I need assistance with Section 2, question 5 and forward please? I have been stuck on this for days.

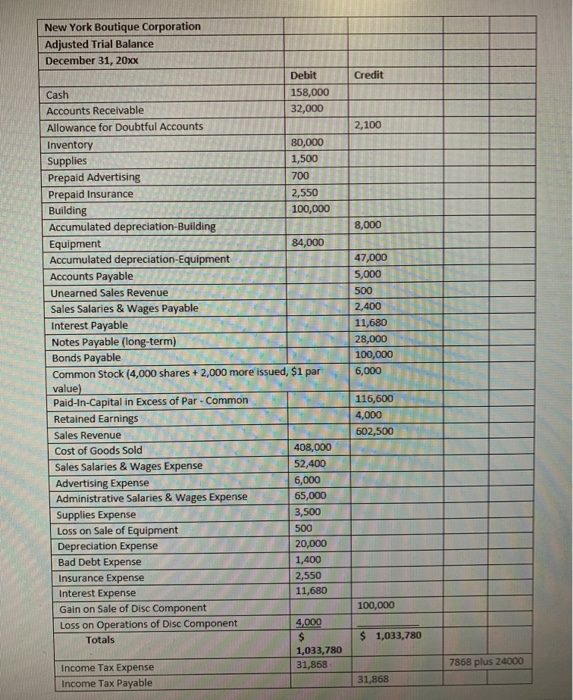

This is the adjusted trial balance

my jou en me what you want to do . . .5 - 700 Presented below is the December 31 unadjusted trial balance for New York Boutique, New York Boutique is a clothing line with multiple business components, including retail stores. The dollar values are in millions. New York Boutique Company Unadjusted Trial Balance December 31, 2017 Debit Credit Cash 68,500 Accounts Receivable 32,000 Allowance for Doubtful Accounts Inventory 80.000 Prepaid Insurance 5.100 Building 100,000 Equipment 84,000 Accumulated depreciation Equipment 35.000 Accounts Payable 5,000 Unearned Sales Revenue 3,000 Notes Payable (long-term) 28,000 Bonds Payable 100,000 Common Stock (6,000 shares outstanding, S1 6,000 value) Paid-In-Capital in Excess of Par - Common 116,600 Retained Earnings 10,000 Sales Revenue 600,000 Cost of Goods Sold 408,000 Sales Salaries & Wages Expense 50,000 Advertising Expense 6,700 65,000 Administrative Salaries & Wages Expense 5,000 Supplies Expense 754,300 754,300 Totals Instructions: 1 Create na Fyral al file for thie nrohlam Within the fila nlaca iaural antrias nn the first . . . 3 . . Section 1 2. Prepare adjusting joumal entries for the following as of December 31, 20xx (omit explanations). Create additional accounts as necessary. Record the journal entries using proper formatting. "Debits are recorded to the left in the journal and credits are indented to the right. Leave a blank line between each transaction. a) Depreciation on the equipment is depreciated based on a 7-year life using the straight line method (no salvage value). b) Depreciation on the building is depreciated based on a 25-year life using the double declining method (no salvage value). c) The company uses the analysis of receivables method (or aging of the receivables) for estimating bad debt expense. Based on an analysis, $2,100 will not be collected. ing this method means that the company must consider the amount that already exists in "Allowance for Doubtful Accounts" when calculating the adjusting entry. d) Insurance expired during the year S2,550. e) The note payable was issued on July 1 of the current year at a rate of 129 annually. Record the interest that has accrued on the note. f) Interest accrued on the bonds payable is $10,000. The bonds were sold at face value so there is no premium or discount. Record the interest that has accrued on the bonds. g) Sales salaries and wages earned but not paid $2,400. h) S700 worth of Advertising Expense has not yet been used i) Office Supplies on hand $1.500. charged to Supplies Expense when purchased. 1) Uneamed Sales Revenue earned by year end is $2,500. k) Paid dividends of $1 per share to common stockholders. Section 2 3. Prepare an adjusted trial balance to ensure that all of the corporation's accounts are up-to- date prior to proceeding to the Income Statement. (The adjusted trial balance is not part of your grade for the comprehensive problem). Additional information needed to prepare the financial statements: a. During the fiscal year, the company sold its Retail Stores division, which qualifies as a separate component according to GAAP. The Retail stores division was sold for a net selling price of $600,000. The Retail Stores division net assets had a book value of $500,000. The Retail Stores division reported a pre-tax loss on income from operations of $4,000. b. 2,000 additional shares of $1 par common stock were issued during the year for $21.00 per share. C. The company's tax rate is 25%. This years' taxes for both continuing operations and discontinued operations have not been recorded. You will need to journalize these taxes and update the accounts. **Round taxes to the nearest whole dollar (no cents). Include the journal entry for the taxes with the closing entries in section 4 5. Prepare a multiple-step income statement (round taxes to the nearest whole dollar). Use a three-column multiple-step income statement (the first column is for the account names and subsections, the 2nd and 3rd columns are for the dollar values). Make sure to include the proper heading for this financial statement. Use the appropriate subcategories such as Operating Expenses, Other Revenue (Expense), Discontinued Operations, etc. Begin each new column with a dollar sign. Place dollar signs in front of the first dollar values that start a column