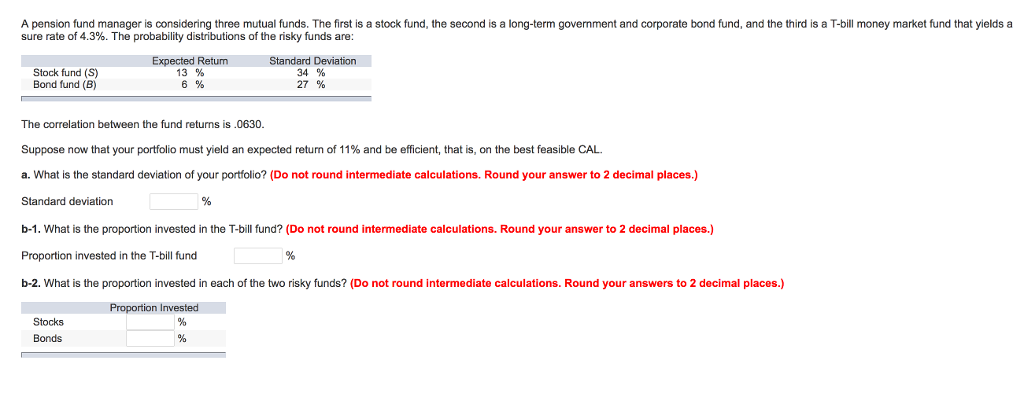

Question

I have been working on this one problem for 2 days now and I still cannot figure it out. I have completed the rest of

I have been working on this one problem for 2 days now and I still cannot figure it out. I have completed the rest of the Chapter assignments I have looked at similar problems here on Chegg, and I just cannot even solve this one. Any help with understanding how to complete this problem will be geatly appreciated!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Futures And Other Derivatives

Authors: John C. Hull

3rd Edition

0131864793, 9780306457555