I need an answer of appendix3

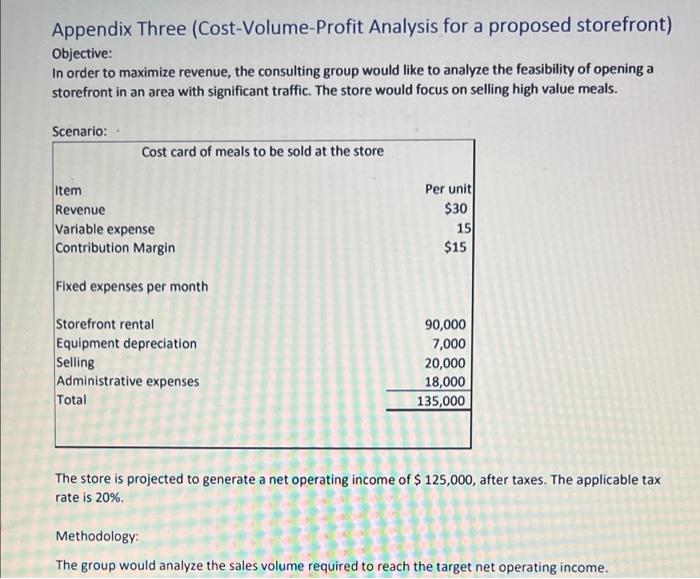

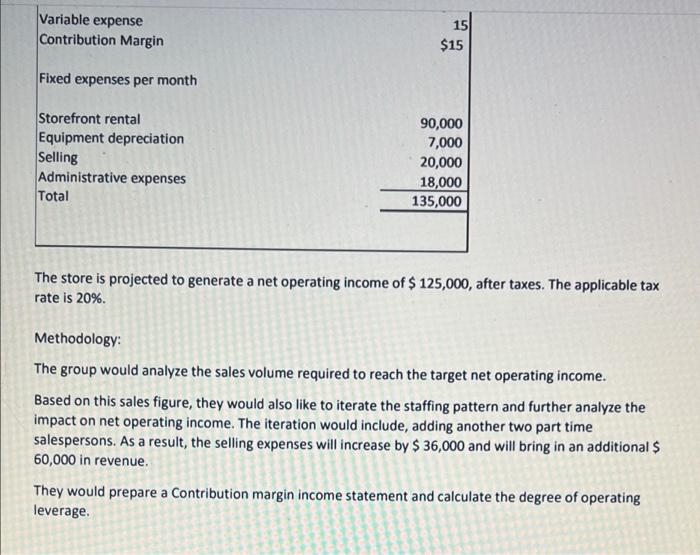

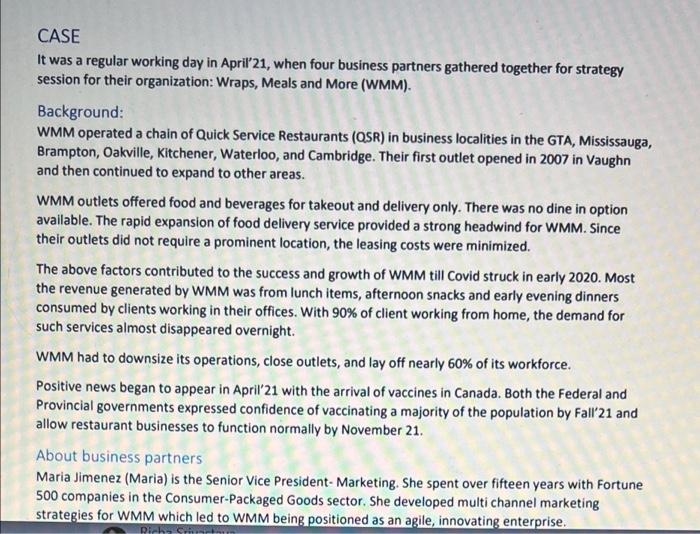

CASE It was a regular working day in April 21, when four business partners gathered together for strategy session for their organization: Wraps, Meals and More (WMM). Background: WMM operated a chain of Quick Service Restaurants (QSR) in business localities in the GTA, Mississauga, Brampton, Oakville, Kitchener, Waterloo, and Cambridge. Their first outlet opened in 2007 in Vaughn and then continued to expand to other areas. WMM outlets offered food and beverages for takeout and delivery only. There was no dine in option available. The rapid expansion of food delivery service provided a strong headwind for WMM. Since their outlets did not require a prominent location, the leasing costs were minimized. The above factors contributed to the success and growth of WMM till Covid struck in early 2020. Most the revenue generated by WMM was from lunch items, afternoon snacks and early evening dinners consumed by clients working in their offices. With 90% of client working from home, the demand for such services almost disappeared overnight. WMM had to downsize its operations, close outlets, and lay off nearly 60% of its workforce. Positive news began to appear in April 21 with the arrival of vaccines in Canada. Both the Federal and Provincial governments expressed confidence of vaccinating a majority of the population by Fall'21 and allow restaurant businesses to function normally by November 21. About business partners Maria Jimenez (Maria) is the Senior Vice President Marketing. She spent over fifteen years with Fortune 500 companies in the Consumer-Packaged Goods sector. She developed multichannel marketing strategies for WMM which led to WMM being positioned as an agile, innovating enterprise. bout business partners Maria Jimenez (Maria) is the Senior Vice President Marketing. She spent over fifteen years with Fortune 500 companies in the Consumer-Packaged Goods sector. She developed multi channel marketing strategies for WMM which led to WMM being positioned as an agile, innovating enterprise. Julia Smith (Julia) was the Corporate Chef of WMM. She spent nearly twenty years with leading hotel chains in Western Canada before taking on the current role in WMM. She displayed exemplary skills at developing new products which contributed to the profitability of WMM. Adam Wiseman (Adam) was the Chief Financial Officer of WMM. He too came from a hospitality background, having worked with leading hotel chains in Toronto. His expertise was in Capital Budgeting and product costing, which worked well in conjunction with the culinary skills of Julia when new products were being developed. Yetunde Jones (Tunde) was the Senior Vice President-Operations. His background was as a General Manager in Fast Food Outlets. With his exemplary people skills and ability to train new hires, WMM was able to hire operations staff with little or no experience and develop them to high performing team members. The four business partners set up their meeting with a view to re-orient their business strategy in the context of changes coming to how work would look like when the economy reopened after the pandemic. The goal was to develop a business model which would be relevant with the hybrid work model which was likely to be the norm once post pandemic recovery takes shape. Maria began the meeting with a discussion what work would look like in the post pandemic era. Clients of WMM were in all age groups ranging from 25 - 48 and were office workers. Due to their workload they preferred to buy food from a Quick Service Restaurant so that they can consume the food as and when their work schedule allowed for. With the hybrid work model, they would be attending office two or three days a week and work from home for the remainder. The food consumption pattern would shift from consumption only in the office(pre-pandemic), to consumption both at office and home (post-pandemic). The question therefore was: how can WMM adapt to this change in consumer behaviour? Julia thanked Maria for her insight and began her discussion. She pointed out at this time, there was a very short time lag between food being prepared at WMM and being consumed by the client. The time lag possibly was no more than two hours. As a result, consumers were able to eat freshly prepared food which was packed to retain the attributes of the cooked meal till it reached the consumer. She expressed opinion that the food production process needed a transformation. In addition to the food being prepared and delivered