and on net income. In the comprehensive problem expenses will be listed by dollar value, higher dollar values listed first. (See number 4 above for additional information). Section 3 6. Prepare a statement of changes in shareholder's equity. (See number 4 above for additional information). Prepare a classified balance sheet. ** Use a four-column balance sheet (the first column is for the account names and subsections, the 2nd, 3rd, and 4th columns are for the dollar values). Use the appropriate subcategories such as current assets, investments, paid-in capital, etc. Begin each new column with a dollar sign. Place dollar signs in front of the first dollar values that start a column and on the totals. Current assets are listed in order of liquidity Property, plant, and equipment are listed according to their useful life, longer lives listed first. Liabilities are normally listed according to time to maturity or due date. In the comprehensive problem liabilities will be listed by dollar value, higher dollar values listed first. (See number 4 above for additional information). Section 4 8. Journalize the necessary closing entrie es as of December 31, 20xx. Credit 2,100 8,000 47,000 5.000 500 2.400 New York Boutique Corporation Adjusted Trial Balance December 31, 20xx Debit Cash 158,000 Accounts Receivable 32,000 Allowance for Doubtful Accounts Inventory 80,000 Supplies 1,500 Prepaid Advertising 700 Prepaid Insurance 2,550 Building 100,000 Accumulated depreciation-Building Equipment 84,000 Accumulated depreciation Equipment Accounts Payable Unearned Sales Revenue Sales Salaries & Wages Payable Interest Payable Notes Payable (long-term) Bonds Payable Common Stock (4,000 shares + 2,000 more issued, $i par . $1 par value) Paid-In-Capital in Excess of Par-Common Retained Earnings Sales Revenue Cost of Goods Sold 408,000 Sales Salaries & Wages Expense 52,400 Advertising Expense 6,000 Administrative Salaries & Wages Expense 65,000 Supplies Expense 3,500 Loss on Sale of Equipment 500 Depreciation Expense 20,000 Bad Debt Expense 1,400 Insurance Expense 2,550 Interest Expense 11,680 Gain on Sale of Disc Component Loss on Operations of Disc Component 4,000 11.680 28,000 100,000 6,000 116,600 4,000 602,500 100,000 Totals $ 1,033,780 1,033,780 31, 868 7 808 plus 24000 Income Tax Expense Income Tax Payable 31,868 my jou en me what you want to do . . .5 - 700 Presented below is the December 31 unadjusted trial balance for New York Boutique, New York Boutique is a clothing line with multiple business components, including retail stores. The dollar values are in millions. New York Boutique Company Unadjusted Trial Balance December 31, 2017 Debit Credit Cash 68,500 Accounts Receivable 32,000 Allowance for Doubtful Accounts Inventory 80.000 Prepaid Insurance 5.100 Building 100,000 Equipment 84,000 Accumulated depreciation Equipment 35.000 Accounts Payable 5,000 Unearned Sales Revenue 3,000 Notes Payable (long-term) 28,000 Bonds Payable 100,000 Common Stock (6,000 shares outstanding, S1 6,000 value) Paid-In-Capital in Excess of Par - Common 116,600 Retained Earnings 10,000 Sales Revenue 600,000 Cost of Goods Sold 408,000 Sales Salaries & Wages Expense 50,000 Advertising Expense 6,700 65,000 Administrative Salaries & Wages Expense 5,000 Supplies Expense 754,300 754,300 Totals Instructions: 1 Create na Fyral al file for thie nrohlam Within the fila nlaca iaural antrias nn the first . . . 3 . . Section 1 2. Prepare adjusting joumal entries for the following as of December 31, 20xx (omit explanations). Create additional accounts as necessary. Record the journal entries using proper formatting. "Debits are recorded to the left in the journal and credits are indented to the right. Leave a blank line between each transaction. a) Depreciation on the equipment is depreciated based on a 7-year life using the straight line method (no salvage value). b) Depreciation on the building is depreciated based on a 25-year life using the double declining method (no salvage value). c) The company uses the analysis of receivables method (or aging of the receivables) for estimating bad debt expense. Based on an analysis, $2,100 will not be collected. ing this method means that the company must consider the amount that already exists in "Allowance for Doubtful Accounts" when calculating the adjusting entry. d) Insurance expired during the year S2,550. e) The note payable was issued on July 1 of the current year at a rate of 129 annually. Record the interest that has accrued on the note. f) Interest accrued on the bonds payable is $10,000. The bonds were sold at face value so there is no premium or discount. Record the interest that has accrued on the bonds. g) Sales salaries and wages earned but not paid $2,400. h) S700 worth of Advertising Expense has not yet been used i) Office Supplies on hand $1.500. charged to Supplies Expense when purchased. 