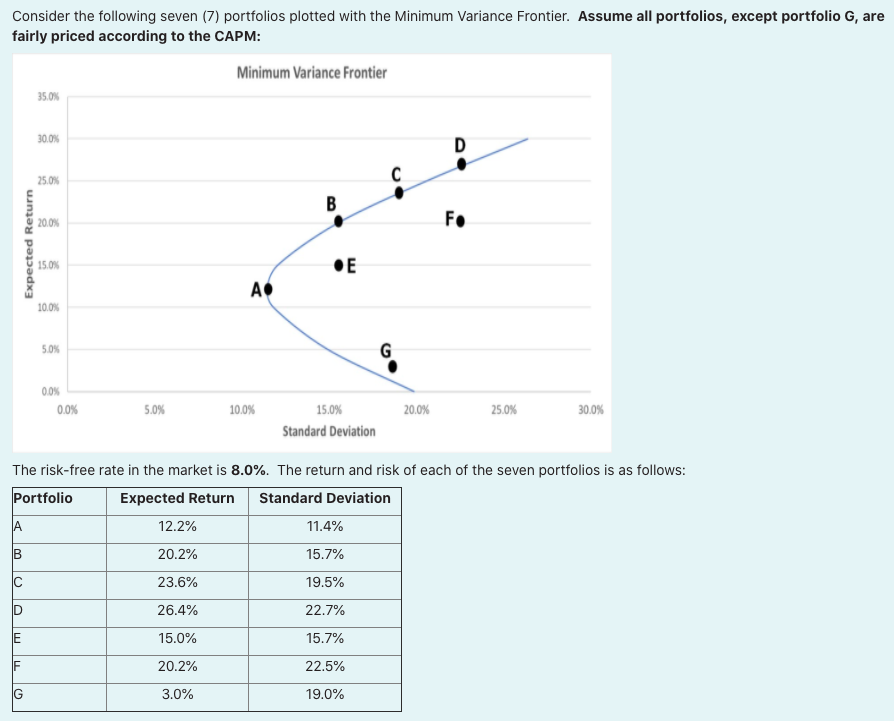

i) Assume that one of these portfolio's is the Market Portfolio and all portfolios, except Portfolio G, are fairly priced according to the CAPM.

i) Assume that one of these portfolio's is the Market Portfolio and all portfolios, except Portfolio G, are fairly priced according to the CAPM. In addition assume there is no residual covariance between portfolios. What it is the correlation between Portfolio E and Portfolio F? (2 marks) Enter your answer to 3 decimal places eg if your answer is 0.4776 enter as 0.478. Consider the following seven (7) portfolios plotted with the Minimum Variance Frontier. Assume all portfolios, except portfolio G, are fairly priced according to the CAPM: A B C D E IF Expected Return G 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% 0.0% 5.0% Minimum Variance Frontier 12.2% 20.2% 23.6% 26.4% 15.0% 20.2% 3.0% A 10.0% B E 15.0% Standard Deviation C 11.4% 15.7% 19.5% 22.7% 15.7% 22.5% 19.0% G 20.0% D The risk-free rate in the market is 8.0%. The return and risk of each of the seven portfolios is as follows: Portfolio Expected Return Standard Deviation Fo 25.0% 30.0%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

1 One of the portfolios on the efficient frontier must be the market portfolio Lets assu...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Corporate Finance

Authors: Aswath Damodaran

4th edition

978-1-118-9185, 9781118918562, 1118808932, 1118918568, 978-1118808931