I have problems 1, 2b and 3a done, but I really need help with understanding the long-run graphs of the industry(sometimes also called market) supply

I have problems 1, 2b and 3a done, but I really need help with understanding the long-run graphs of the industry(sometimes also called market) supply and demand curve and the long-run cost curves. I'm also really confused on number 5 and don't know where to start with that. I've attached pictures of the problems and some pages of my textbook concerning long-run graphs.

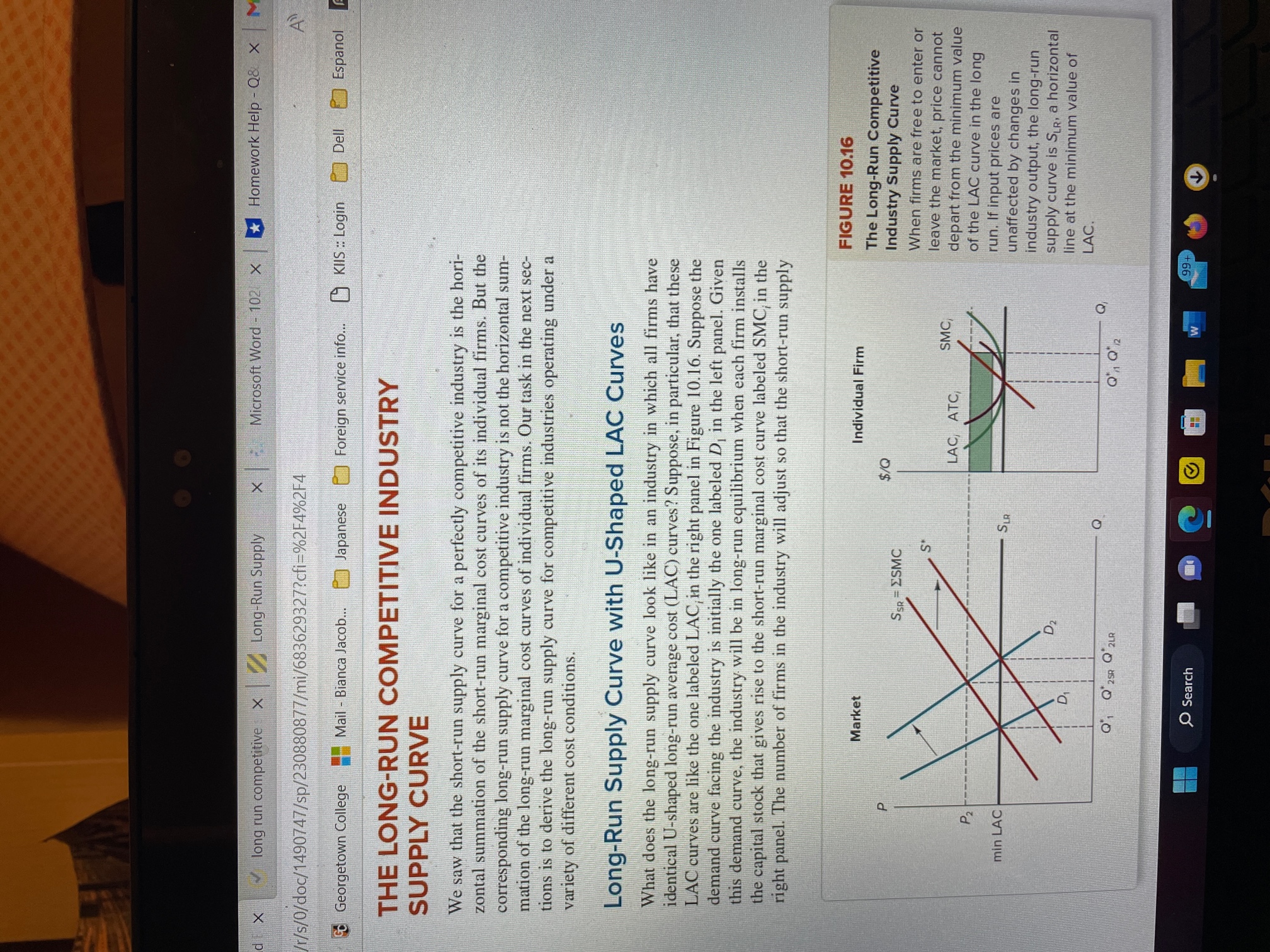

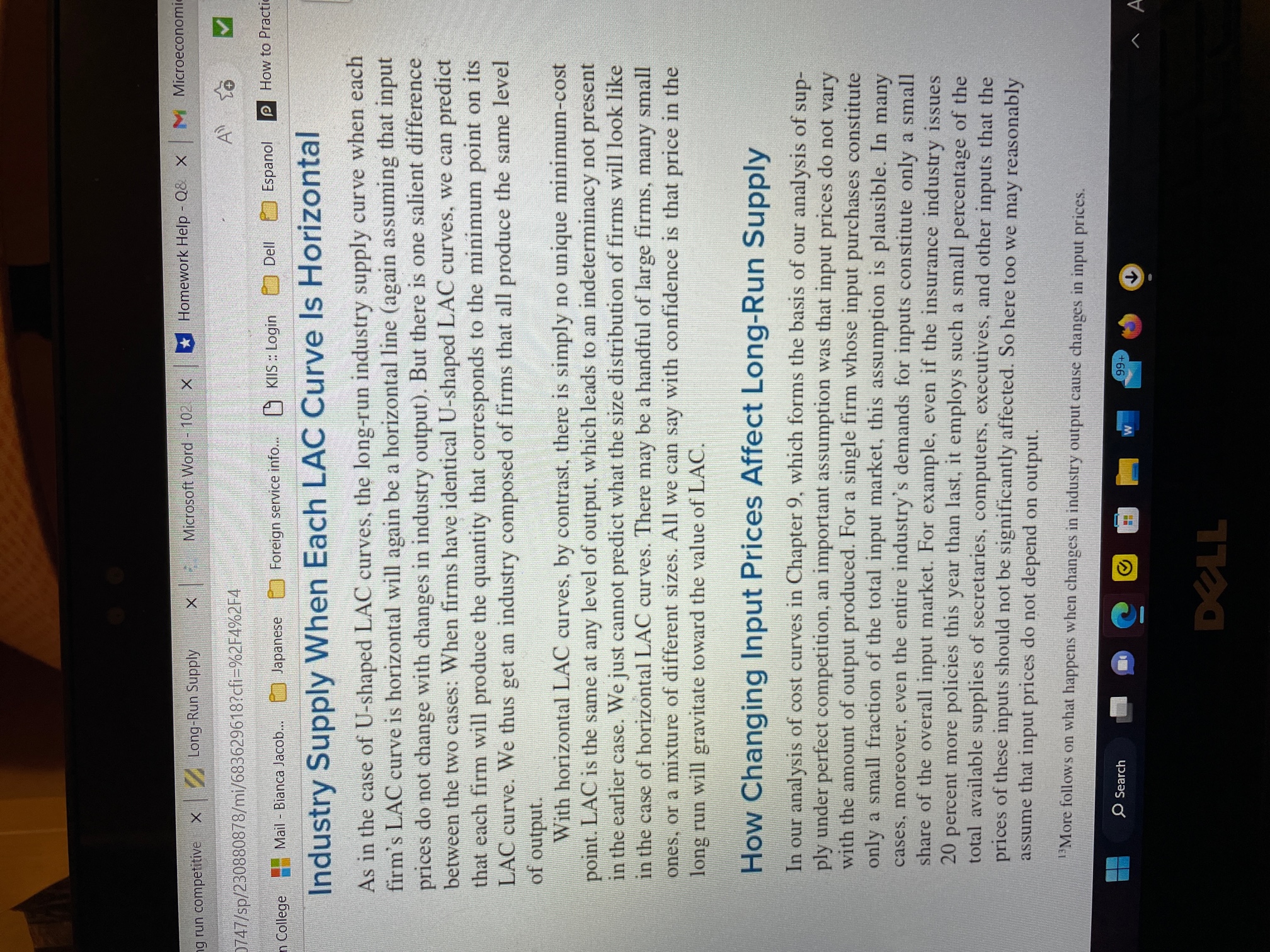

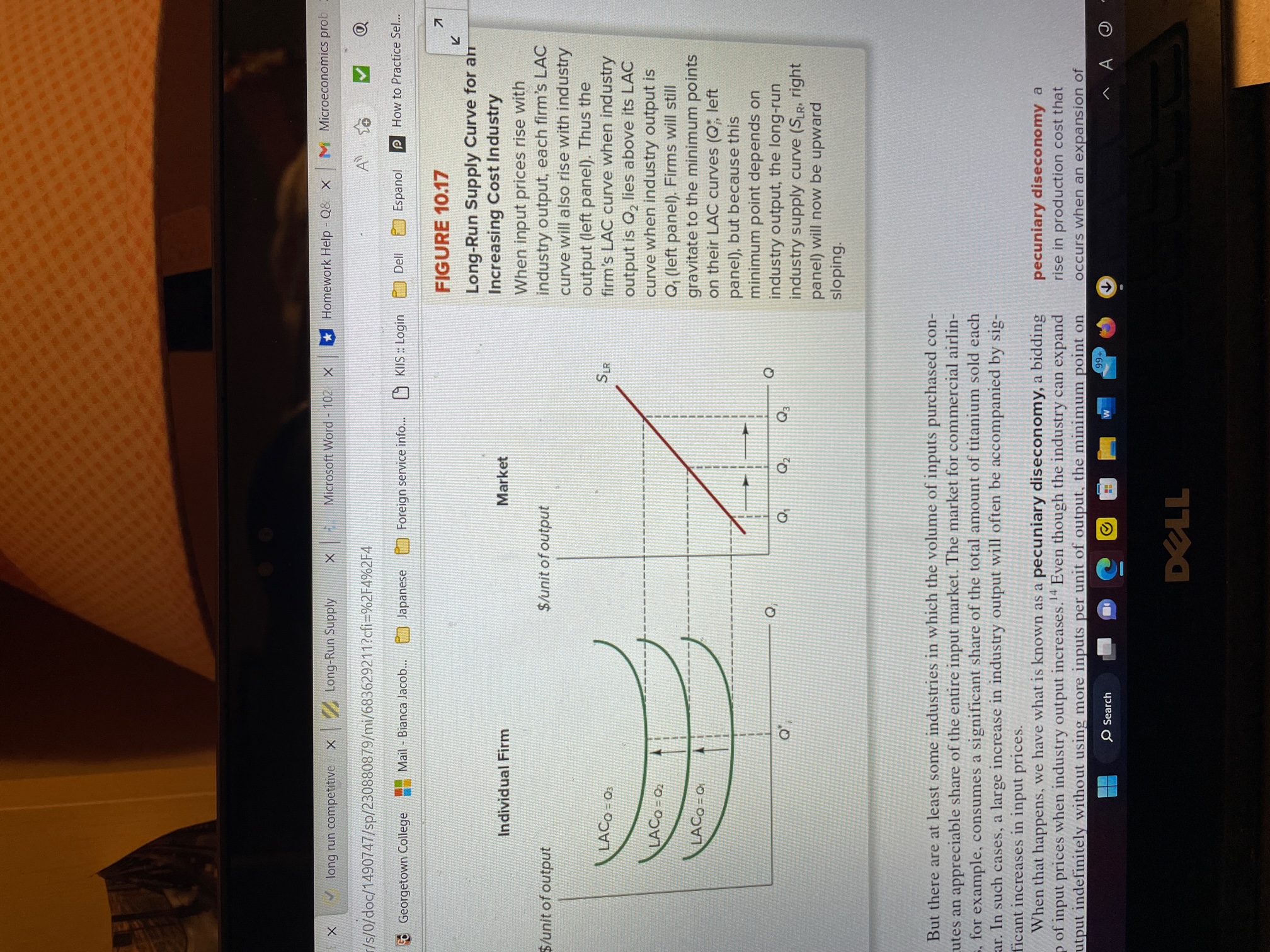

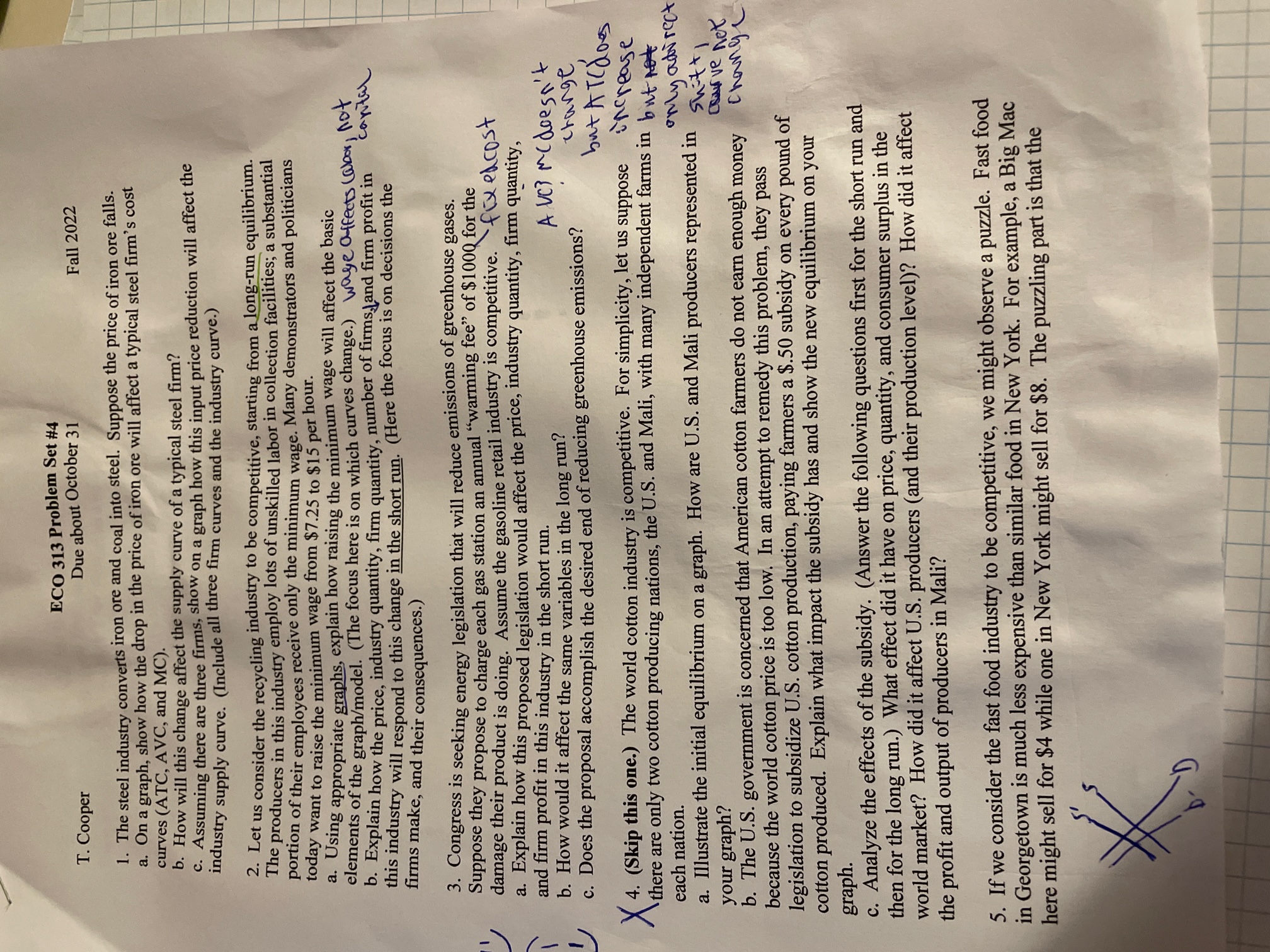

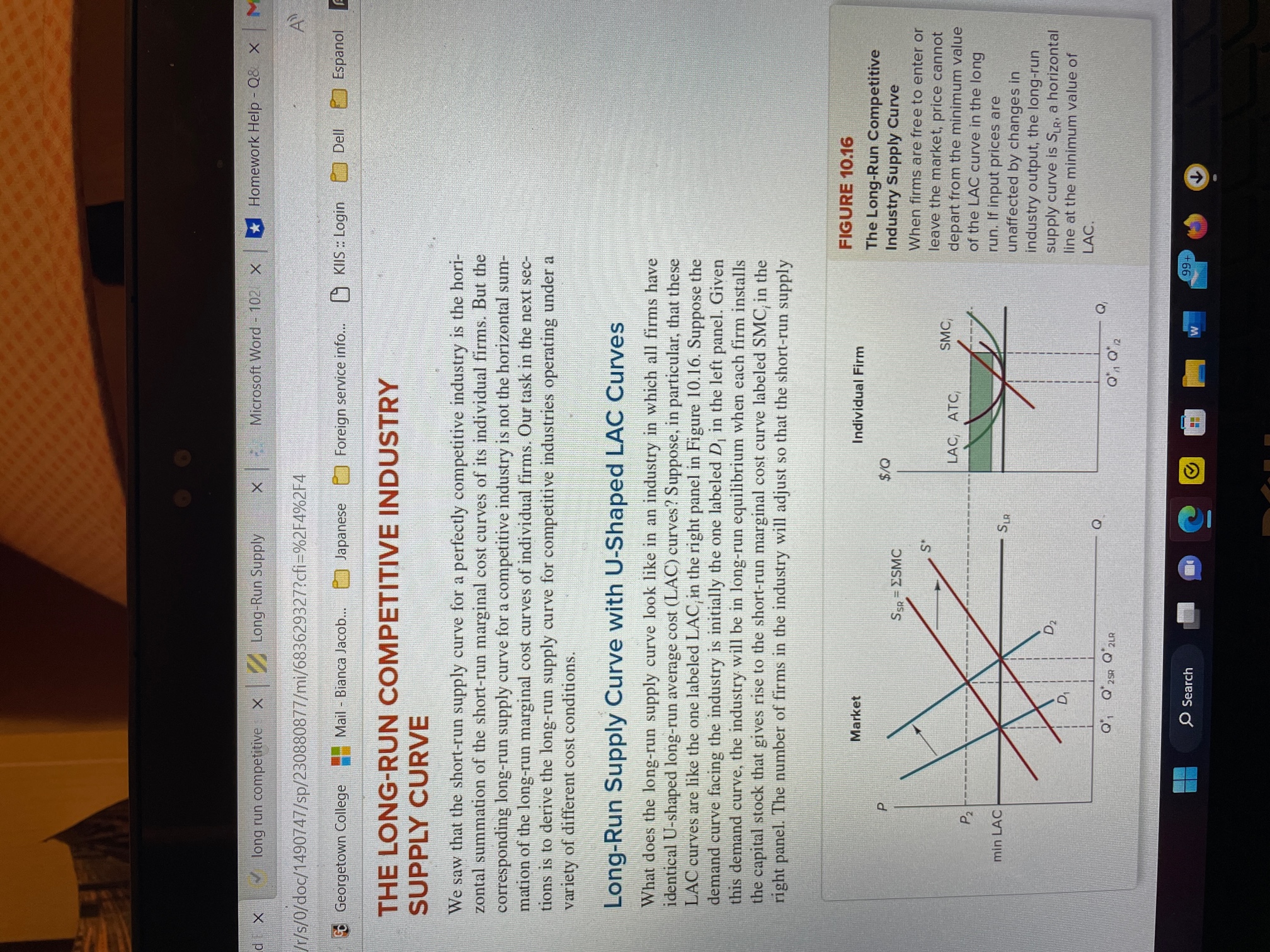

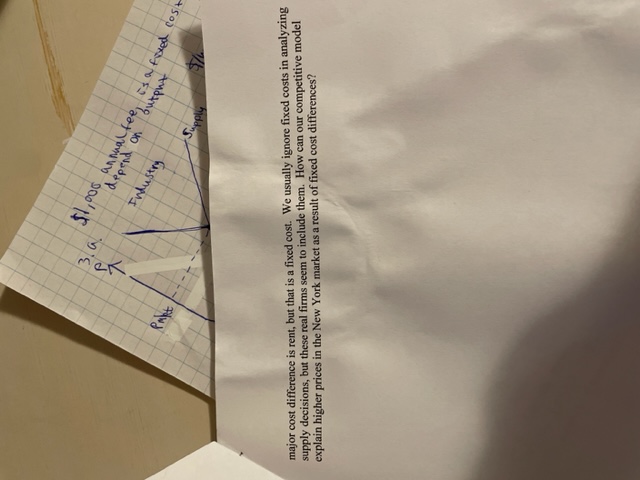

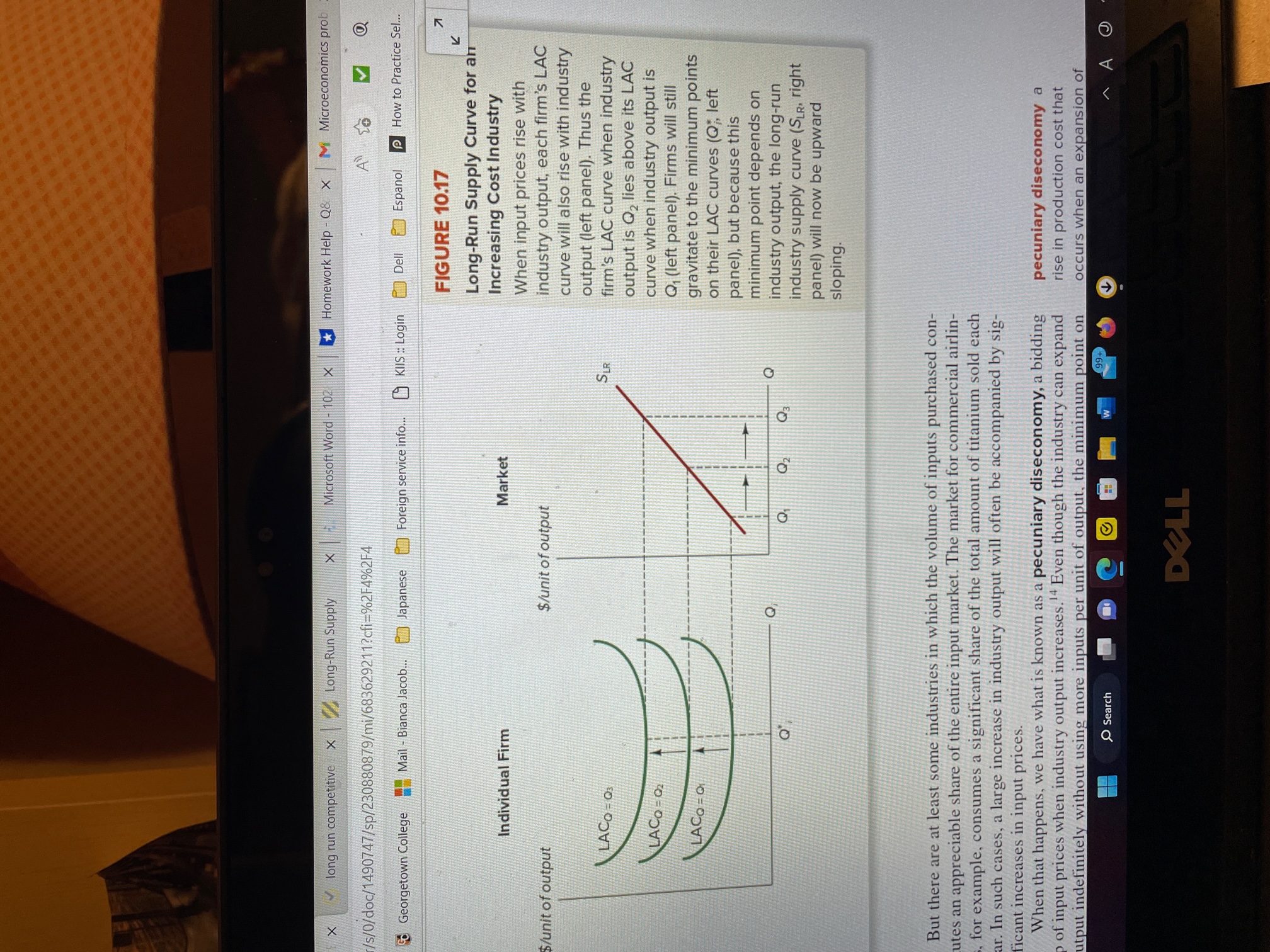

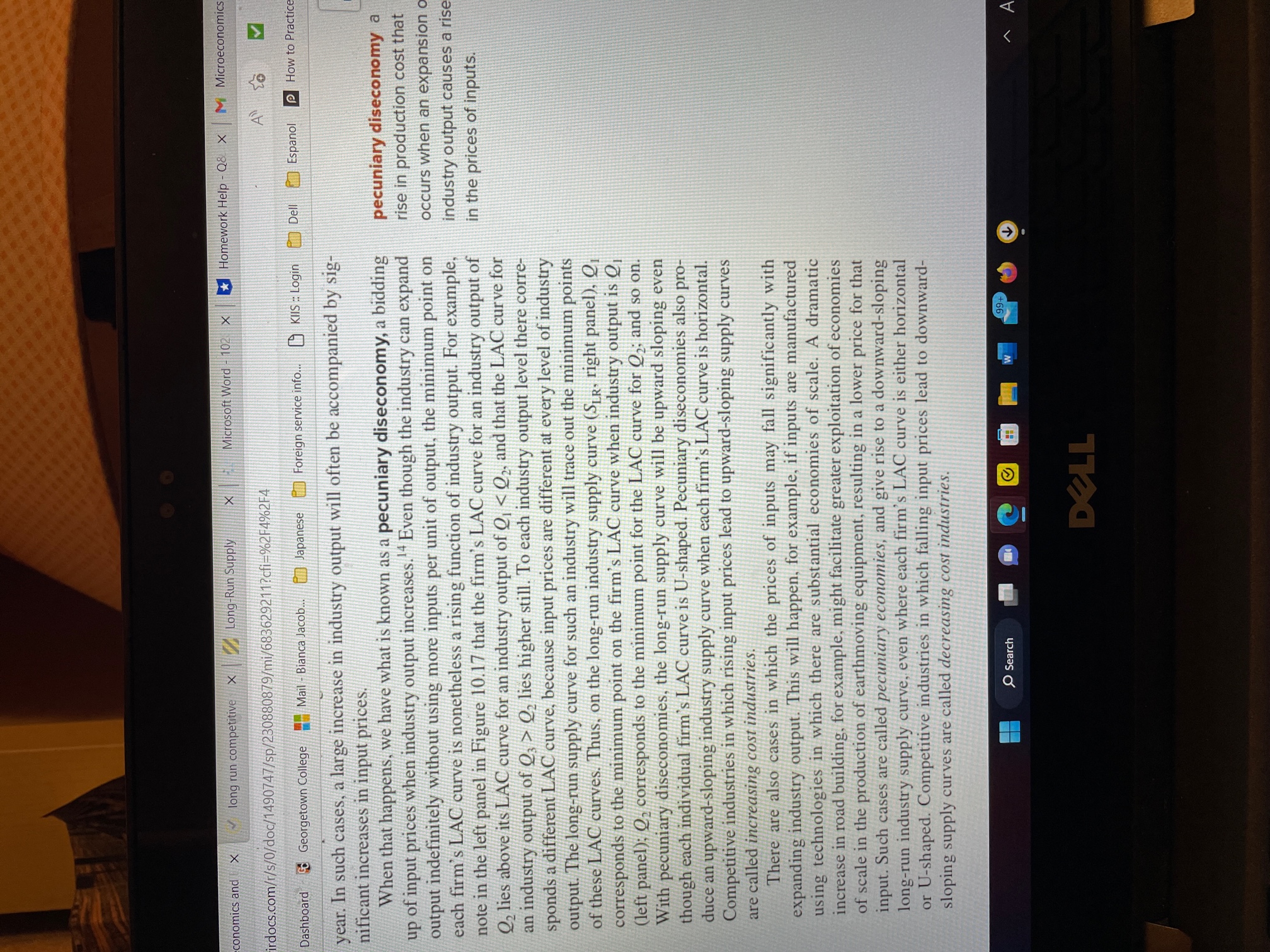

ECO 313 Problem Set #4 T. Cooper Due about October 31 Fall 2022 1. The steel industry converts iron ore and coal into steel. Suppose the price of iron ore falls. a. On a graph, show how the drop in the price of iron ore will affect a typical steel firm's cost curves (ATC, AVC, and MC). b. How will this change affect the supply curve of a typical steel firm? C. Assuming there are three firms, show on a graph how this input price reduction will affect the industry supply curve. (Include all three firm curves and the industry curve.) 2. Let us consider the recycling industry to be competitive, starting from a long-run equilibrium. The producers in this industry employ lots of unskilled labor in collection facilities; a substantial portion of their employees recei receive only the minimum wage. Many demonstrators and politicians today want to raise the minimum wage from $7.25 to $15 per hour. elements of a. Using appropriate graphs, explain how raising the minimum wage will affect the basic h/model. (The focus here is on which curves change.) wage affects (abox, not b. Explain how the price, industry quantity, firm quantity, number of firms, land firm profit in cantal this industry will respond to this change in the short run. (Here the focus is on decisions the firms make, and their consequences.) 