Answered step by step

Verified Expert Solution

Question

1 Approved Answer

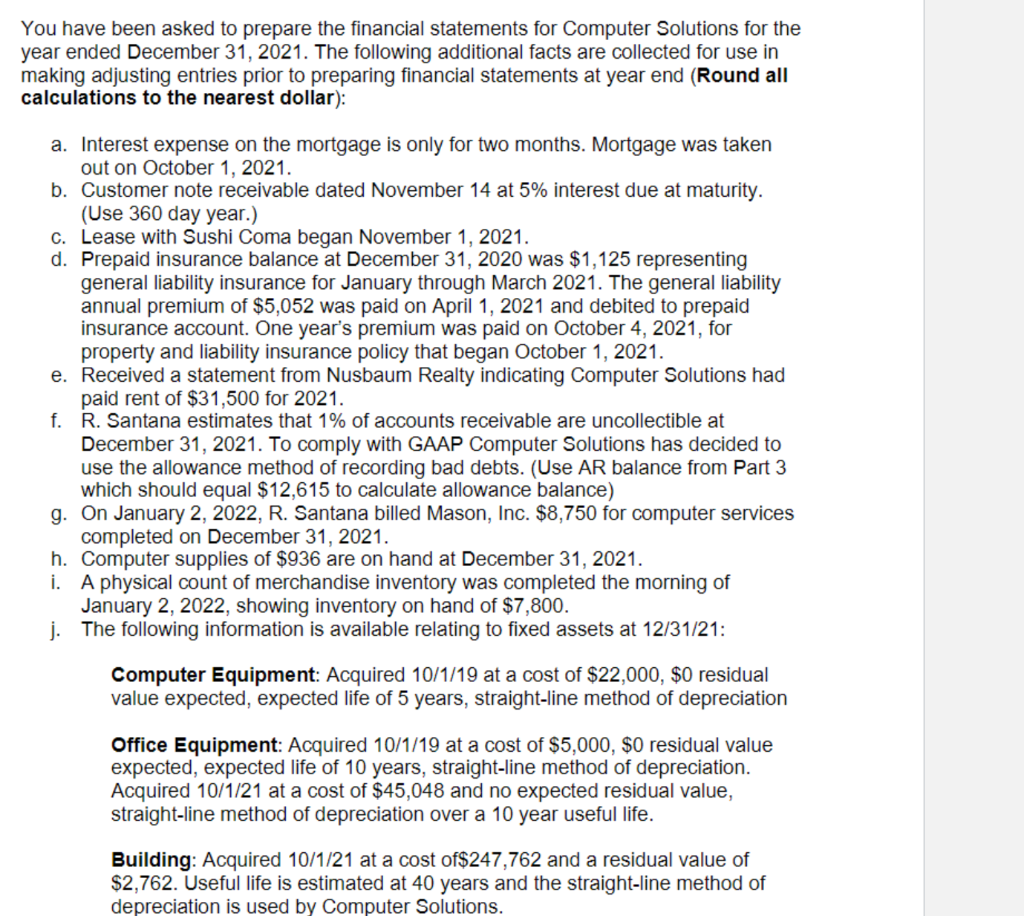

I just need journal entries You have been asked to prepare the financial statements for Computer Solutions for the year ended December 31, 2021. The

I just need journal entries

You have been asked to prepare the financial statements for Computer Solutions for the year ended December 31, 2021. The following additional facts are collected for use in making adjusting entries prior to preparing financial statements at year end (Round all calculations to the nearest dollar): a. Interest expense on the mortgage is only for two months. Mortgage was taken out on October 1, 2021. b. Customer note receivable dated November 14 at 5% interest due at maturity. (Use 360 day year.) c. Lease with Sushi Coma began November 1, 2021. d. Prepaid insurance balance at December 31,2020 was $1,125 representing general liability insurance for January through March 2021. The general liability annual premium of $5,052 was paid on April 1, 2021 and debited to prepaid insurance account. One year's premium was paid on October 4, 2021, for property and liability insurance policy that began October 1, 2021. e. Received a statement from Nusbaum Realty indicating Computer Solutions had paid rent of $31,500 for 2021. f. R. Santana estimates that 1% of accounts receivable are uncollectible at December 31, 2021. To comply with GAAP Computer Solutions has decided to use the allowance method of recording bad debts. (Use AR balance from Part 3 which should equal $12,615 to calculate allowance balance) g. On January 2, 2022, R. Santana billed Mason, Inc. $8,750 for computer services completed on December 31, 2021. h. Computer supplies of $936 are on hand at December 31, 2021. i. A physical count of merchandise inventory was completed the morning of January 2, 2022, showing inventory on hand of $7,800. j. The following information is available relating to fixed assets at 12/31/21: Computer Equipment: Acquired 10/1/19 at a cost of $22,000, $0 residual value expected, expected life of 5 years, straight-line method of depreciation Office Equipment: Acquired 10/1/19 at a cost of $5,000,$0 residual value expected, expected life of 10 years, straight-line method of depreciation. Acquired 10/1/21 at a cost of $45,048 and no expected residual value, straight-line method of depreciation over a 10 year useful life. Building: Acquired 10/1/21 at a cost of $247,762 and a residual value of $2,762. Useful life is estimated at 40 years and the straight-line method of depreciation is used by Computer Solutions. You have been asked to prepare the financial statements for Computer Solutions for the year ended December 31, 2021. The following additional facts are collected for use in making adjusting entries prior to preparing financial statements at year end (Round all calculations to the nearest dollar): a. Interest expense on the mortgage is only for two months. Mortgage was taken out on October 1, 2021. b. Customer note receivable dated November 14 at 5% interest due at maturity. (Use 360 day year.) c. Lease with Sushi Coma began November 1, 2021. d. Prepaid insurance balance at December 31,2020 was $1,125 representing general liability insurance for January through March 2021. The general liability annual premium of $5,052 was paid on April 1, 2021 and debited to prepaid insurance account. One year's premium was paid on October 4, 2021, for property and liability insurance policy that began October 1, 2021. e. Received a statement from Nusbaum Realty indicating Computer Solutions had paid rent of $31,500 for 2021. f. R. Santana estimates that 1% of accounts receivable are uncollectible at December 31, 2021. To comply with GAAP Computer Solutions has decided to use the allowance method of recording bad debts. (Use AR balance from Part 3 which should equal $12,615 to calculate allowance balance) g. On January 2, 2022, R. Santana billed Mason, Inc. $8,750 for computer services completed on December 31, 2021. h. Computer supplies of $936 are on hand at December 31, 2021. i. A physical count of merchandise inventory was completed the morning of January 2, 2022, showing inventory on hand of $7,800. j. The following information is available relating to fixed assets at 12/31/21: Computer Equipment: Acquired 10/1/19 at a cost of $22,000, $0 residual value expected, expected life of 5 years, straight-line method of depreciation Office Equipment: Acquired 10/1/19 at a cost of $5,000,$0 residual value expected, expected life of 10 years, straight-line method of depreciation. Acquired 10/1/21 at a cost of $45,048 and no expected residual value, straight-line method of depreciation over a 10 year useful life. Building: Acquired 10/1/21 at a cost of $247,762 and a residual value of $2,762. Useful life is estimated at 40 years and the straight-line method of depreciation is used by Computer SolutionsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting

Authors: Carl S. Warren, Philip E. Fess, James M. Reeve, C.Rollin Niswonger, Jim Reeve

18th Edition

0538839333, 978-0538839334