Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I can't figure out the following amounts: - CPP enhanced contributions - Moving Meals & vehicle (simplified Method) Everything else is correct, I checked. In

I can't figure out the following amounts:

I can't figure out the following amounts:

- CPP enhanced contributions

- Moving Meals & vehicle (simplified Method)

Everything else is correct, I checked.

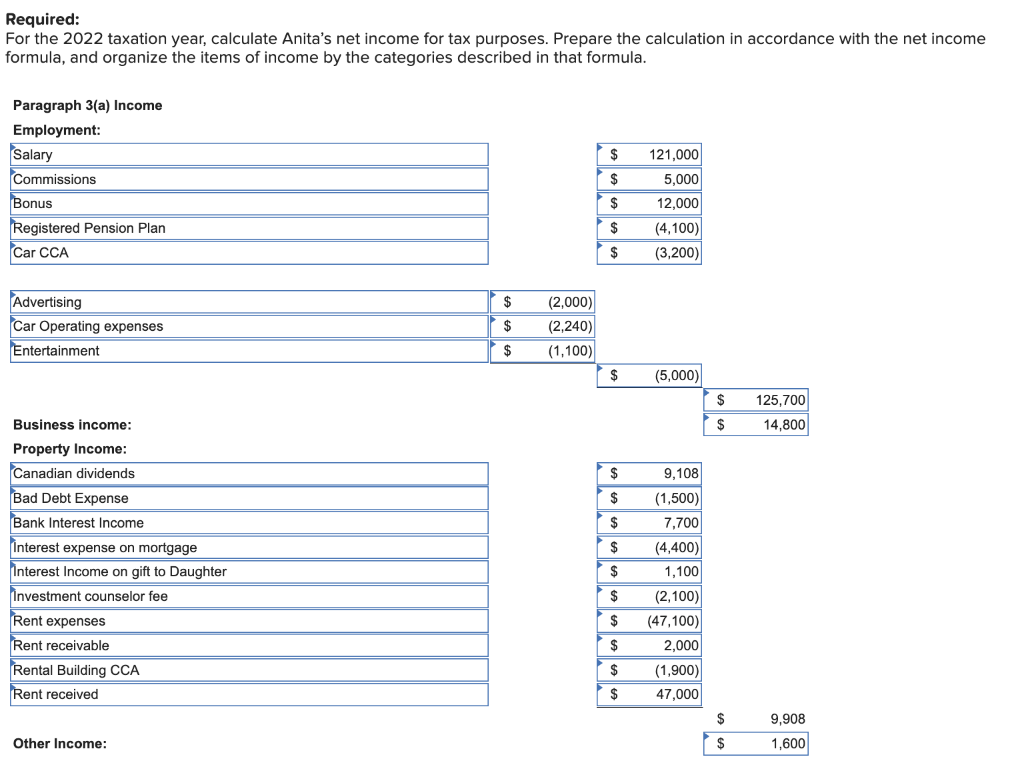

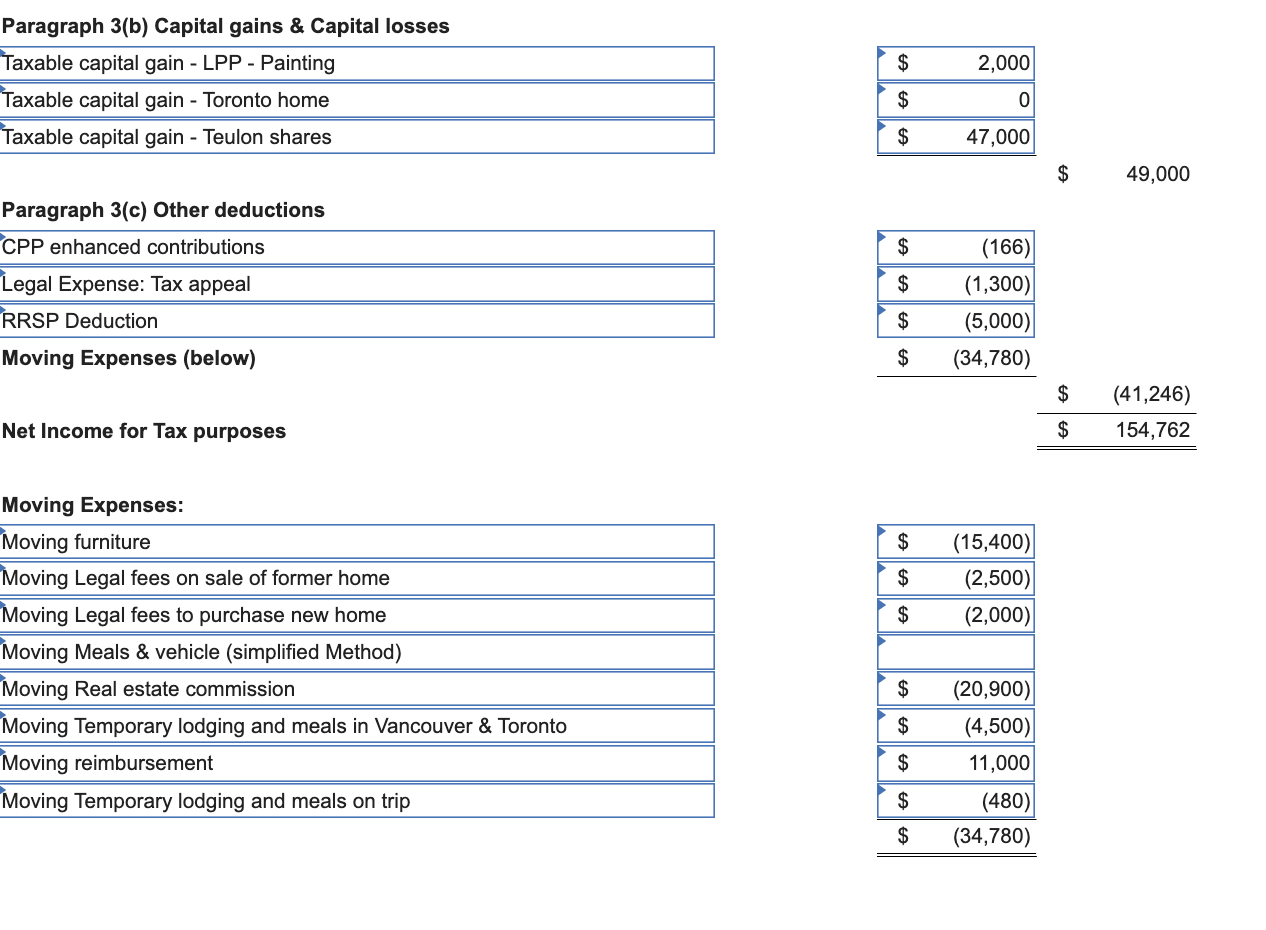

In 2022, Anita Poirier was transferred by her employer to Vancouver from Toronto. She has made a number of financial transactions related to the move. Anita has asked you for help in determining her 2022 income for tax purposes. She has provided the following information: 1. Anita is divorced and supports her two children Lise (aged 17) and Randy (aged 19). In the summer, Randy earned net profits of $4,000 as a street vendor. Lise's only source of income was from an investment purchased for her by her mother. The investment, bonds of a Canadian public corporation, paid interest of $1,100 during the year. 2. Anita began work in Vancouver in February 2022 as a senior sales associate for a clothing manufacturer. During the year, she received a gross salary of $121,000 as well as selling commissions of $5,000. In addition, on June 30 , her employer's year-end, she was awarded a bonus of $24,000 payable in 12 monthly instalments of $2,000 beginning July 31,2022 . She contributed $4,100 to the company's registered pension plan, and her employer contributed the same amount. She also paid $3,500 to the Canada Pension Plan and made Employment Insurance contributions of $953. 3. Anita's employer has certified that she is required to pay some of her own expenses as part of her selling duties. She incurred the following costs: Anita uses her own car for business activities. At the end of 2021 , the car had an undepreciated capital cost of $20,000. In 2022 , she drove the car 30,000km, of which approximately 14,000Km were for personal use. She acquired a computer (see table), which she uses at home to maintain customer files and industry information. She estimates that 90% of her computer time is employment related. 4. On January 15,2023 , Anita contributed $7,700 to an RRSP. On the same date she contributed $4,400 to a TFSA. For the 2021 taxation year, her earned income was $63,889. In 2021, the combined (employer and employee) contribution to her employer RPP was $6,500. 5. Anita drove herself and her two children from Toronto to Vancouver. The 4,400- km trip took five days and cost $400 for gasoline, $480 for accommodation (four nights), and $500 for meals (five days). As well, she incurred the following relocation costs: Her employer, in accordance with company policy, paid her the maximum $11,000 as a partial reimbursement for transporting furniture to Vancouver. the move to Vancouver. 