3. Congress is seeking energy legislation that will reduce emissions of greenhouse gases. Suppose they propose to charge each gas station an annual "warming fee" of $1000 for the damage their product is doing. Assume the gasoline retail industry is competitive. fixedcost a. Explain how this proposed legislation would affect the price, industry quantity, firm quantity, and firm profit in this industry in the short run. b. How would it affect the same variables in the long run? A UCP Mcdoesn't c. Does the proposal accomplish the desired end of reducing greenhouse emissions? change but ATCdoes X 4. (Skip this one.) The world cotton industry is competitive. For simplicity, let us suppose increase there are only two cotton producing nations, the U.S. and Mali, with many independent farms in butt each nation. only adirect a. Illustrate the initial equilibrium on a graph. How are U.S. and Mali producers represented in swift your graph? say've net b. The U.S. government is concerned that American cotton farmers do not earn enough money change because the world cotton price is too low. In an attempt to remedy this problem, they pass legislation to subsidize U.S. cotton production, paying farmers a $.50 subsidy on every pound of cotton produced. Explain what impact the subsidy has and show the new equilibrium on your graph. c. Analyze the effects of the subsidy. (Answer the following questions first for the short run and then for the long run.) What effect did it have on price, quantity, and consumer surplus in the world market? How did it affect U.S. producers (and their production level)? How did it affect the profit and output of producers in Mali? 5. If we consider the