Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I have provided all the information needed. No one to answer? please advise. Thank you QUESTION ONE Kalaluka, a Zambian resident individual, runs a small

I have provided all the information needed. No one to answer? please advise. Thank you

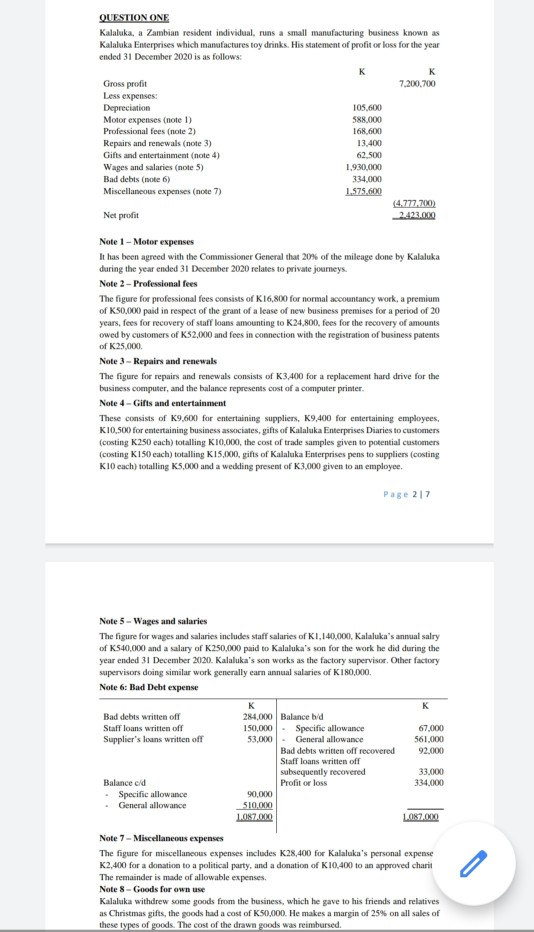

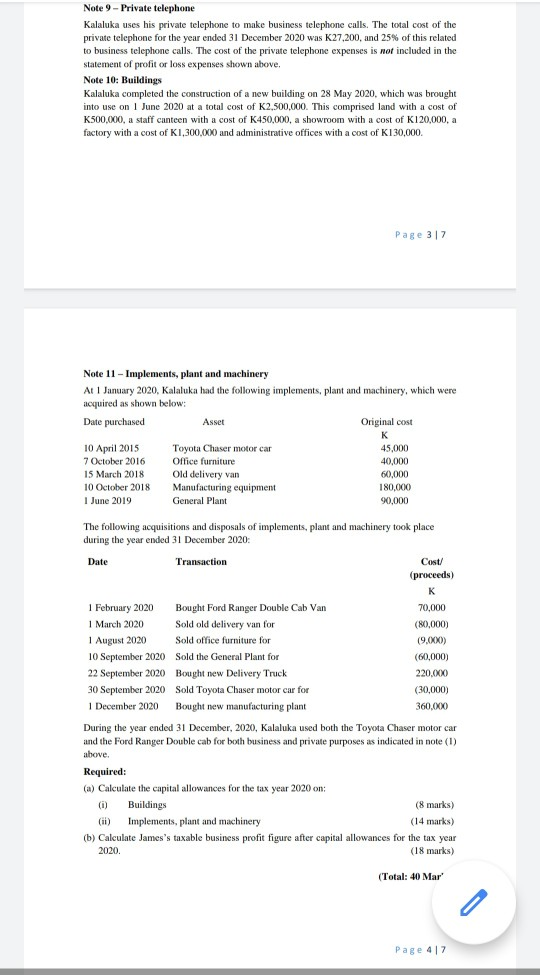

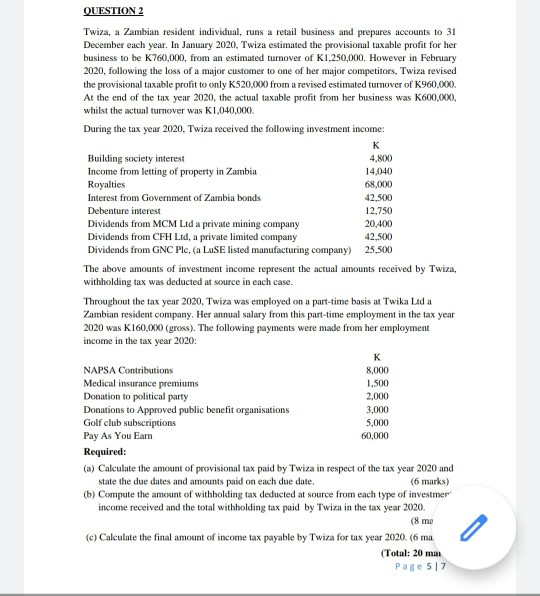

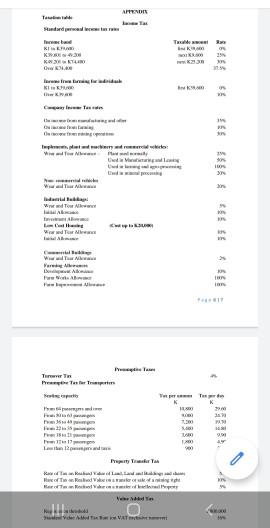

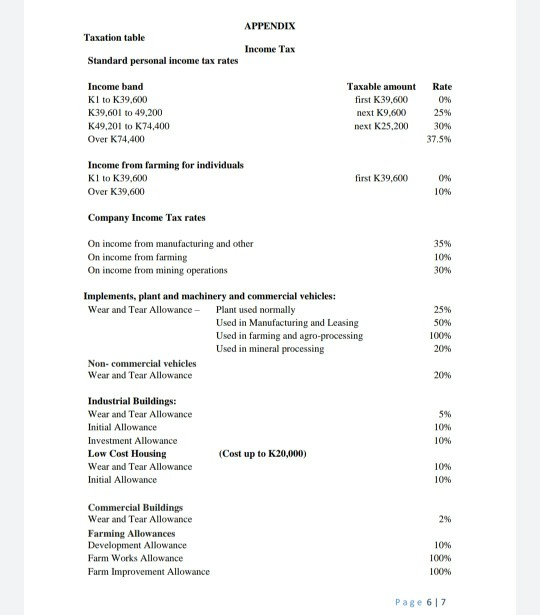

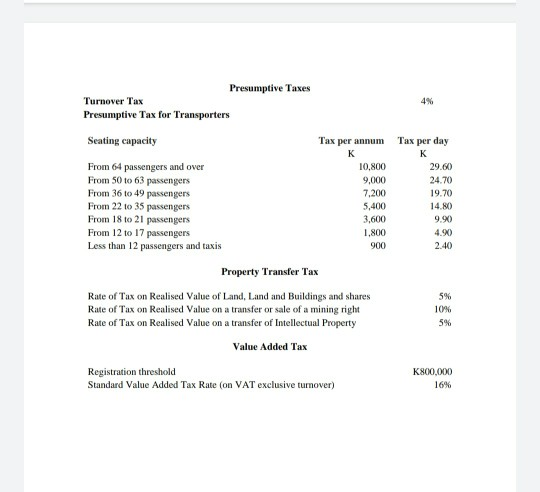

QUESTION ONE Kalaluka, a Zambian resident individual, runs a small manufacturing business known as Kalaluka Enterprises which manufactures toy drinks. His statement of profit or loss for the year ended 31 December 2020 is as follows: K Gross profit 7.200,700 Less expenses Depreciation 105.600 Motor expenses (note 1) 588.000 Professional fees (note 2) 168,600 Repairs and renewals (note 3) 13.400 Gifts and entertainment (note 4) 62.500 Wages and salaries (note 5) 1.930,000 Bad debts (note 6) 334,000 Miscellaneous expenses (note 7) 1.575.600 (4.777 700) Net profit 2.423.000 Note 1 - Motor expenses It has been agreed with the Commissioner General that 20% of the mileage done by Kalaluka during the year ended 31 December 2020 relates to private journeys. Note 2 - Professional fees The figure for professional fees consists of K16,800 for normal accountancy work, a premium of K50,000 paid in respect of the grant of a lease of new business premises for a period of 20 years, fees for recovery of staff loans amounting to K24,800, fees for the recovery of amounts owed by customers of KS2,000 and fees in connection with the registration of business patents of K25,000 Note 3 - Repairs and renewals The figure for repairs and renewals consists of K3.400 for a replacement hard drive for the business computer, and the balance represents cost of a computer printer. Note 4 - Gifts and entertainment These consists of K9,600 for entertaining suppliers, K9,400 for entertaining employees, K10,500 for entertaining business associates, gifts of Kalaluka Enterprises Diaries to customers (costing K250 each) totalling K10,000, the cost of trade samples given to potential customers (costing K150 each) totalling K15,000, gifts of Kalaluka Enterprises pens to suppliers (costing K10 cach) totalling K5,000 and a wedding present of K3,000 given to an employee. Page 217 Note 5 - Wages and salaries The figure for wages and salaries includes staff salaries of K1,140,000, Kalaluka's annual salry of K540,000 and a salary of K250,000 paid to Kalaluka's son for the work he did during the year ended 31 December 2020. Kalaluka's son works as the factory supervisor Other factory supervisors doing similar work generally earn annual salaries of K180,000 Note 6: Bad Debt expense K K Bad debts written off 284,000 Balance hd Staff loans written off 150,000. Specific allowance 67,000 Supplier's loans written off 53,000 - General allowance 561.000 Bad debts written off recovered 92.000 Staff loans written off subsequently recovered 33.000 Balance eld Profit or loss 334.000 Specific allowance 90,000 General allowance 510.000 1.087.000 LO87.000 Note 7 - Miscellaneous expenses