8. Five years ago, Anita purchased 5% of the common shares of Prentice Ltd. for $20,000. Prentice is a Canadian-controlled private corporation manufacturing specialized furniture. In June 2019, when the company had cash-flow problems, Anita lent Prentice $10,000. The loan was unsecured and payable on demand. Although Anita has received no interest to date, in 2020 and 2021 , she included in her taxable income interest of $1,500($7502y=$1,500) based on the agreed interest rate on each anniversary date. other than the leased manufacturing equipment, were inventory and receivables, which were pledged on a bank loan; these were insufficient to meet even that obligation. In March 2023, Prentice closed operations and declared bankruptcy. 9. Anita sold the followina broberties: The sale of the commodity futures contract was Anita's second commodity transaction. In 2020 , she purchased and sold a similar contract but lost $14,000. She deducted the full $14,000 when computing her 2020 taxable income. 0. Anita owns a residential rental property in Toronto. She acquired the property in 2021 for $414,000 (land - $54,000, building $360,000). She incurred a substantial loss in 2021 as a result of an unexpected vacancy. She found a new tenant in 2022 . She received gross rents of $47,000 in 2022 . Expenses for utilities, taxes, insurance, interest, and maintenance were $47,100 that year. One of the tenants failed to pay their December 2022 rent of $2,100. However, she received that payment on January 20,2023. 11. Anita received the followina additional amounts: 2. Anita hired an investment counsellor. On his recommendation, she used $40,000 of the $200,000 mortgage loan on her new home to acquire Canadian public securities. Her mortgage interest payments totalled $22,000. She paid the investment counsellor $2,100 for his advice. 3. Anita made donations of $4,000 to registered charities. 4. During 2022, Anita's 2020 tax return was reassessed. She hired a lawyer to prepare an appeal. The legal fee was $1,300. The appeal was not successful. Required: F fi 'ance with the net income [ 3 Paragraph 3(b) Capital gains \& Capital losses \begin{tabular}{l} Taxable capital gain - LPP - Painting \\ \hline \hline Taxable capital gain - Toronto home \\ \hline \hline Taxable capital gain - Teulon shares \\ \hline \end{tabular} \begin{tabular}{|lr|} \hline$ & 2,000 \\ \hline$ & 0 \\ \hline$ & 47,000 \\ \hline \hline \end{tabular} Paragraph 3(c) Other deductions CPP enhanced contributions Legal Expense: Tax appeal RRSP Deduction Moving Expenses (below) $49,000 Net Income for Tax purposes \begin{tabular}{|rr|} \hline$ & (166) \\ \hline \hline$ & (1,300) \\ \hline \hline$ & (5,000) \\ \hline$ & (34,780) \\ \hline \end{tabular} Moving Expenses: Moving furniture Moving Legal fees on sale of former home Moving Legal fees to purchase new home Moving Meals \& vehicle (simplified Method) Moving Real estate commission Moving Temporary lodging and meals in Vancouver \& Toronto Moving reimbursement Moving Temporary lodging and meals on trip \begin{tabular}{ll} $ & (41,246) \\ \hline$ & 154,762 \\ \hline \hline \end{tabular} \begin{tabular}{|lr|} \hline$ & (15,400) \\ \hline$ & (2,500) \\ \hline$ & (2,000) \\ \hline & \\ \hline$ & (20,900) \\ \hline$ & (4,500) \\ \hline \hline$ & 11,000 \\ \hline$ & (480) \\ \hline \hline$ & (34,780) \\ \hline \hline \end{tabular} In 2022, Anita Poirier was transferred by her employer to Vancouver from Toronto. She has made a number of financial transactions related to the move. Anita has asked you for help in determining her 2022 income for tax purposes. She has provided the following information: 1. Anita is divorced and supports her two children Lise (aged 17) and Randy (aged 19). In the summer, Randy earned net profits of $4,000 as a street vendor. Lise's only source of income was from an investment purchased for her by her mother. The investment, bonds of a Canadian public corporation, paid interest of $1,100 during the year. 2. Anita began work in Vancouver in February 2022 as a senior sales associate for a clothing manufacturer. During the year, she received a gross salary of $121,000 as well as selling commissions of $5,000. In addition, on June 30 , her employer's year-end, she was awarded a bonus of $24,000 payable in 12 monthly instalments of $2,000 beginning July 31,2022 . She contributed $4,100 to the company's registered pension plan, and her employer contributed the same amount. She also paid $3,500 to the Canada Pension Plan and made Employment Insurance contributions of $953. 3. Anita's employer has certified that she is required to pay some of her own expenses as part of her selling duties. She incurred the following costs: Anita uses her own car for business activities. At the end of 2021 , the car had an undepreciated capital cost of $20,000. In 2022 , she drove the car 30,000km, of which approximately 14,000Km were for personal use. She acquired a computer (see table), which she uses at home to maintain customer files and industry information. She estimates that 90% of her computer time is employment related. 4. On January 15,2023 , Anita contributed $7,700 to an RRSP. On the same date she contributed $4,400 to a TFSA. For the 2021 taxation year, her earned income was $63,889. In 2021, the combined (employer and employee) contribution to her employer RPP was $6,500. 5. Anita drove herself and her two children from Toronto to Vancouver. The 4,400- km trip took five days and cost $400 for gasoline, $480 for accommodation (four nights), and $500 for meals (five days). As well, she incurred the following relocation costs: Her employer, in accordance with company policy, paid her the maximum $11,000 as a partial reimbursement for transporting furniture to Vancouver. the move to Vancouver. 8. Five years ago, Anita purchased 5% of the common shares of Prentice Ltd. for $20,000. Prentice is a Canadian-controlled private corporation manufacturing specialized furniture. In June 2019, when the company had cash-flow problems, Anita lent Prentice $10,000. The loan was unsecured and payable on demand. Although Anita has received no interest to date, in 2020 and 2021 , she included in her taxable income interest of $1,500($7502y=$1,500) based on the agreed interest rate on each anniversary date. other than the leased manufacturing equipment, were inventory and receivables, which were pledged on a bank loan; these were insufficient to meet even that obligation. In March 2023, Prentice closed operations and declared bankruptcy. 