fast food industry to be competitive, we might observe a puzzle. Fast food in Georgetown is much less expensive than similar food in New York. For example, a Big Mac here might sell for $4 while one in New York might sell for $8. The puzzling part is that theX long run competitive x Long-Run Supply x Microsoft Word - 102 x Homework Help - Q& x M /r/s/0/doc/1490747/sp/230880877/mi/683629327?cfi=%2F4%2F4 A Georgetown College Mail - Bianca Jacob... Japanese Foreign service info... KIIS : Login Dell Espanol THE LONG-RUN COMPETITIVE INDUSTRY SUPPLY CURVE We saw that the short-run supply curve for a perfectly competitive industry is the hori- zontal summation of the short-run marginal cost curves of its individual firms. But the corresponding long-run supply curve for a competitive industry is not the horizontal sum- mation of the long-run marginal cost curves of individual firms. Our task in the next sec- tions is to derive the long-run supply curve for competitive industries operating under a variety of different cost conditions. Long-Run Supply Curve with U-Shaped LAC Curves What does the long-run supply curve look like in an industry in which all firms have identical U-shaped long-run average cost (LAC) curves? Suppose, in particular, that these LAC curves are like the one labeled LAC, in the right panel in Figure 10.16. Suppose the demand curve facing the industry is initially the one labeled D, in the left panel. Given this demand curve, the industry will be in long-run equilibrium when each firm installs the capital stock that gives rise to the short-run marginal cost curve labeled SMC, in the right panel. The number of firms in the industry will adjust so that the short-run supply FIGURE 10.16 Market Individual Firm The Long-Run Competitive $/Q Industry Supply Curve When firms are free to enter or SMC leave the market, price cannot depart from the minimum value P2 of the LAC curve in the long min