The figure for miscellaneous expenses includes K28,400 for Kalaluka's personal expense K2,400 for a donation to a political party, and a donation of K10,400 to an approved charit The remainder is made of allowable expenses. Note 8 Goods for own use Kalaluka withdrew some goods from the business, which he gave to his friends and relatives as Christmas gifts, the goods had a cost of K50,000. He makes a margin of 25% on all sales of these types of goods. The cost of the drawn goods was reimbursed Note 9 - Private telephone Kalaluka uses his private telephone to make business telephone calls. The total cost of the private telephone for the year ended 31 December 2020 was K27.200, and 25% of this related to business telephone calls. The cost of the private telephone expenses is not included in the Statement of profit or loss expenses shown above, Note 10: Buildings Kalaluka completed the construction of a new building on 28 May 2020, which was brought into use on 1 June 2020 at a total cost of K2,500,000. This comprised land with a cost of K500,000, a staff canteen with a cost of K450,000, a showroom with a cost of K120,000, a factory with a cost of K1,300,000 and administrative offices with a cost of K130,000 Page 37 Note 11 - Implements, plant and machinery At 1 January 2020, Kalaluka had the following implements, plant and machinery, which were acquired as shown below: Date purchased Asset Original cost K 10 April 2015 Toyota Chaser motor car 45,000 7 October 2016 Office furniture 40,000 15 March 2018 Old delivery van 60,000 10 October 2018 Manufacturing equipment 180,000 1 June 2019 General Plant 90.000 The following acquisitions and disposals of implements, plant and machinery took place during the year ended 31 December 2020: Date Transaction Cost/ (proceeds) K 1 February 2020 Bought Ford Ranger Double Cab Van 70,000 1 March 2020 Sold old delivery van for (80,000) 1 August 2020 Sold office furniture for (9.(XX) 10 September 2020 Sold the General Plant for (60,000) 22 September 2020 Bought new Delivery Truck 220.000 30 September 2020 Sold Toyota Chaser motor car for (30,000) 1 December 2020 Bought new manufacturing plant 360.XX During the year ended 31 December, 2020, Kalaluka used both the Toyota Chaser motor car and the Ford Ranger Double cab for both business and private purposes as indicated in note (1) abowe Required: (a) Calculate the capital allowances for the tax year 2020 on: (1) Buildings (8 marks) (ii) Implements, plant and machinery (14 marks) (b) Calculate James's taxable business profit figure after capital allowances for the tax year 2020 (18 marks) (Total: 40 Mar' : Page 417 QUESTION 2 Twiza, a Zambian resident individual, runs a retail business and prepares accounts to 31 December each year. In January 2020, Twiza estimated the provisional taxable profit for her business to be K760,000, from an estimated turnover of K1,250,000. However in February 2020, following the loss of a major customer to one of her major competitors, Twiza revised the provisional taxable profit to only K520,000 from a revised estimated turnover of K960,000. At the end of the tax year 2020, the actual taxable profit from her business was K600,000, whilst the actual