i need belp understanding the problems thank you so much.

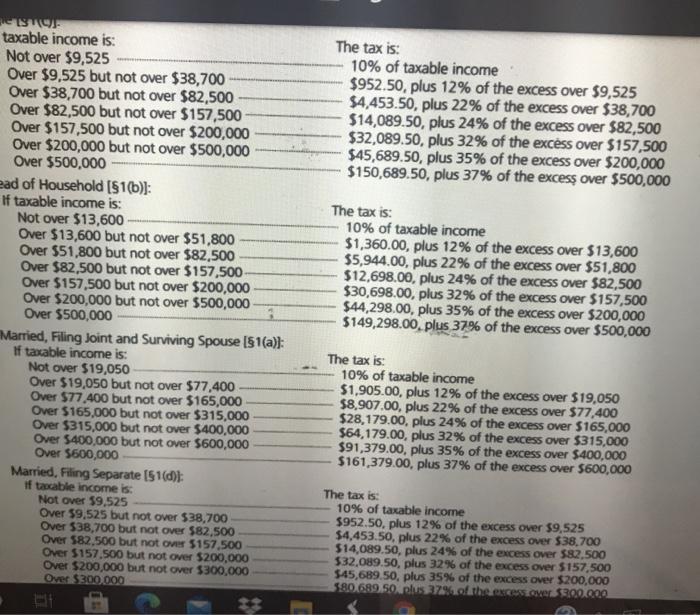

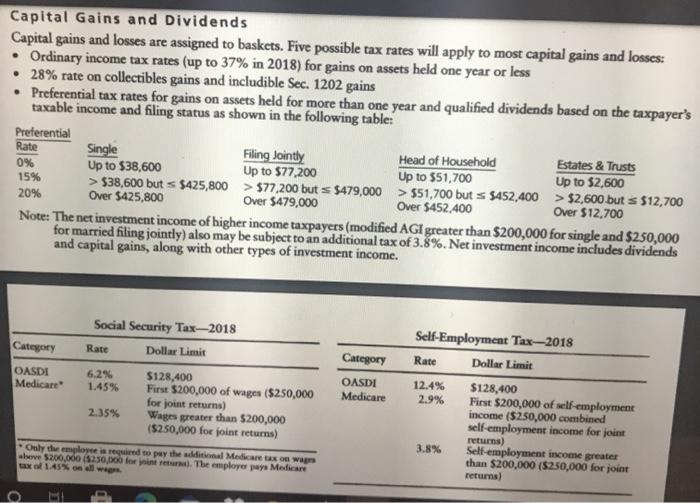

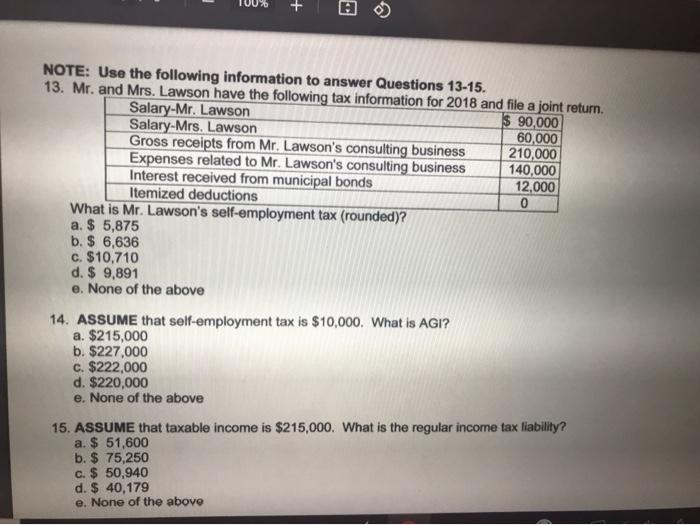

NOTE: Use the following information to answer Questions 13-15. 13. Mr. and Mrs. Lawson have the following tax information for 2018 and file a joint return. Salary-Mr. Lawson $ 90,000 Salary-Mrs. Lawson 60,000 Gross receipts from Mr. Lawson's consulting business 210,000 Expenses related to Mr. Lawson's consulting business 140,000 Interest received from municipal bonds 12,000 Itemized deductions 0 What is Mr. Lawson's self-employment tax (rounded)? a. $ 5,875 b. $ 6,636 c. $10,710 d. $ 9,891 e. None of the above 14. ASSUME that self-employment tax is $10,000. What is AGI? a. $215,000 b. $227.000 c. $222,000 d. $220,000 e. None of the above 15. ASSUME that taxable income is $215,000. What is the regular income tax liability? a $ 51,600 b.$ 75,250 c. $ 50,940 d. $ 40,179 e. None of the above The tax is: 10% of taxable income $952.50, plus 12% of the excess over $9,525 $4,453.50, plus 22% of the excess over $38,700 $14,089.50, plus 24% of the excess over $82,500 $32,089.50, plus 32% of the excess over $157,500 $45,689.50, plus 35% of the excess over $200,000 $150,689.50, plus 37% of the excess over $500,000 ES taxable income is: Not over $9,525 Over $9,525 but not over $38,700 Over $38,700 but not over $82,500 Over $82,500 but not over $157,500 Over $157,500 but not over $200,000 Over $200,000 but not over $500,000 Over $500,000 ead of Household ($1(b)]: If taxable income is: Not over $13,600 Over $13,600 but not over $51,800 Over $51,800 but not over $82,500 Over $82,500 but not over $157,500- Over $157,500 but not over $200,000 Over $200,000 but not over $500,000 Over $500,000 Married, Filing Joint and Surviving Spouse ($1(a)); If taxable income is: Not over $19,050 Over $19,050 but not over $77,400 Over $77.400 but not over $165,000 Over $165,000 but not over $315,000 Over $315,000 but not over $400,000 Over $400,000 but not over $600,000 Over $600,000 Married, Filing Separate [51(d)): If acable income is: Not over $9,525 Over 59,525 but not over 538,700 Over 538,700 but not over $82,500 Over 582,500 but not over 5157.500 Over 5157.500 but not over $200,000 Over $200,000 but not over $300,000 Over $300.000 The tax is: 10% of taxable income $1,360.00, plus 12% of the excess over $13,600 55,944.00, plus 22% of the excess over $51,800 $12,698.00, plus 24% of the excess over $82,500 $30,698.00, plus 32% of the excess over $157,500 $44,298.00, plus 35% of the excess over $200,000 $149,298.00, plus 37% of the excess over $500,000 The tax is: 10% of taxable income 51,905.00, plus 12% of the excess over 519,050 58.907.00, plus 22% of the excess over $77,400 $28,179.00, plus 24% of the excess over $165,000 564,179.00, plus 32% of the excess over $315,000 $91,379.00, plus 35% of the excess over $400,000 $161.379.00, plus 37% of the excess over 5600,000 The tax is: 10% of taxable income $952.50, plus 12% of the excess over $9,525 54,453.50, plus 22% of the excess over $38.700 $14,089.50, plus 24% of the excess over $82,500 532,089.50, plus 32% of the excess over $157,500 $45,689.50, plus 35% of the excess over $200,000 580.689.50.plus 27. the excesso 800.000 Capital Gains and Dividends Capital gains and losses are assigned to baskets. Five possible tax rates will apply to most capital gains and losses: Ordinary income tax rates (up to 37% in 2018) for gains on assets held one year or less 28% rate on collectibles gains and includible Sec. 1202 gains Preferential tax rates for gains on assets held for more than one year and qualified dividends based on the taxpayer's taxable income and filing status as shown in the following table: Preferential Rate Single Filing Jointly Head of Household Estates & Trusts 0% Up to $38,600 Up to $77,200 Up to 551,700 15% Up to $2,600 > $38,600 but s $425,800 > 577,200 but s $479,000 > 551,700 but s 5452,400 > $2,600 but $12,700 Over $425,800 Over $479,000 Over $452,400 Over $12,700 Note: The net investment income of higher income taxpayers (modified AGI greater than $200,000 for single and $250,000 for married filing jointly) also may be subject to an additional tax of 3.8%. Net investment income includes dividends and capital gains, along with other types of investment income. 20% Social Security Tax-2018 Rate Dollar Limit Category Category OASDI Medicare OASDI 6,2% 5128,400 Medicare 1.45% First $200,000 of wages ($250,000 for joint returns 2.35% Wages greater than $200,000 ($250,000 for joint returns) Only the employees red to pay the wal Medicare was bove $200,000 $250,000 forint. The employer pays Medicare Self-Employment Tax-2018 Rate Dollar Limit 12.4% $128,400 2.9% First $200,000 of self-employment income ($250,000 combined self-employment income for joint returns) 3.8% Self-employment income greater than $200,000 ($250,000 for joint returns) + NOTE: Use the following information to answer Questions 13-15. 13. Mr. and Mrs. Lawson have the following tax information for 2018 and file a joint return. Salary-Mr. Lawson $ 90,000 Salary-Mrs. Lawson 60,000 Gross receipts from Mr. Lawson's consulting business 210,000 Expenses related to Mr. Lawson's consulting business 140,000 Interest received from municipal bonds 12,000 Itemized deductions 0 What is Mr. Lawson's self-employment tax (rounded)? a. $ 5,875 b. $ 6,636 c. $10,710 d. $ 9,891 e. None of the above 14. ASSUME that self-employment tax is $10,000. What is AGI? a. $215,000 b. $227,000 c. $222,000 d. $220,000 e. None of the above 15. ASSUME that taxable income is $215,000. What is the regular income tax liability? a. $ 51,600 b. $ 75,250 c. $ 50,940 d. $ 40,179 e. None of the above