LAC run. If input prices are unaffected by changes in industry output, the long-run supply curve is SLR, a horizontal line at the minimum value of LAC. Q'1 Q 25R Q 2LR Q Q1 Q2 Search W 99+51,005 annualfee, is a fixed cost 3 . G depend on output Industry Supply Palt major cost difference is rent, but that is a fixed cost. We usually ignore fixed costs in analyzing supply decisions, but these real firms seem to include them. How can our competitive model explain higher prices in the New York market as a result of fixed cost differences?ng run competitive x Long-Run Supply X 1 : Microsoft Word - 102 x * Homework Help - Q& x Microecono 0747/sp/230880878/mi/683629618?cfi=%2F4%2F4 M wn College Mail - Bianca Jacob... Japanese Foreign service info... KIIS : Login Dell Espanol |How to Pra curve, denoted SSR in the left panel, intersects D, at a price equal to the minimum value of LAC,. (If there were more firms than that or fewer, each would be making either an economic loss or a profit.) Now suppose demand shifts rightward from D, to D2, intersecting the short-run in- dustry supply curve at the price P2. The short-run effect will be for each firm to increase its output from Of to Q%, which will lead to an economic profit measured by the shaded rectangle in the right panel in Figure 10.16. With the passage of time, these profits will lure additional firms into the industry until the rightward supply shift (to S* in the left panel) again results in a price of min LAC. The long-run response to an increase in demand, then, is to increase industry output by increasing the number of firms in the industry. As long as the expansion of industry output does not cause the prices of capi- tal, labor, and other inputs to rise, there will be no long-run increase in the price of the product. 