I need help completing these 2 tables

here is all the information that had been provided to me

I need help. Help me, please

I need help. Help me, please

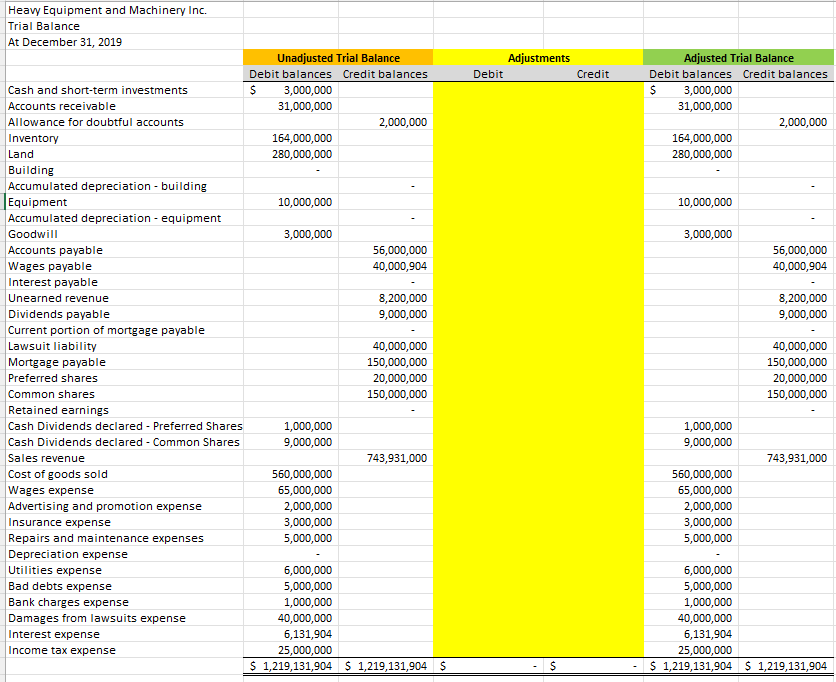

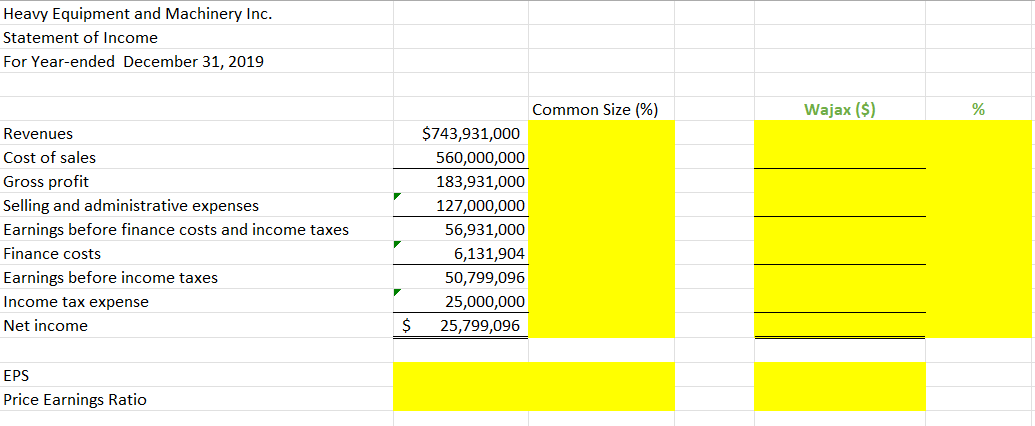

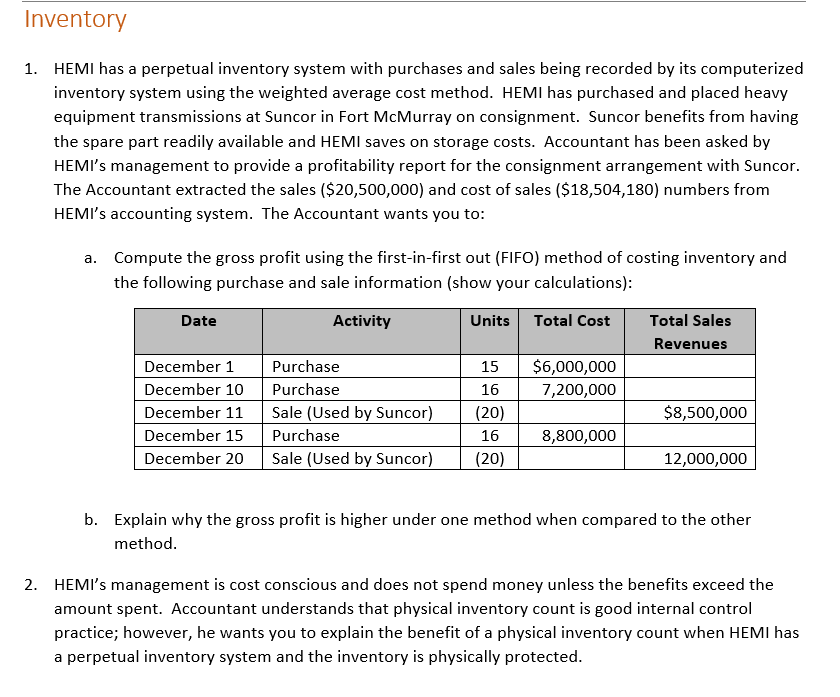

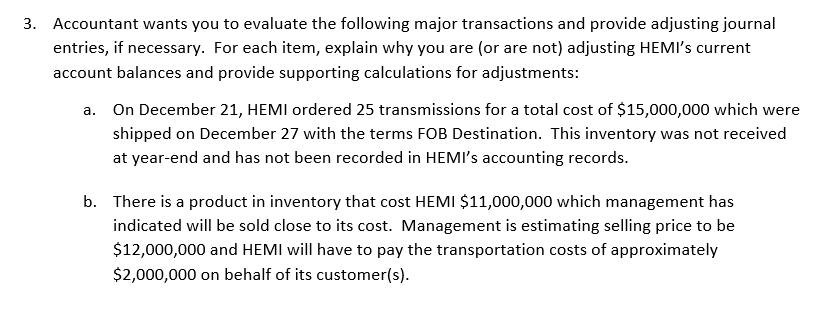

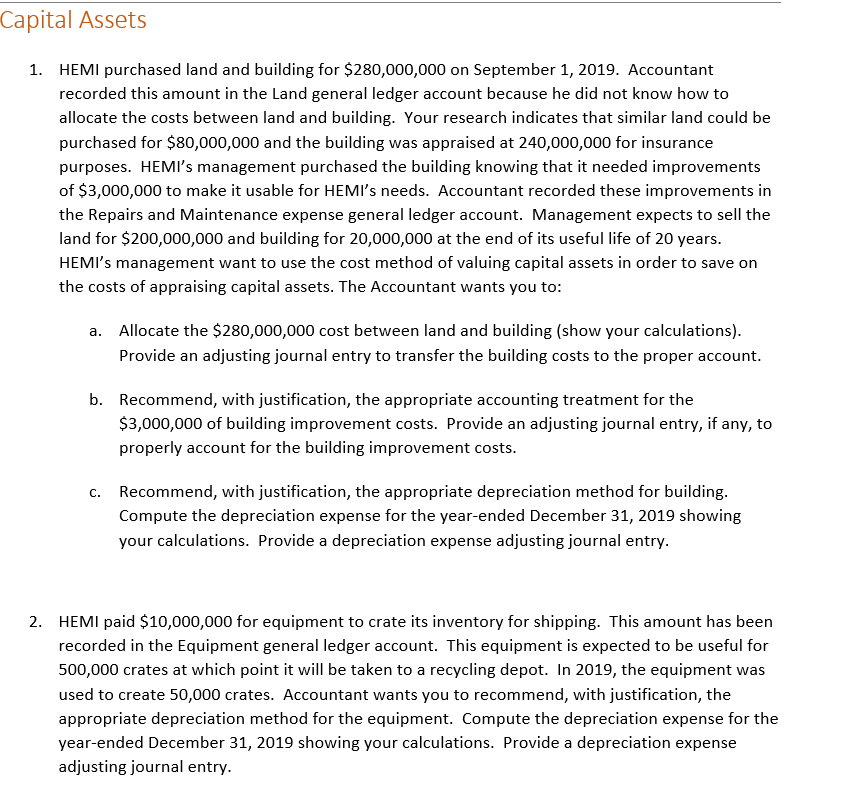

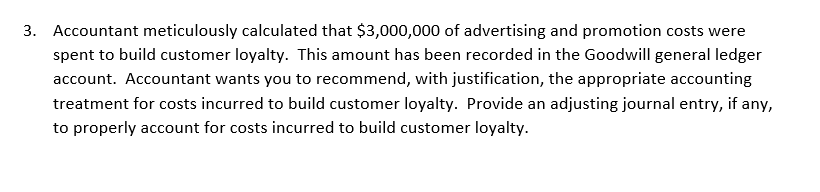

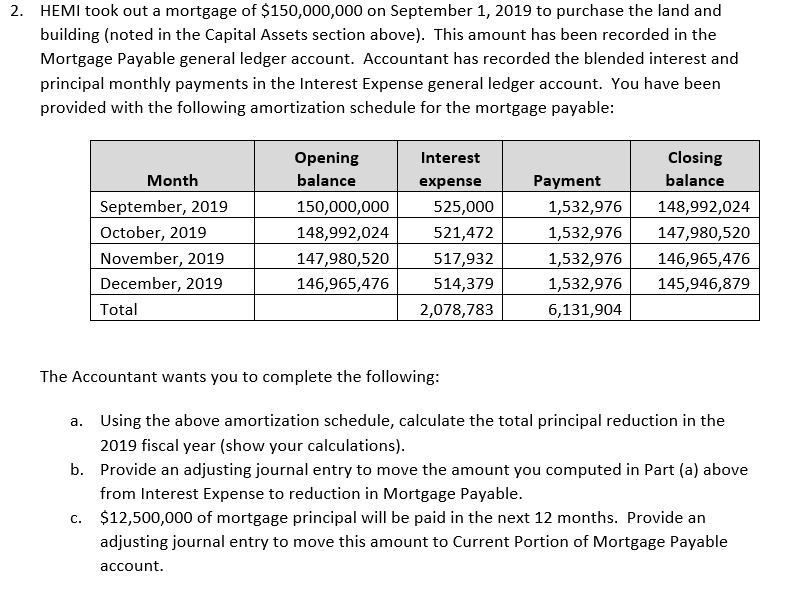

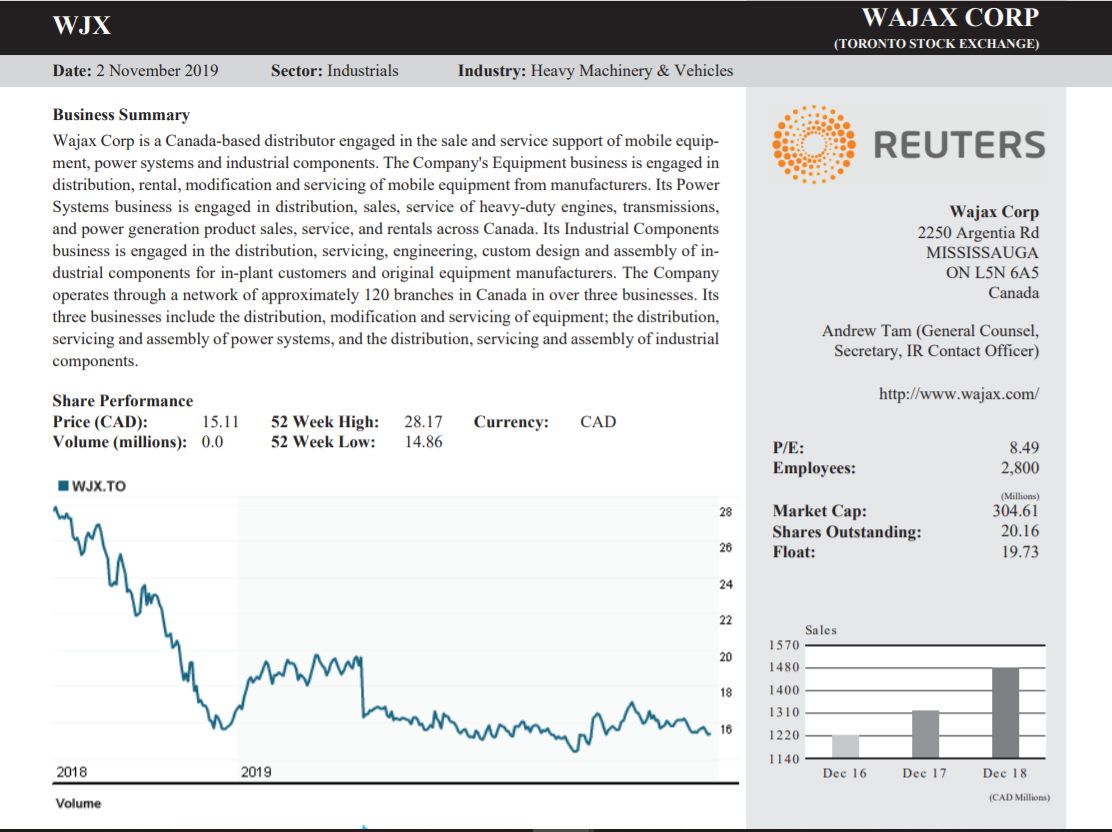

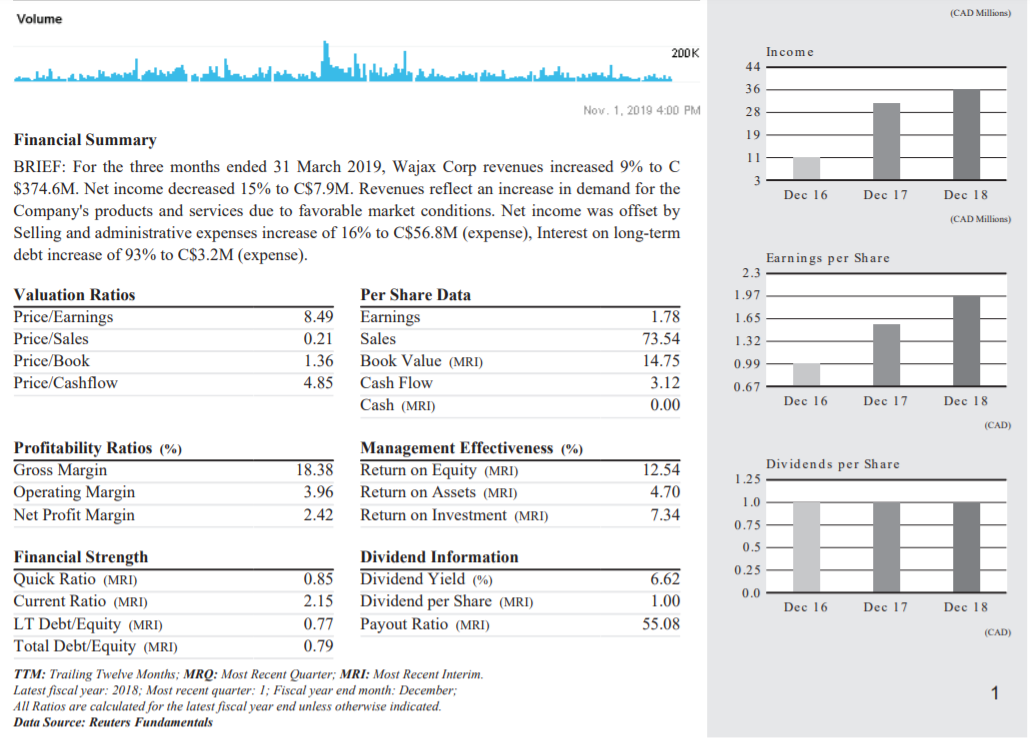

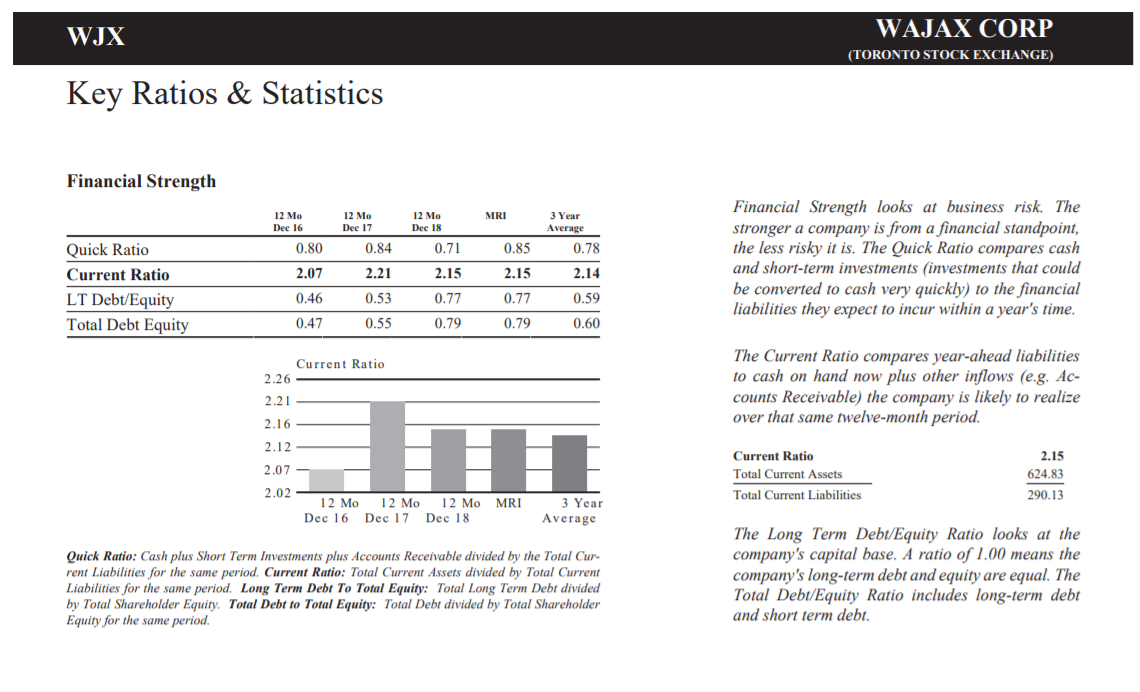

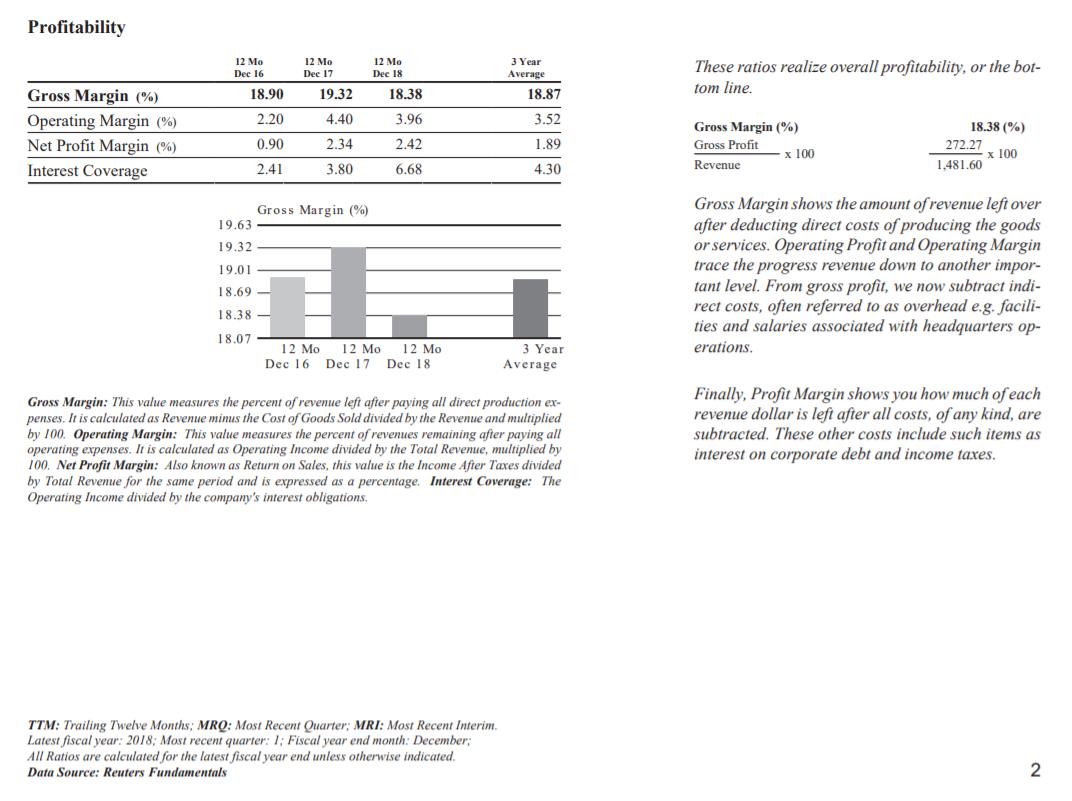

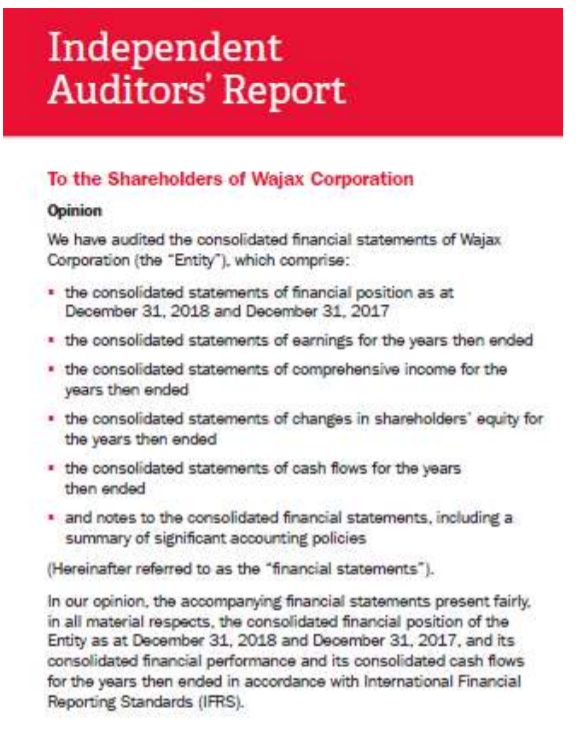

Adjustments Debit Credit Adjusted Trial Balance Debit balances Credit balances $ 3,000,000 31,000,000 2,000,000 164,000,000 280,000,000 10,000,000 3,000,000 56,000,000 40,000,904 8,200,000 9,000,000 Heavy Equipment and Machinery Inc. Trial Balance At December 31, 2019 Unadjusted Trial Balance Debit balances Credit balances Cash and short-term investments $ 3,000,000 Accounts receivable 31,000,000 Allowance for doubtful accounts 2,000,000 Inventory 164,000,000 Land 280,000,000 Building Accumulated depreciation - building Equipment 10,000,000 Accumulated depreciation - equipment Goodwill 3,000,000 Accounts payable 56,000,000 Wages payable 40,000,904 Interest payable Unearned revenue 8,200,000 Dividends payable 9,000,000 Current portion of mortgage payable Lawsuit liability 40,000,000 Mortgage payable 150,000,000 Preferred shares 20,000,000 Common shares 150,000,000 Retained earnings Cash Dividends declared - Preferred Shares 1,000,000 Cash Dividends declared - Common Shares 9,000,000 Sales revenue 743,931,000 Cost of goods sold 560,000,000 Wages expense 65,000,000 Advertising and promotion expense 2,000,000 Insurance expense 3,000,000 Repairs and maintenance expenses 5,000,000 Depreciation expense Utilities expense 6,000,000 Bad debts expense 5,000,000 Bank charges expense 1,000,000 Damages from lawsuits expense 40,000,000 Interest expense 6,131,904 Income tax expense 25,000,000 $ 1,219,131,904 $1,219,131,904 $ 40,000,000 150,000,000 20,000,000 150,000,000 1,000,000 9,000,000 743,931,000 560,000,000 65,000,000 2,000,000 3,000,000 5,000,000 6,000,000 5,000,000 1,000,000 40,000,000 6,131,904 25,000,000 $ 1,219,131,904 $1,219,131,904 Heavy Equipment and Machinery