Question

I do not know if this is the best example, but I am confused by how the COGS are calculated . I see the 2

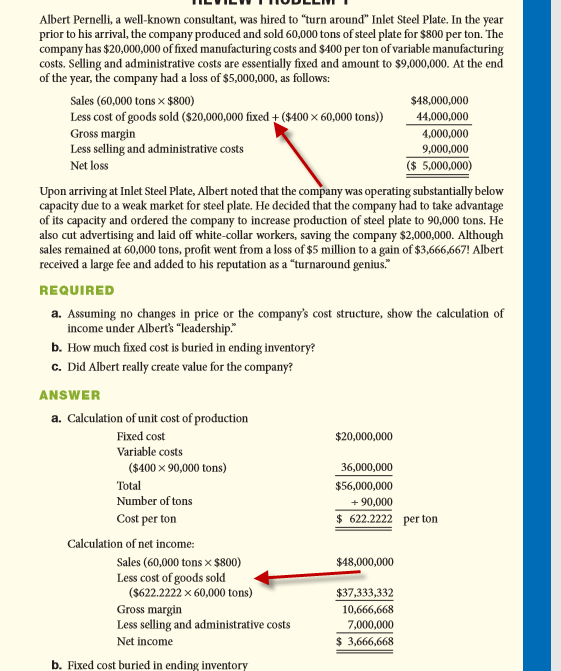

I do not know if this is the best example, but I am confused by how the COGS are calculated . I see the 2 different ways noted on the image I attached (screenshot attached) but why is only part of the fixed costs including in the first part?

I also thought COGS had to be figured out by knowing cost of beg inventory + cost of purchases - cost of ending inventory ?

And speaking of ending inventory, does that mean if a company produced 100 items, for example, but they only sold 80, does that mean there will be 20 left in ending inventory? I still get confused by that stuff from Chapter 3 process costing i believe.

Thank you

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

College Accounting A Practical Approach

Authors: Jeffrey Slater, Debra Good

13th Canadian edition

134616316, 134166698, 9780134632407 , 978-0134166698