13 If demand had shifted to the left from D, , a parallel story would have unfolded: Price would have fallen in the short run, firms would have adjusted their offerings, and the re- sulting economic losses would have induced some firms to leave the industry. The exodus would shift industry supply to the left until price had again risen to min LAC. Here again the long-run response to a shift in demand is accommodated by a change in the number of firms. With U-shaped LAC curves, there is no tendency for a fall in demand to produce a long-run decline in price. In summary, the long-run supply curve for a competitive industry with U-shaped LAC curves and constant input prices is a horizontal line at the minimum value of the LAC curve. In the long run, all the adjustment to variations in demand occurs not through changing prices but through variations in the number of firms serving the mar- ket. Following possibly substantial deviations in the short run, price shows a persistent tendency to gravitate to the minimum value of long-run average cost. Industry Supply When Each LAC Curve Is Horizontal 9 Search C W 99+ig run competitive x Long-Run Supply X Microsoft Word - 102 x Homework Help - Q& X M Microeconom 0747/sp/230880878/mi/683629618?cfi=%2F4%2F4 College Mail - Bianca Jacob... Japanese Foreign service info... ) KIIS : Login Dell Espanol |How to Practi Industry Supply When Each LAC Curve Is Horizontal As in the case of U-shaped LAC curves, the long-run industry supply curve when each firm's LAC curve is horizontal will again be a horizontal line (again assuming that input prices do not change with changes in industry output). But there is one salient difference between the two cases: When firms have identical U-shaped LAC curves, we can predict that each firm will produce the quantity that corresponds to the minimum point on its LAC curve. We thus get an industry composed of firms that all produce the same level of output. With horizontal LAC curves, by contrast, there is simply no unique minimum-cost point. LAC is the same at any level