turnover was K1,040,000 During the tax year 2020, Twiza received the following investment income: K Building society interest 4.800 Income from letting of property in Zambia 14,040 Royalties 68,000 Interest from Government of Zambia bonds 42.500 Debenture interest 12,750 Dividends from MCM Ltd a private mining company 20,400 Dividends from CFH Ltd, a private limited company 42,500 Dividends from GNC Plc, (a LuSE listed manufacturing company) 25,500 The above amounts of investment income represent the actual amounts received by Twiza, withholding tax was deducted at source in each case. Throughout the tax year 2020, Twiza was employed on a part-time basis at Twika Lid a Zambian resident company. Her annual salary from this part-time employment in the tax year 2020 was K160,000 (gross). The following payments were made from her employment income in the tax year 2020: K NAPSA Contributions 8,000 Medical insurance premiums 1.500 Donation to political party 2,000 Donations to Approved public benefit organisations 3,000 Golf club subscriptions 5,000 Pay As You Earn 60,000 Required: (a) Calculate the amount of provisional tax paid by Twiza in respect of the tax year 2020 and state the due dates and amounts paid on each due date. (6 marks) (b) Compute the amount of withholding tax deducted at source from each type of investmer income received and the total withholding tax paid by Twiza in the tax year 2020. (8 me (c) Calculate the final amount of income tax payable by Twiza for tax year 2020. (6 ma. (Total: 20 man Page 57 Standard prestane KI KKT w tidigal Landey Www To D A IN Tur 3 Ipy retra | Men dhe do Taxation table APPENDIX Income Tax Standard personal income tax rates Income band Kl to K39,600 K39,601 to 49,200 K49,201 to K74,400 Over K74,400 Taxable amount first K39.600 next K9.600 next K25,200 Rate 0% 25% 30% 37.5% Income from farming for individuals Kl to K39,600 Over K39,600 first K39,600 0% 10% Company Income Tax rates 35% 10% 30% On income from manufacturing and other On income from farming On income from mining operations Implements, plant and machinery and commercial vehicles: Wear and Tear Allowance - Plant used normally Used in Manufacturing and Leasing Used in farming and agro-processing Used in mineral processing Non-commercial vehicles Wear and Tear Allowance 25% 50% 100% 20% 20% Industrial Buildings: Wear and Tear Allowance Initial Allowance Investment Allowance Low Cost Housing Wear and Tear Allowance Initial Allowance 5% 10% 10% (Cost up to K20,000) 10% 10% 2% Commercial Buildings Wear and Tear Allowance Farming Allowances Development Allowance Farm Works Allowance Farm Improvement Allowance 10% 100% 100% Page 67 K Presumptive Taxes Turnover Tax Presumptive Tax for Transporters Seating capacity Tax per annum From 64 passengers and over 10.800 From 50 to 63 passengers 9,000 From 36 to 49 passengers 7.200 From 22 to 35 passengers 5,400 From 18 to 21 passengers 3,600 From 12 to 17 passengers 1.800 Less than 12 passengers and taxis 900 Property Transfer Tax Rate of Tax on Realised Value of Land, Land and Buildings and shares Rate of Tax on Realised Value on a transfer or sale of a mining right Rate of Tax on Realised Value on a transfer of Intellectual