Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I cant figure out the standard deviation of portfolio i.e the standard deviation in c) part. PLEASE HELP There are two stocks in the market,

I cant figure out the standard deviation of portfolio i.e the standard deviation in c) part.

PLEASE HELP

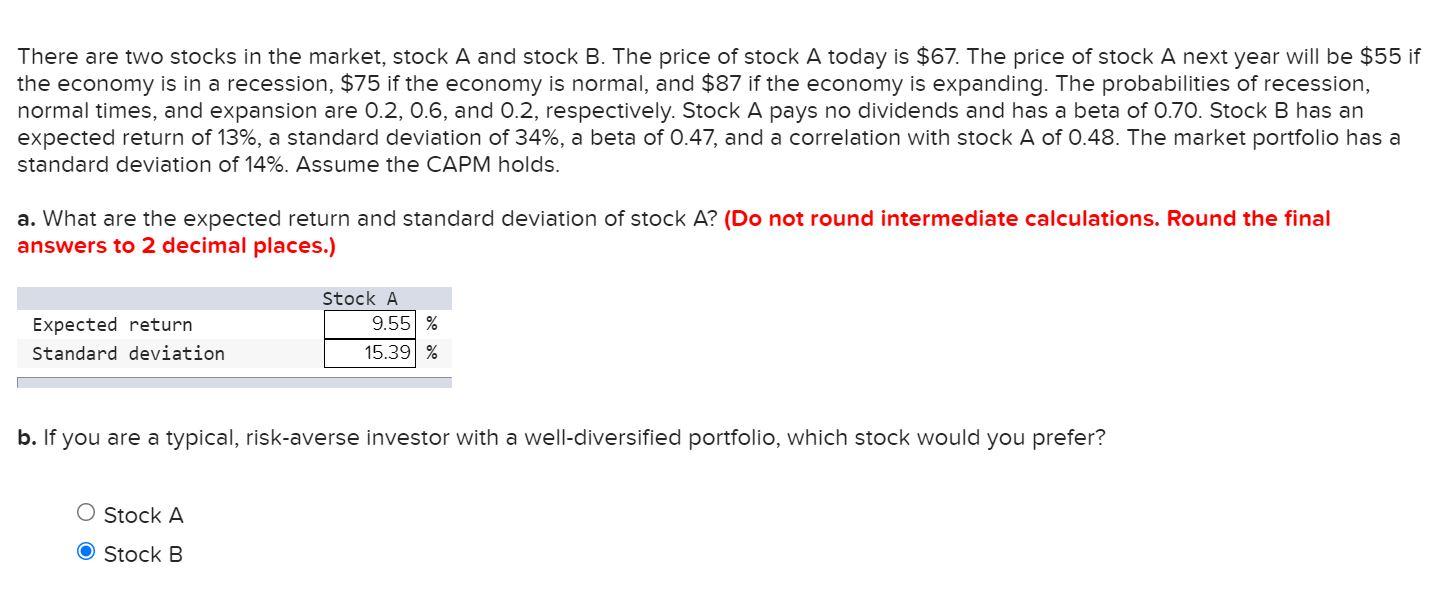

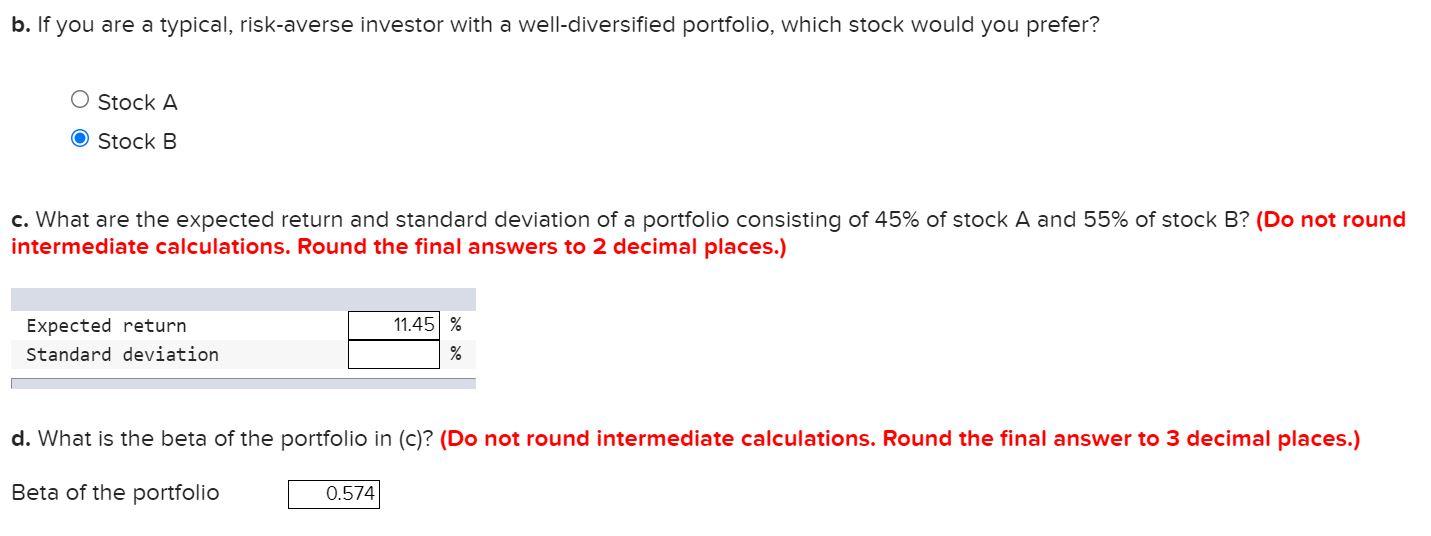

There are two stocks in the market, stock A and stock B. The price of stock A today is $67. The price of stock A next year will be $55 if the economy is in a recession, $75 if the economy is normal, and $87 if the economy is expanding. The probabilities of recession, normal times, and expansion are 0.2, 0.6, and 0.2, respectively. Stock A pays no dividends and has a beta of 0.70. Stock B has an expected return of 13%, a standard deviation of 34%, a beta of 0.47, and a correlation with stock A of 0.48. The market portfolio has a standard deviation of 14%. Assume the CAPM holds. a. What are the expected return and standard deviation of stock A? (Do not round intermediate calculations. Round the final answers to 2 decimal places.) Expected return Standard deviation Stock A 9.55 % 15.39% b. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? O Stock A O Stock B b. If you are a typical, risk-averse investor with a well-diversified portfolio, which stock would you prefer? O Stock A Stock B c. What are the expected return and standard deviation of a portfolio consisting of 45% of stock A and 55% of stock B? (Do not round intermediate calculations. Round the final answers to 2 decimal places.) Expected return Standard deviation 11.45 % % d. What is the beta of the portfolio in (c)? (Do not round intermediate calculations. Round the final answer to 3 decimal places.) Beta of the portfolio 0.574Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurship In Finance Successfully Launching And Managing A Hedge Fund In Asia

Authors: Henri Arslanian

1st Edition

331943912X,3319439138