Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I need explanations Problem 6.12 Casper Landsten -- CIA (A) Casper Landsten is a foreign exchange trader for a bank in New York. He has

I need explanations

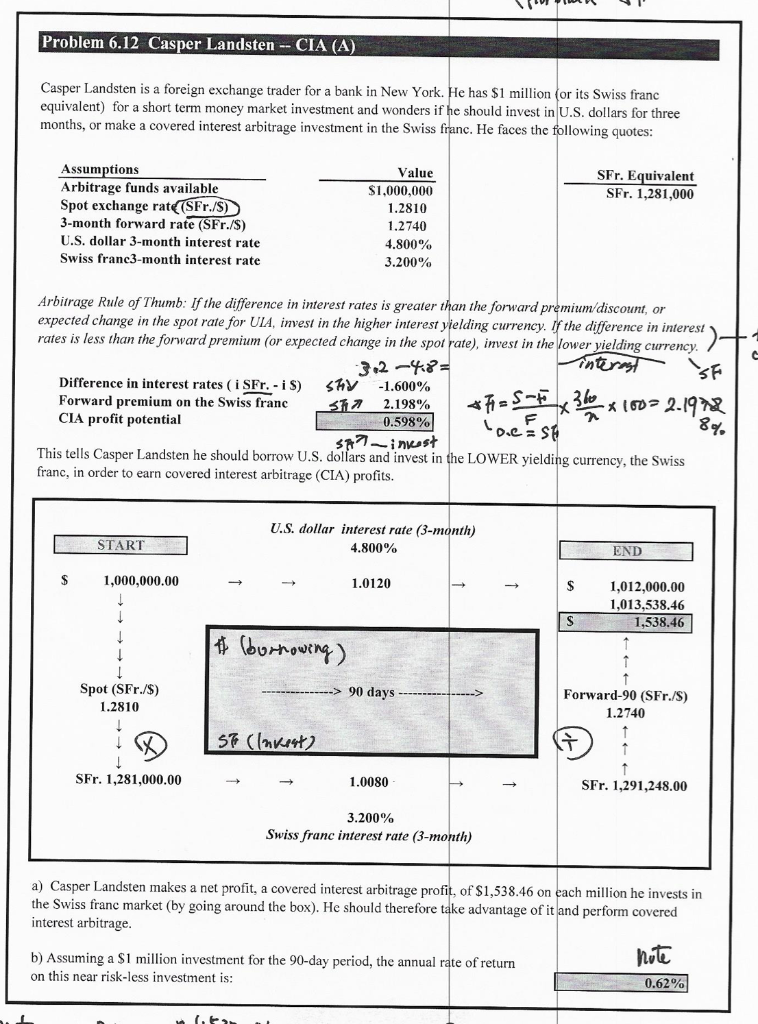

Problem 6.12 Casper Landsten -- CIA (A) Casper Landsten is a foreign exchange trader for a bank in New York. He has $1 million (or its Swiss franc equivalent) for a short term money market investment and wonders if he should invest in U.S. dollars for three months, or make a covered interest arbitrage investment in the Swiss franc. He faces the following quotes: SFr. Equivalent SFr. 1,281,000 Assumptions Arbitrage funds available Spot exchange rat& (SFr./S) 3-month forward rate (SFr./S) U.S. dollar 3-month interest rate Swiss franc3-month interest rate Value $1,000,000 1.2810 1.2740 4.800% 3.200% Arbitrage Rule of Thumb: if the difference in interest rates is greater than the forward premium/discount, or ) - rates is less than the forward premium (or expected change in the spot rate), invest in the lower yielding currency. 3.2 -48 inter SF Difference in interest rates (i SFr.-i S) 577 -1.600% Forward premium on the Swiss franc 572 2.198% . CIA profit potential 0.598% 8% SA?inkast This tells Casper Landsten he should borrow U.S. dollars and invest in the LOWER yielding rrency, the Swiss franc, in order to earn covered interest arbitrage (CIA) profits. *F=S-Fx 360 x 100-2.1978 loc=st U.S. dollar interest rate (3-month) 4.800% START END $ 1,000,000.00 1.0120 - $ 1,012,000.00 1,013,538.46 1,538.46 $ (bornowing 90 days Spot (SFr./$) 1.2810 + Forward-90 (SFr./S) 1.2740 57 (Invest) SFr. 1,281,000.00 1.0080 SFr. 1,291,248.00 3.200% Swiss franc interest rate (3-month) a) Casper Landsten makes a net profit, a covered interest arbitrage profit, of $1,538.46 on each million he invests in the Swiss franc market (by going around the box). He should therefore take advantage of it and perform covered interest arbitrage. b) Assuming a $1 million investment for the 90-day period, the annual rate of return note on this near risk-less investment is: 0.62% Problem 6.12 Casper Landsten -- CIA (A) Casper Landsten is a foreign exchange trader for a bank in New York. He has $1 million (or its Swiss franc equivalent) for a short term money market investment and wonders if he should invest in U.S. dollars for three months, or make a covered interest arbitrage investment in the Swiss franc. He faces the following quotes: SFr. Equivalent SFr. 1,281,000 Assumptions Arbitrage funds available Spot exchange rat& (SFr./S) 3-month forward rate (SFr./S) U.S. dollar 3-month interest rate Swiss franc3-month interest rate Value $1,000,000 1.2810 1.2740 4.800% 3.200% Arbitrage Rule of Thumb: if the difference in interest rates is greater than the forward premium/discount, or ) - rates is less than the forward premium (or expected change in the spot rate), invest in the lower yielding currency. 3.2 -48 inter SF Difference in interest rates (i SFr.-i S) 577 -1.600% Forward premium on the Swiss franc 572 2.198% . CIA profit potential 0.598% 8% SA?inkast This tells Casper Landsten he should borrow U.S. dollars and invest in the LOWER yielding rrency, the Swiss franc, in order to earn covered interest arbitrage (CIA) profits. *F=S-Fx 360 x 100-2.1978 loc=st U.S. dollar interest rate (3-month) 4.800% START END $ 1,000,000.00 1.0120 - $ 1,012,000.00 1,013,538.46 1,538.46 $ (bornowing 90 days Spot (SFr./$) 1.2810 + Forward-90 (SFr./S) 1.2740 57 (Invest) SFr. 1,281,000.00 1.0080 SFr. 1,291,248.00 3.200% Swiss franc interest rate (3-month) a) Casper Landsten makes a net profit, a covered interest arbitrage profit, of $1,538.46 on each million he invests in the Swiss franc market (by going around the box). He should therefore take advantage of it and perform covered interest arbitrage. b) Assuming a $1 million investment for the 90-day period, the annual rate of return note on this near risk-less investment is: 0.62%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Crimes

Authors: Maximilian Edelbacher, Peter Kratcoski, Michael Theil

1st Edition

0367866528, 978-0367866525