of output, which leads to an indeterminacy not present in the earlier case. We just cannot predict what the size distribution of firms will look like in the case of horizontal LAC curves. There may be a handful of large firms, many small ones, or a mixture of different sizes. All we can say with confidence is that price in the long run will gravitate toward the value of LAC. How Changing Input Prices Affect Long-Run Supply In our analysis of cost curves in Chapter 9, which forms the basis of our analysis of sup- ply under perfect competition, an important assumption was that input prices do not vary with the amount of output produced. For a single firm whose input purchases constitute only a small fraction of the total input market, this assumption is plausible. In many cases, moreover, even the entire industry's demands for inputs constitute only a small share of the overall input market. For example, even if the insurance industry issues 20 percent more policies this year than last, it employs such a small percentage of the total available supplies of secretaries, computers, executives, and other inputs that the prices of these inputs should not be significantly affected. So here too we may reasonably assume that input prices do not depend on output. "More follows on what happens when changes in industry output cause changes in input prices. 9 Search (99+ DELLX long run competitive x Long-Run Supply X Microsoft Word - 102 x Homework Help - Q& x M Microeconomics prob /s/0/doc/1490747/sp/230880879/mi/683629211?cfi=%2F4%2F4 A to Georgetown College Mail - Bianca Jacob... ) Japanese e Foreign service info... Klis =: Login Dell Espanol P How to Practice Sel.. FIGURE 10.17 K Long-Run Supply Curve for an Individual Firm Market Increasing Cost Industry When input prices rise with $/unit of output $/unit of output industry output, each firm's LAC curve will also rise with industry output (left panel). Thus