9. Anita sold the followina broberties: The sale of the commodity futures contract was Anita's second commodity transaction. In 2020 , she purchased and sold a similar contract but lost $14,000. She deducted the full $14,000 when computing her 2020 taxable income. 0. Anita owns a residential rental property in Toronto. She acquired the property in 2021 for $414,000 (land - $54,000, building $360,000). She incurred a substantial loss in 2021 as a result of an unexpected vacancy. She found a new tenant in 2022 . She received gross rents of $47,000 in 2022 . Expenses for utilities, taxes, insurance, interest, and maintenance were $47,100 that year. One of the tenants failed to pay their December 2022 rent of $2,100. However, she received that payment on January 20,2023. 11. Anita received the followina additional amounts: 2. Anita hired an investment counsellor. On his recommendation, she used $40,000 of the $200,000 mortgage loan on her new home to acquire Canadian public securities. Her mortgage interest payments totalled $22,000. She paid the investment counsellor $2,100 for his advice. 3. Anita made donations of $4,000 to registered charities. 4. During 2022, Anita's 2020 tax return was reassessed. She hired a lawyer to prepare an appeal. The legal fee was $1,300. The appeal was not successful. Required: F fi 'ance with the net income [ 3 Paragraph 3(b) Capital gains \& Capital losses \begin{tabular}{l} Taxable capital gain - LPP - Painting \\ \hline \hline Taxable capital gain - Toronto home \\ \hline \hline Taxable capital gain - Teulon shares \\ \hline \end{tabular} \begin{tabular}{|lr|} \hline$ & 2,000 \\ \hline$ & 0 \\ \hline$ & 47,000 \\ \hline \hline \end{tabular} Paragraph 3(c) Other deductions CPP enhanced contributions Legal Expense: Tax appeal RRSP Deduction Moving Expenses (below) $49,000 Net Income for Tax purposes \begin{tabular}{|rr|} \hline$ & (166) \\ \hline \hline$ & (1,300) \\ \hline \hline$ & (5,000) \\ \hline$ & (34,780) \\ \hline \end{tabular} Moving Expenses: Moving furniture Moving Legal fees on sale of former home Moving Legal fees to purchase new home Moving Meals \& vehicle (simplified Method) Moving Real estate commission Moving Temporary lodging and meals in Vancouver \& Toronto Moving reimbursement Moving Temporary lodging and meals on trip \begin{tabular}{ll} $ & (41,246) \\ \hline$ & 154,762 \\ \hline \hline \end{tabular} \begin{tabular}{|lr|} \hline$ & (15,400) \\ \hline$ & (2,500) \\ \hline$ & (2,000) \\ \hline & \\ \hline$ & (20,900) \\ \hline$ & (4,500) \\ \hline \hline$ & 11,000 \\ \hline$ & (480) \\ \hline \hline$ & (34,780) \\ \hline \hline \end{tabular}Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wiley CPAexcel Exam Review 2018 Study Guide Auditing And Attestation

Authors: Wiley

1st Edition

1119480671, 978-1119480679