Question

I have following two questions: 1.Consider a bond that promises to pay coupons annually for 10 years. The face value is $1000. The riskfree rate

I have following two questions:

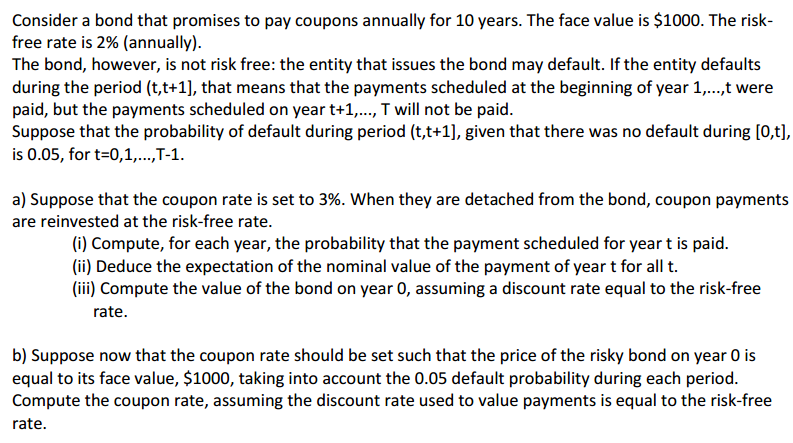

1.Consider a bond that promises to pay coupons annually for 10 years. The face value is $1000. The riskfree rate is 2% (annually). The bond, however, is not risk free: the entity that issues the bond may default. If the entity defaults during the period (t,t+1], that means that the payments scheduled at the beginning of year 1,...,t were paid, but the payments scheduled on year t+1,..., T will not be paid. Suppose that the probability of default during period (t,t+1], given that there was no default during [0,t], is 0.05, for t=0,1,...,T-1.

a) Suppose that the coupon rate is set to 3%. When they are detached from the bond, coupon payments are reinvested at the risk-free rate.

(i) Compute, for each year, the probability that the payment scheduled for year t is paid.

(ii) Deduce the expectation of the nominal value of the payment of year t for all t.

(iii) Compute the value of the bond on year 0, assuming a discount rate equal to the risk-free rate. b) Suppose now that the coupon rate should be set such that the price of the risky bond on year 0 is equal to its face value, $1000, taking into account the 0.05 default probability during each period. Compute the coupon rate, assuming the discount rate used to value payments is equal to the risk-free rate.

b) Suppose now that the coupon rate should be set such that the price of the risky bond on year 0 is equal to its face value, $1000, taking into account the 0.05 default probability during each period. Compute the coupon rate, assuming the discount rate used to value payments is equal to the risk-free rate.

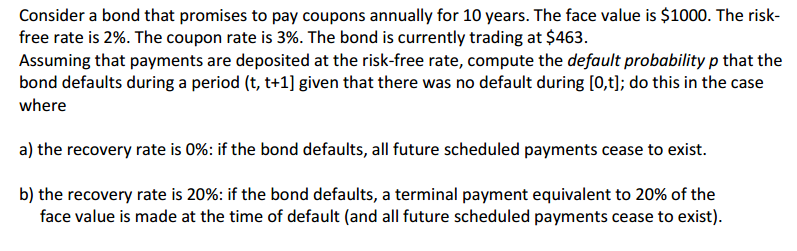

2.Consider a bond that promises to pay coupons annually for 10 years. The face value is $1000. The riskfree rate is 2%. The coupon rate is 3%. The bond is currently trading at $463. Assuming that payments are deposited at the risk-free rate, compute the default probability p that the bond defaults during a period (t, t+1] given that there was no default during [0,t]; do this in the case where a) the recovery rate is 0%: if the bond defaults, all future scheduled payments cease to exist. b) the recovery rate is 20%: if the bond defaults, a terminal payment equivalent to 20% of the face value is made at the time of default (and all future scheduled payments cease to exist).

Here is the pics of there two questions. Thanks!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Pairs Trading

Authors: Douglas S. Ehrman

1st Edition

0471727075, 9780471727071