Answered step by step

Verified Expert Solution

Question

1 Approved Answer

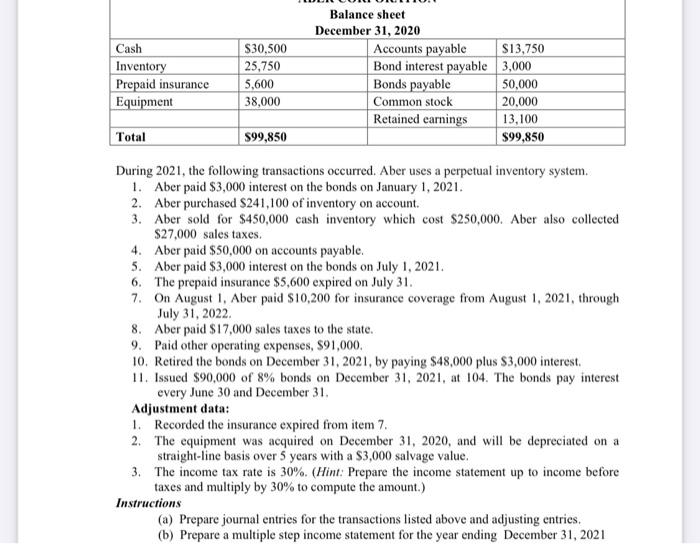

Detailed journal entries for adjustment data and income statement for part b is required. Balance sheet December 31, 2020 Accounts payable Cash S30,500 25,750 Inventory

Detailed journal entries for adjustment data and income statement for part b is required.

Balance sheet December 31, 2020 Accounts payable Cash S30,500 25,750 Inventory Prepaid insurance Equipment S13,750 Bond interest payable 3,000 50,000 20,000 Bonds payable 5,600 38,000 Common stock Retained earnings 13,100 Total $99,850 $99,850 During 2021, the following transactions occurred. Aber uses a perpetual inventory system. 1. Aber paid $3,000 interest on the bonds on January 1, 2021. 2. Aber purchased $241,100 of inventory on account. 3. Aber sold for $450,000 cash inventory which cost $250,000. Aber also collected $27,000 sales taxes. 4. Aber paid $50,000 on accounts payable. 5. Aber paid $3,000 interest on the bonds on July 1, 2021. 6. The prepaid insurance $5,600 expired on July 31. 7. On August 1, Aber paid $10,200 for insurance coverage from August 1, 2021, through July 31, 2022. 8. Aber paid $17,000 sales taxes to the state. 9. Paid other operating expenses, $91,000. 10. Retired the bonds on December 31, 2021, by paying $48,000 plus $3,000 interest. 11. Issued $90,000 of 8% bonds on December 31, 2021, at 104. The bonds pay interest every June 30 and December 31. Adjustment data: 1. Recorded the insurance expired from item 7. 2. The equipment was acquired on December 31, 2020, and will be depreciated on a straight-line basis over 5 years with a $3,000 salvage value. 3. The income tax rate is 30%. (Hint: Prepare the income statement up to income before taxes and multiply by 30% to compute the amount.) Instructions (a) Prepare journal entries for the transactions listed above and adjusting entries. (b) Prepare a multiple step income statement for the year ending December 31, 2021

Step by Step Solution

★★★★★

3.46 Rating (153 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Managerial Accounting Concepts

Authors: Edmonds, Tsay, olds

6th Edition

71220720, 78110890, 9780071220729, 978-0078110894