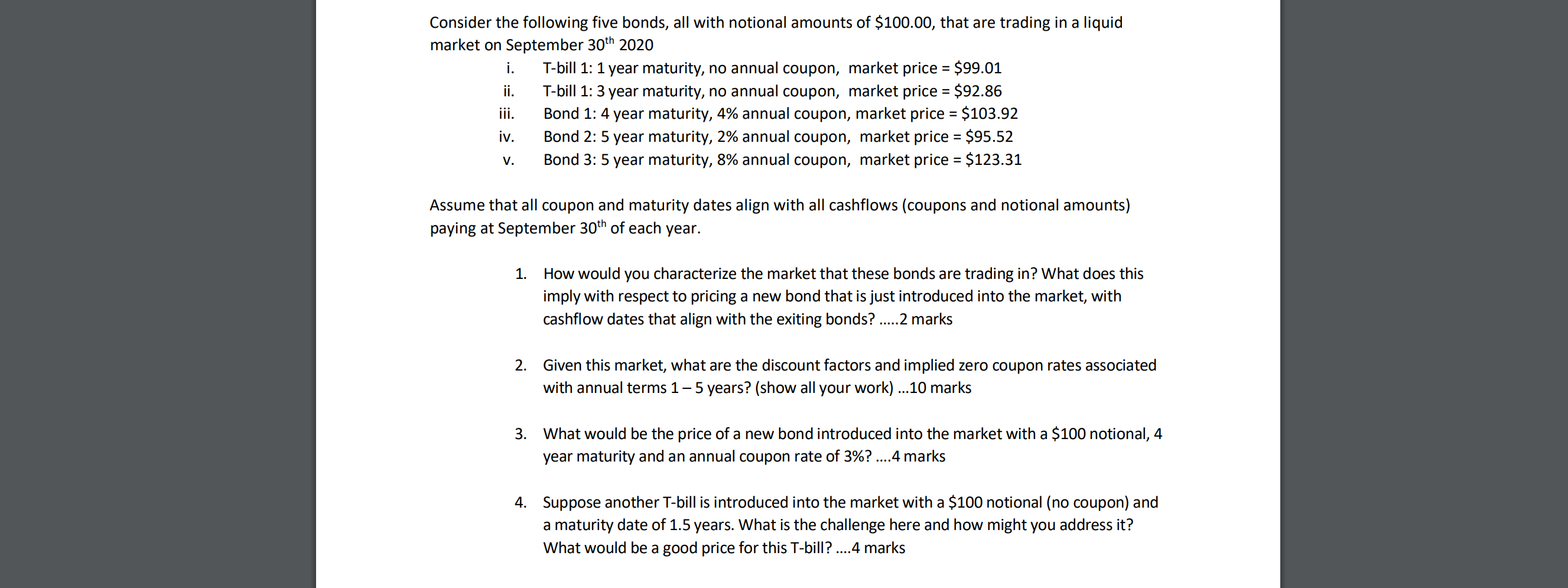

i. Consider the following five bonds, all with notional amounts of $100.00, that are trading in a liquid market on September 30th 2020 T-bill 1: 1 year maturity, no annual coupon, market price = $99.01 ii. T-bill 1: 3 year maturity, no annual coupon, market price = $92.86 iii. Bond 1: 4 year maturity, 4% annual coupon, market price = $103.92 iv. Bond 2: 5 year maturity, 2% annual coupon, market price = $95.52 Bond 3: 5 year maturity, 8% annual coupon, market price = $123.31 V. Assume that all coupon and maturity dates align with all cashflows (coupons and notional amounts) paying at September 30th of each year. 1. How would you characterize the arket that these bonds are trading in? What does this imply with respect to pricing a new bond that is just introduced into the market, with cashflow dates that align with the exiting bonds? .....2 marks 2. Given this market, what are the discount factors and implied zero coupon rates associated with annual terms 1 5 years? (show all your work) ...10 marks 3. What would be the price of a new bond introduced into the market with a $100 notional, 4 year maturity and an annual coupon rate of 3%? ....4 marks 4. Suppose another T-bill is introduced into the market with a $100 notional (no coupon) and a maturity date of 1.5 years. What is the challenge here and how might you address it? What would be a good price for this T-bill? ....4 marks i. Consider the following five bonds, all with notional amounts of $100.00, that are trading in a liquid market on September 30th 2020 T-bill 1: 1 year maturity, no annual coupon, market price = $99.01 ii. T-bill 1: 3 year maturity, no annual coupon, market price = $92.86 iii. Bond 1: 4 year maturity, 4% annual coupon, market price = $103.92 iv. Bond 2: 5 year maturity, 2% annual coupon, market price = $95.52 Bond 3: 5 year maturity, 8% annual coupon, market price = $123.31 V. Assume that all coupon and maturity dates align with all cashflows (coupons and notional amounts) paying at September 30th of each year. 1. How would you characterize the arket that these bonds are trading in? What does this imply with respect to pricing a new bond that is just introduced into the market, with cashflow dates that align with the exiting bonds? .....2 marks 2. Given this market, what are the discount factors and implied zero coupon rates associated with annual terms 1 5 years? (show all your work) ...10 marks 3. What would be the price of a new bond introduced into the market with a $100 notional, 4 year maturity and an annual coupon rate of 3%? ....4 marks 4. Suppose another T-bill is introduced into the market with a $100 notional (no coupon) and a maturity date of 1.5 years. What is the challenge here and how might you address it? What would be a good price for this T-bill? ....4 marks