to the client for consumption, there has to be a secondary process where food would be prepared and packed. The packed food would retain its original attributes for 48 hours. Therefore, a client can order two versions of the same meal. One, which she can consume in the office within the next two hours and second, the packed version, which can be taken home, kept in the refrigerator, and consumed on the following day. She would come up with a list of menu items which could be cooked and packed. She requested Maria to explore the possibility of building a new brand based on the packed meals. At this point, Adam took over and pointed out that to implement this strategy, the following steps would be necessary . . . . A new facility, where food preparation and food packaging can happen Benchmarking studies to analyze performance of similar companies Product costing and estimation of manufacturing volume to meet financial goals Multi-channel marketing of packed food Tunde, pointed out that implementing the above, would lead to several operational issues as well. In order to resolve them, it may be necessary to incur additional fixed expenses. As a next step, they decided to retain the services of Conestoga Consulting (CC), a reputed consulting agency. The scope of work for CC would be to develop financial projections based on the above issues and provide a recommendation as to the best way forward for WMM. Page 4 12 MGMT 8500: F21 - capstone v3 Initial meeting with Conestoga Consulting: A group of five consultants met with the four business partners to develop a plan of action. It was decided that the consulting group will develop financial projections as requested and provide a report to WMM in two weeks Project work for Conestoga Consulting: Issue #1: New facility for WMM For acquiring the new facility, the consulting group wanted to evaluate both options of leasing the facility as well as an outright purchase. They gathered data which is presented in Appendix 1. Issue #2: Benchmarking studies of a similar company The consulting group decided to conduct a ratio analysis of a comparable company (Waterloo Corporation) and compare with that of the industry. This would allow them to provide feedback to WMM as to operating metrics they should follow in their new venture. Relevant data is presented in Appendix 2. Issue #3: Cost-Volume-Profit Analysis for proposed storefront The consulting group wanted to develop a Contribution Margin Income statement and conduct a Cost- Volume-Profit Analysis so that the estimated selling volume can be projected for a proposed storefront. Relevant data is presented in Appendix 3. Issue #4: Equipment replacement decision The consulting group wanted to develop calculations using the relevant costing model of 'Equipment Replacement Decision'. Relevant data is presented in Appendix 4. Required: At the end of the two-week period, the consulting group would be meeting with the business partners. Prepare a report showing all the calculations and your recommendations for all the four issues Appendix Three (Cost-Volume-Profit Analysis for a proposed storefront) Objective: In order to maximize revenue, the consulting group would like to analyze the feasibility of opening a storefront in an area with significant traffic. The store would focus on selling high value meals. Scenario: Cost card of meals to be sold at the store Item Revenue Variable expense Contribution Margin Per unit $30 15 $15 Fixed expenses per month Storefront rental Equipment depreciation Selling Administrative expenses Total 90,000 7,000 20,000 18,000 135,000 The store is projected to generate a net operating income of $ 125,000, after taxes. The applicable tax rate is 20% Methodology: The group would analyze the sales volume required to reach the target net operating income. Variable expense Contribution Margin 15 $15 Fixed expenses per month Storefront rental Equipment depreciation Selling Administrative expenses Total 90,000 7,000 20,000 18,000 135,000 The store is projected to generate a net operating income of $ 125,000, after taxes. The applicable tax rate is 20%. Methodology: The group would analyze the sales volume required to reach the target net operating income. Based on this sales figure, they would also like to iterate the staffing pattern and further analyze the impact on net operating income. The iteration would include, adding another two part time salespersons. As a result, the selling expenses will increase by $ 36,000 and will bring in an additional $ 60,000 in revenue. They would prepare a Contribution margin income statement and calculate the degree of operating leverage. s GO E 10