the LACO - O3 SIR firm's LAC curve when industry output is @2 lies above its LAC LACO - 02 curve when industry output is Q1 (left panel). Firms will still LACO - Q gravitate to the minimum points on their LAC curves (@;, left panel), but because this minimum point depends on Q2 Q 2 industry output, the long-run industry supply curve (SLR, right panel) will now be upward sloping. But there are at least some industries in which the volume of inputs purchased con- ites an appreciable share of the entire input market. The market for commercial airlin- for example, consumes a significant share of the total amount of titanium sold each ar. In such cases, a large increase in industry output will often be accompanied by sig- ficant increases in input prices. When that happens, we have what is known as a pecuniary diseconomy, a bidding pecuniary diseconomy a of input prices when industry output increases. # Even though the industry can expand rise in production cost that utput indefinitely without using more inputs per unit of output, the minimum point on occurs when an expansion of Search A DELLconomics and (X long run competitive X Long-Run Supply |X Microsoft Word - 102| |Homework Help -Q& X M Microeconomic rdocs.com/r/s/0/doc/1490747/sp/230880879/mi/683629211?cfi#%2F4%2FA Dashboard Georgetown College Mail - Bianca Jacob... Japanese Foreign service info... KIIS = Login Dell Espanol How to Practic year. In such cases, a large increase in industry output will often be accompanied by sig- nificant increases in input prices. When that happens, we have what is known as a pecuniary diseconomy, a bidding pecuniary diseconomy a up of input prices when industry output increases. Even though the industry can expand ise in production cost that output indefinitely without using more inputs per unit of output, the minimum point on occurs when an expansion each firm's LAC curve is nonetheless a rising function of industry output. For example, industry output causes a rise note in the left panel in Figure 10.17 that the firm's LAC curve for an industry output of in the prices of inputs. 