Property Value Added Tax Registration threshold Standard Value Added Tax Rate (on VAT exclusive turnover) Tax per day K 29.60 24.70 19.70 14.80 9.90 4.90) 2.40 5% 10% 5% K800,000 16% QUESTION ONE Kalaluka, a Zambian resident individual, runs a small manufacturing business known as Kalaluka Enterprises which manufactures toy drinks. His statement of profit or loss for the year ended 31 December 2020 is as follows: K Gross profit 7.200,700 Less expenses Depreciation 105.600 Motor expenses (note 1) 588.000 Professional fees (note 2) 168,600 Repairs and renewals (note 3) 13.400 Gifts and entertainment (note 4) 62.500 Wages and salaries (note 5) 1.930,000 Bad debts (note 6) 334,000 Miscellaneous expenses (note 7) 1.575.600 (4.777 700) Net profit 2.423.000 Note 1 - Motor expenses It has been agreed with the Commissioner General that 20% of the mileage done by Kalaluka during the year ended 31 December 2020 relates to private journeys. Note 2 - Professional fees The figure for professional fees consists of K16,800 for normal accountancy work, a premium of K50,000 paid in respect of the grant of a lease of new business premises for a period of 20 years, fees for recovery of staff loans amounting to K24,800, fees for the recovery of amounts owed by customers of KS2,000 and fees in connection with the registration of business patents of K25,000 Note 3 - Repairs and renewals The figure for repairs and renewals consists of K3.400 for a replacement hard drive for the business computer, and the balance represents cost of a computer printer. Note 4 - Gifts and entertainment These consists of K9,600 for entertaining suppliers, K9,400 for entertaining employees, K10,500 for entertaining business associates, gifts of Kalaluka Enterprises Diaries to customers (costing K250 each) totalling K10,000, the cost of trade samples given to potential customers (costing K150 each) totalling K15,000, gifts of Kalaluka Enterprises pens to suppliers (costing K10 cach) totalling K5,000 and a wedding present of K3,000 given to an employee. Page 217 Note 5 - Wages and salaries The figure for wages and salaries includes staff salaries of K1,140,000, Kalaluka's annual salry of K540,000 and a salary of K250,000 paid to Kalaluka's son for the work he did during the year ended 31 December 2020. Kalaluka's son works as the factory supervisor Other factory supervisors doing similar work generally earn annual salaries of K180,000 Note 6: Bad Debt expense K K Bad debts written off 284,000 Balance hd Staff loans written off 150,000. Specific allowance 67,000 Supplier's loans written off 53,000 - General allowance 561.000 Bad debts written off recovered 92.000 Staff loans written off subsequently recovered 33.000 Balance eld Profit or loss 334.000 Specific allowance 90,000 General allowance 510.000 1.087.000 LO87.000 Note 7 - Miscellaneous expenses The figure for miscellaneous expenses includes K28,400 for Kalaluka's personal expense K2,400 for a donation to a political party, and a donation of K10,400 to an approved charit The remainder is made of allowable expenses. Note 8 Goods for own use Kalaluka withdrew some goods from the business, which he gave to his friends and relatives as Christmas gifts, the goods had a cost of K50,000. He makes a margin of 25% on all sales of these types of goods. The cost of the drawn goods was reimbursed Note 9 - Private telephone Kalaluka uses his private telephone to make business telephone calls. The total cost of the private telephone for the year ended 31 December 2020 was K27.200, and 25% of this related to business telephone calls. The cost of the private telephone expenses is not included in the Statement of profit or loss expenses shown above, Note 10: Buildings Kalaluka completed the construction of a new building on 28 May 2020, which was brought into use on 1 June 2020 at a total cost of K2,500,000. This comprised land with a cost of K500,000, a staff canteen with a cost of K450,000, a showroom with a cost of K120,000, a factory with a cost of K1,300,000 and administrative offices with a cost of K130,000 Page 37 Note 11 - Implements, plant and machinery At 1 January 2020, Kalaluka had the following implements, plant and machinery, which were acquired as shown below: Date purchased Asset Original cost K 10 April 2015 Toyota Chaser motor car 45,000 7 October 2016 Office furniture 40,000 15 March 2018 Old delivery van 60,000 10 October 2018 Manufacturing equipment 180,000 1 June 2019 General Plant 90.000 The following acquisitions and disposals of implements, plant and machinery took place during the year ended 31 December 2020: Date Transaction Cost/ (proceeds) K 1 February 2020 Bought Ford Ranger Double Cab Van 70,000 1 March 2020 Sold old delivery van for (80,000) 1 August 2020 Sold office furniture for (9.(XX) 10 September 2020 Sold the General Plant for (60,000) 22 September 2020 Bought new Delivery Truck 220.000 30 September 2020 Sold Toyota Chaser motor car for (30,000) 1 December 2020 Bought new manufacturing plant 360.XX During the year ended 31 December, 2020, Kalaluka used both the Toyota Chaser motor car and the Ford Ranger Double cab for both business and private purposes as indicated in note (1) abowe Required: (a) Calculate the capital allowances for the tax year 2020 on: (1) Buildings (8 marks) (ii) Implements, plant and machinery (14 marks) (b) Calculate James's taxable business profit figure after capital allowances for the tax year 2020 (18 marks) (Total: 40 Mar' : Page 417 QUESTION 2 Twiza, a Zambian resident individual, runs a retail business and prepares accounts to 31 December each year. In January 2020, Twiza estimated the provisional taxable profit for her business to be K760,000, from an estimated turnover of K1,250,000. However in February 2020, following the loss of a major customer to one of her major competitors, Twiza revised the provisional taxable profit to only K520,000 from a revised estimated turnover of K960,000. At the end of the tax year 2020, the actual taxable profit from her business was K600,000, whilst the actual turnover was K1,040,000 During the tax year 2020, Twiza received the following investment income: K Building society interest 4.800 Income from letting of property in Zambia 14,040 Royalties 68,000 Interest from Government of Zambia bonds 42.500 Debenture interest 12,750 Dividends from MCM Ltd a private mining company 20,400 Dividends from CFH Ltd, a private limited company 42,500 Dividends from GNC Plc, (a LuSE listed manufacturing company) 25,500 The above amounts of investment income represent the actual amounts received by Twiza, withholding tax was deducted at source in each case. Throughout the tax year 2020, Twiza was employed on a part-time basis at Twika Lid a Zambian resident company. Her annual salary from this part-time employment in the tax year 2020 was K160,000 (gross). The following payments were made from her employment income in the tax year 2020: K NAPSA Contributions 8,000 Medical insurance premiums 1.500 Donation to political party 2,000 Donations to Approved public benefit organisations 3,000 Golf club subscriptions 5,000 Pay As You Earn 60,000 Required: (a) Calculate the amount of provisional tax paid by Twiza in respect of the tax year 2020 and state the due dates and amounts paid on each due date. (6 marks) (b) Compute the amount of withholding tax deducted at source from each type of investmer income received and the total withholding tax paid by Twiza in the tax year 2020. (8 me (c) Calculate the final amount of income tax payable by Twiza for tax year 2020. (6 ma. (Total: 20 man Page 57 Standard prestane KI KKT w tidigal Landey Www To D A IN Tur 3 Ipy retra | Men dhe do Taxation table APPENDIX Income Tax Standard personal income tax rates Income band Kl to K39,600 K39,601 to 49,200 K49,201 to K74,400 Over K74,400 Taxable amount first K39.600 next K9.600 next K25,200 Rate 0% 25% 30% 37.5% Income from farming for individuals Kl to K39,600 Over K39,600 first K39,600 0% 10% Company Income Tax rates 35% 10% 30% On income from manufacturing and other On income from farming On income from mining operations Implements, plant and machinery and commercial vehicles: Wear and Tear Allowance - Plant used normally Used in Manufacturing and Leasing Used in farming and agro-processing Used in mineral processing Non-commercial vehicles Wear and Tear Allowance 25% 50% 100% 20% 20% Industrial Buildings: Wear and Tear Allowance Initial Allowance Investment Allowance Low Cost Housing Wear and Tear Allowance Initial Allowance 5% 10% 10% (Cost up to K20,000) 10% 10% 2% Commercial Buildings Wear and Tear Allowance Farming Allowances Development Allowance Farm Works Allowance Farm Improvement Allowance 10% 100% 100% Page 67 K Presumptive Taxes Turnover Tax Presumptive Tax for Transporters Seating capacity Tax per annum From 64 passengers and over 10.800 From 50 to 63 passengers 9,000 From 36 to 49 passengers 7.200 From 22 to 35 passengers 5,400 From 18 to 21 passengers 3,600 From 12 to 17 passengers 1.800 Less than 12 passengers and taxis 900 Property Transfer Tax Rate of Tax on Realised Value of Land, Land and Buildings and shares Rate of Tax on Realised Value on a transfer or sale of a mining right Rate of Tax on Realised Value on a transfer of Intellectual Property Value Added Tax Registration threshold Standard Value Added Tax Rate (on VAT exclusive turnover) Tax per day K 29.60 24.70 19.70 14.80 9.90 4.90) 2.40 5% 10% 5% K800,000 16%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Inside Accounting The Sociology Of Financial Reporting And Auditing

Authors: David Leung

1st Edition

1138251178, 9781138251175