1) Uneamed Sales Revenue earned by year end is $2,500. k) Paid dividends of $1 per share to common stockholders. Section 2 3. Prepare an adjusted trial balance to ensure that all of the corporation's accounts are up-to- date prior to proceeding to the Income Statement. (The adjusted trial balance is not part of your grade for the comprehensive problem). Additional information needed to prepare the financial statements: a. During the fiscal year, the company sold its Retail Stores division, which qualifies as a separate component according to GAAP. The Retail stores division was sold for a net selling price of $600,000. The Retail Stores division net assets had a book value of $500,000. The Retail Stores division reported a pre-tax loss on income from operations of $4,000. b. 2,000 additional shares of $1 par common stock were issued during the year for $21.00 per share. C. The company's tax rate is 25%. This years' taxes for both continuing operations and discontinued operations have not been recorded. You will need to journalize these taxes and update the accounts. **Round taxes to the nearest whole dollar (no cents). Include the journal entry for the taxes with the closing entries in section 4 5. Prepare a multiple-step income statement (round taxes to the nearest whole dollar). Use a three-column multiple-step income statement (the first column is for the account names and subsections, the 2nd and 3rd columns are for the dollar values). Make sure to include the proper heading for this financial statement. Use the appropriate subcategories such as Operating Expenses, Other Revenue (Expense), Discontinued Operations, etc. Begin each new column with a dollar sign. Place dollar signs in front of the first dollar values that start a column and on net income. In the comprehensive problem expenses will be listed by dollar value, higher dollar values listed first. (See number 4 above for additional information). Section 3 6. Prepare a statement of changes in shareholder's equity. (See number 4 above for additional information). Prepare a classified balance sheet. ** Use a four-column balance sheet (the first column is for the account names and subsections, the 2nd, 3rd, and 4th columns are for the dollar values). Use the appropriate subcategories such as current assets, investments, paid-in capital, etc. Begin each new column with a dollar sign. Place dollar signs in front of the first dollar values that start a column and on the totals. Current assets are listed in order of liquidity Property, plant, and equipment are listed according to their useful life, longer lives listed first. Liabilities are normally listed according to time to maturity or due date. In the comprehensive problem liabilities will be listed by dollar value, higher dollar values listed first. (See number 4 above for additional information). Section 4 8. Journalize the necessary closing entrie es as of December 31, 20xx. Credit 2,100 8,000 47,000 5.000 500 2.400 New York Boutique Corporation Adjusted Trial Balance December 31, 20xx Debit Cash 158,000 Accounts Receivable 32,000 Allowance for Doubtful Accounts Inventory 80,000 Supplies 1,500 Prepaid Advertising 700 Prepaid Insurance 2,550 Building 100,000 Accumulated depreciation-Building Equipment 84,000 Accumulated depreciation Equipment Accounts Payable Unearned Sales Revenue Sales Salaries & Wages Payable Interest Payable Notes Payable (long-term) Bonds Payable Common Stock (4,000 shares + 2,000 more issued, $i par . $1 par value) Paid-In-Capital in Excess of Par-Common Retained Earnings Sales Revenue Cost of Goods Sold 408,000 Sales Salaries & Wages Expense 52,400 Advertising Expense 6,000 Administrative Salaries & Wages Expense 65,000 Supplies Expense 3,500 Loss on Sale of Equipment 500 Depreciation Expense 20,000 Bad Debt Expense 1,400 Insurance Expense 2,550 Interest Expense 11,680 Gain on Sale of Disc Component Loss on Operations of Disc Component 4,000 11.680 28,000 100,000 6,000 116,600 4,000 602,500 100,000 Totals $ 1,033,780 1,033,780 31, 868 7 808 plus 24000 Income Tax Expense Income Tax Payable 31,868