2 lies above its LAC curve for an industry output of , @2 lies higher still. To each industry output level there corre- sponds a different LAC curve, because input prices are different at every level of industry output. The long-run supply curve for such an industry will trace out the minimum points of these LAC curves. Thus, on the long-run industry supply curve (SR. right panel), O, corresponds to the minimum point on the firm's LAC curve when industry output is @ (left panel); 02 corresponds to the minimum point for the LAC curve for 2; and so on. With pecuniary diseconomies, the long-run supply curve will be upward sloping even though each individual firm's LAC curve is U-shaped. Pecuniary diseconomies also pro- duce an upward-sloping industry supply curve when each firm's LAC curve is horizontal. Competitive industries in which rising input prices lead to upward-sloping supply curves are called increasing cost industries. There are also cases in which the prices of inputs may fall significantly with expanding industry output. This will happen, for example, if inputs are manufactured using technologies in which there are substantial economies of scale. A dramatic increase in road building, for example, might facilitate greater exploitation of economies of scale in the production of earthmoving equipment, resulting in a lower price for that input. Such cases are called pecuniary economies, and give rise to a downward-sloping long-run industry supply curve, even where each firm's LAC curve is either horizontal or U-shaped. Competitive industries in which falling input prices lead to downward- sloping supply curves are called decreasing cost industries. Search C C HW 99+ DELL

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance