Question

I have the answer to the question, but I need hep understanding how a portion of the problem works. The answer is 454.45%, but I

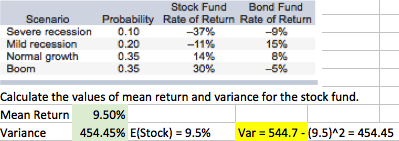

I have the answer to the question, but I need hep understanding how a portion of the problem works. The answer is 454.45%, but I need help understanding how the variance's VAR 544.7 in yellow how it was calculated step by step please

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Optimization Methods In Finance

Authors: Gerard Cornuejols, Reha Tütüncü

1st Edition

0521861705, 978-0521861700