Inc. Statement of Income For Year-ended December 31, 2019 Wajax ($) % Revenues Cost of sales Gross profit Selling and administrative expenses Earnings before finance costs and income taxes Finance costs Earnings before income taxes Income tax expense Net income Common Size (%) $743,931,000 560,000,000 183,931,000 127,000,000 56,931,000 6,131,904 50,799,096 25,000,000 25,799,096 $ EPS Price Earnings Ratio Case Study Information . You have been hired as a Financial Consultant by Heavy Equipment and Machinery Inc. (HEMI). HEMI is a private corporation that has finished its first year of operations. HEMI's owners plan to list the business on the Toronto Stock Exchange (TSE) in the next 5 years; accordingly, are keen to have their financial statements reflect the business in the best light possible using the IFRS Accounting Standards. HEMI's operations are considered to be similar to Wajax Corporation listed on the TSE. In addition to the questions outlined below, the Accountant has provided you with the following two files: An Excel spreadsheet with information from the HEMI's accounting records and HEMI's Statement of Income created by formulas. Selected Wajax Corporation's publicly available financial information. Your consulting assignment requires you to complete the following: 1. Answer the Accountant's questions outlined below (including any necessary adjusting journal entries). 2. Post the adjusting journal entries that you have identified in Step #1 to the Excel trial balance spreadsheet. 3. Enter Wajax Corporation's 2018 Statement of Income beside HEMI's 2019 Statement of Income and enter the formulas to prepare common size Statements of Income for HEMI and Wajax Corporation. Inventory 1. HEMI has a perpetual inventory system with purchases and sales being recorded by its computerized inventory system using the weighted average cost method. HEMI has purchased and placed heavy equipment transmissions at Suncor in Fort McMurray on consignment. Suncor benefits from having the spare part readily available and HEMI saves on storage costs. Accountant has been asked by HEMI's management to provide a profitability report for the consignment arrangement with Suncor. The Accountant extracted the sales ($20,500,000) and cost of sales ($18,504,180) numbers from HEMI's accounting system. The Accountant wants you to: a. Compute the gross profit using the first-in-first out (FIFO) method of costing inventory and the following purchase and sale information (show your calculations): Date Activity Units Total Cost Total Sales Revenues $6,000,000 7,200,000 December 1 December 10 December 11 December 15 December 20 Purchase Purchase Sale (Used by Suncor) Purchase Sale (Used by Suncor) 15 16 (20) 16 (20) $8,500,000 8,800,000 12,000,000 b. Explain why the gross profit is higher under one method when compared to the other method. 2. HEMI's management is cost conscious and does not spend money unless the benefits exceed the amount spent. Accountant understands that physical inventory count is good internal control practice; however, he wants you to explain the benefit of a physical inventory count when HEMI has a perpetual inventory system and the inventory is physically protected. 3. Accountant wants you to evaluate the following major transactions and provide adjusting journal entries, if necessary. For each item, explain why you are (or are not) adjusting HEMI's current account balances and provide supporting calculations for adjustments: a. On December 21, HEMI ordered 25 transmissions for a total cost of $15,000,000 which were shipped on December 27 with the terms FOB Destination. This inventory was not received at year-end and has not been recorded in HEMI's accounting records. b. There is a product in inventory that cost HEMI $11,000,000 which management has indicated will be sold close to its cost. Management is estimating selling price to be $12,000,000 and HEMI will have to pay the transportation costs of approximately $2,000,000 on behalf of its customer(s). Capital Assets 1. HEMI purchased land and building for $280,000,000 on September 1, 2019. Accountant recorded this amount in the Land general ledger account because he did not know how to allocate the costs between land and building. Your research indicates that similar land could be purchased for $80,000,000 and the building was appraised at 240,000,000 for insurance purposes. HEMI's management purchased the building knowing that it needed improvements of $3,000,000 to make it usable for HEMI's needs. Accountant recorded these improvements in the Repairs and Maintenance expense general ledger account. Management expects to sell the land for $200,000,000 and building for 20,000,000 at the end of its useful life of 20 years. HEMI's management want to use the cost method of valuing capital assets in order to save on the costs of appraising capital assets. The Accountant wants you to: a. Allocate the $280,000,000 cost between land and building (show your calculations). Provide an adjusting journal entry to transfer the building costs to the proper account. b. Recommend, with justification, the appropriate accounting treatment for the $3,000,000 of building improvement costs. Provide an adjusting journal entry, if any, to properly account for the building improvement costs. C. Recommend, with justification, the appropriate depreciation method for building. Compute the depreciation expense for the year-ended December 31, 2019 showing your calculations. Provide a depreciation expense adjusting journal entry. 2. HEMI paid $10,000,000 for equipment to crate its inventory for shipping. This amount has been recorded in the Equipment general ledger account. This equipment is expected to be useful for 500,000 crates at which point it will be taken to a recycling depot. In 2019, the equipment was used to create 50,000 crates. Accountant wants you to recommend, with justification, the appropriate depreciation method for the equipment. Compute the depreciation expense for the year-ended December 31, 2019 showing your calculations. Provide a depreciation expense adjusting journal entry. a 3. Accountant meticulously calculated that $3,000,000 of advertising and promotion costs were spent to build customer loyalty. This amount has been recorded in the Goodwill general ledger account. Accountant wants you to recommend, with justification, the appropriate accounting treatment for costs incurred to build customer loyalty. Provide an adjusting journal entry, if any, to properly account for costs incurred to build customer loyalty. Current and long-term Liabilities 1. Yukon territorial government entered into an agreement with HEMI to open a warehouse in Whitehorse. The agreement required the Yukon territorial government to prepay $10,000,000 for future equipment purchases and to buy all of its equipment from HEMI over the next 5 years. The government also agreed to only use $9,000,000 of the prepayment (i.e., give HEMI a "breakage" if equipment is supplied from the Whitehorse warehouse). In 2019, HEMI supplied $1,800,000 of equipment from its Whitehorse warehouse. The Unearned Revenues general ledger account is at a balance of $8,200,000 ($10,000,000 less $1,800,000). No adjustment has been made for the "breakage". Accountant has computed the "breakage" revenue at $200,000 that HEMI can recognize for the year-ended December 31, 2019. Provide an adjusting journal entry to recognize the breakage revenue. 2. HEMI took out a mortgage of $150,000,000 on September 1, 2019 to purchase the land and building (noted in the Capital Assets section above). This amount has been recorded in the Mortgage Payable general ledger account. Accountant has recorded the blended interest and principal monthly payments in the Interest Expense general ledger account. You have been provided with the following amortization schedule for the mortgage payable: Month September, 2019 October, 2019 November, 2019 December, 2019 Total Opening balance 150,000,000 148,992,024 147,980,520 146,965,476 Interest expense 525,000 521,472 517,932 514,379 2,078,783 Payment 1,532,976 1,532,976 1,532,976 1,532,976 6,131,904 Closing balance 148,992,024 147,980,520 146,965,476 145,946,879 The Accountant wants you to complete the following: a. Using the above amortization schedule, calculate the total principal reduction in the 2019 fiscal year (show your calculations). b. Provide an adjusting journal entry to move the amount you computed in Part (a) above from Interest Expense to reduction in Mortgage Payable. C. $12,500,000 of mortgage principal will be paid in the next 12 months. Provide an adjusting journal entry to move this amount to Current Portion of Mortgage Payable account. 3. On November 4, 2019 HEMI was sued for $50,000,000 in damages because one of its transmissions was incorrectly installed by Suncor repair technicians which resulted in significant property damage. HEMI's lawyers are of the opinion that the lawsuit is without any merit as the transmission supplied by HEMI was working properly. The problem was with the incorrect installation of the transmission. HEMI plans to defend itself through the Canadian legal system which may take as long as 3 years. The Accountant has recorded $40,000,000 in the general ledger because $10,000,000 of damages will be paid for HEMI's insurance company. The Accountant wants you to explain the appropriate accounting treatment for this contingent loss. Provide an adjusting journal entry, if any, to properly account this contingent loss considering that the contingent loss is already recorded in the accounting records. Shareholders' Equity 1. Preferred shares cash dividends have been declared and paid. Common share dividends have been declared, but not paid. HEMI is authorized to issue 50,000,000. HEMI issued 12,000,000 common shares on January 2, 2019 (i.e., these were the shares outstanding prior to the stock dividend). HEMI's common shares are valued at $21 per share. The Accountant wants you to use/disregard any relevant information in preparing the trial balance. WJX WAJAX CORP (TORONTO STOCK EXCHANGE) Date: 2 November 2019 Sector: Industrials Industry: Heavy Machinery & Vehicles REUTERS Business Summary Wajax Corp is a Canada-based distributor engaged in the sale and service support of mobile equip- ment, power systems and industrial components. The Company's Equipment business is engaged in distribution, rental, modification and servicing of mobile equipment from manufacturers. Its Power Systems business is engaged in distribution, sales, service of heavy-duty engines, transmissions, and power generation product sales, service, and rentals across Canada. Its Industrial Components business is engaged in the distribution, servicing, engineering, custom design and assembly of in- dustrial components for in-plant customers and original equipment manufacturers. The Company operates through a network of approximately 120 branches in Canada in over three businesses. Its three businesses include the distribution, modification and servicing of equipment; the distribution, servicing and assembly of power systems, and the distribution, servicing and assembly of industrial components. Wajax Corp 2250 Argentia Rd MISSISSAUGA ON L5N 6A5 Canada Andrew Tam (General Counsel, Secretary, IR Contact Officer) http://www.wajax.com/ Share Performance Price (CAD): 15.11 Volume (millions): 0.0 52 Week High: 52 Week Low: CAD 28.17 14.86 Currency: P/E: Employees: 8.49 2,800 WJX.TO 28 Market Cap: Shares Outstanding: Float: (Millions) 304.61 20.16 19.73 26 24 22 Sales 20 1570 1480 wamy 18 1400 1310 16 1220 1140 2018 2019 Dec 16 Dec 17 Dec 18 (CAD Millions) Volume (CAD Millions) Volume 200K Income 44 36 Nov. 1, 2019 4:00 PM 28 19 11 3 Financial Summary BRIEF: For the three months ended 31 March 2019, Wajax Corp revenues increased 9% to C $374.6M. Net income decreased 15% to C$7.9M. Revenues reflect an increase in demand for the Company's products and services due to favorable market conditions. Net income was offset by Selling and administrative expenses increase of 16% to C$56.8M (expense), Interest on long-term debt increase of 93% to C$3.2M (expense). Dec 16 Dec 17 Dec 18 (CAD Millions) Earnings per Share 2.3 1.97 1.65 Valuation Ratios Price/Earnings Price/Sales Price/Book Price/Cashflow Per Share Data Earnings Sales Book Value (MRI) Cash Flow 8.49 0.21 1.36 4.85 1.32 1.78 73.54 14.75 3.12 0.00 0.99 0.67 Cash (MRI) Dec 16 Dec 17 Dec 18 (CAD) 18.38 Dividends per Share Profitability Ratios (%) Gross Margin Operating Margin Net Profit Margin Management Effectiveness (%) Return on Equity (MRI) Return on Assets (MRI) Return on Investment (MRI) 3.96 2.42 12.54 4.70 7.34 1.25 1.0 0.75 0.5 0.25 0.0 6.62 1.00 55.08 Dec 16 Dec 17 Dec 18 (CAD) Financial Strength Dividend Information Quick Ratio (MRI) 0.85 Dividend Yield (%) Current Ratio (MRI) 2.15 Dividend per Share (MRI) LT Debt/Equity (MRI) 0.77 Payout Ratio (MRI) Total Debt/Equity (MRI) 0.79 TTM: Trailing Twelve Months; MRQ: Most Recent Quarter; MRI: Most Recent Interim. Latest fiscal year: 2018, Most recent quarter: 1; Fiscal year end month: December; All Ratios are calculated for the latest fiscal year end unless otherwise indicated. Data Source: Reuters Fundamentals 1 WJX WAJAX CORP (TORONTO STOCK EXCHANGE) Key Ratios & Statistics Financial Strength MRI 12 Mo Dec 16 12 Mo Dec 17 12 Mo Dec 18 0.71 3 Year Average 0.78 0.80 0.84 0.85 Financial Strength looks at business risk. The stronger a company is from a financial standpoint, the less risky it is. The Quick Ratio compares cash and short-term investments (investments that could be converted to cash very quickly) to the financial liabilities they expect to incur within a year's time. 2.07 2.21 2.15 2.15 Quick Ratio Current Ratio LT Debt/Equity Total Debt Equity 2.14 0.46 0.53 0.77 0.77 0.59 0.47 0.55 0.79 0.79 0.60 Current Ratio 2.26 2.21 The Current Ratio compares year-ahead liabilities to cash on hand now plus other inflows (e.g. Ac- counts Receivable) the company is likely to realize over that same twelve-month period. 2.16 2.12 H 2.07 Current Ratio Total Current Assets Total Current Liabilities 2.15 624.83 290.13 2.02 12 Mo Dec 16 12 Mo 12 Mo MRI Dec 17 Dec 18 3 Year Average Quick Ratio: Cash plus Short Term Investments plus Accounts Receivable divided by the Total Cur- rent Liabilities for the same period. Current Ratio: Total Current Assets divided by Total Current Liabilities for the same period. Long Term Debt To Total Equity: Total Long Term Debt divided by Total Shareholder Equity. Total Debt to Total Equity: Total Debt divided by Total Shareholder Equity for the same period. The Long Term Debt/Equity Ratio looks at the company's capital base. A ratio of 1.00 means the company's long-term debt and equity are equal. The Total Debt/Equity Ratio includes long-term debt and short term debt. Profitability 12 Mo Dec 16 12 Mo Dec 17 12 Mo Dec 18 3 Year Average These ratios realize overall profitability, or the bot- tom line. 18.90 19.32 18.38 18.87 2.20 4.40 3.96 3.52 Gross Margin (%) Operating Margin (%) Net Profit Margin (%) Interest Coverage 2.34 2.42 0.90 2.41 1.89 4.30 Gross Margin (%) Gross Profit x 100 Revenue 18.38 (%) 272.27 x 100 1,481.60 3.80 6.68 Gross Margin (%) 19.63 19.32 19.01 Gross Margin shows the amount of revenue left over after deducting direct costs of producing the goods or services. Operating Profit and Operating Margin trace the progress revenue down to another impor- tant level. From gross profit, we now subtract indi- rect costs, often referred to as overhead e.g. facili- ties and salaries associated with headquarters op- erations. 18.69 18.38 18.07 12 Mo 12 Mo 12 Mo Dec 16 Dec 17 Dec 18 3 Year Average Gross Margin: This value measures the percent of revenue left after paying all direct production ex- penses. It is calculated as Revenue minus the Cost of Goods Sold divided by the Revenue and multiplied by 100. Operating Margin: This value measures the percent of revenues remaining after paying all operating expenses. It is calculated as Operating Income divided by the Total Revenue, multiplied by 100. Net Profit Margin: Also known as Return on Sales, this value is the Income After Taxes divided by Total Revenue for the same period and is expressed as a percentage. Interest Coverage: The Operating Income divided by the company's interest obligations. Finally, Profit Margin shows you how much of each revenue dollar is left after all costs, of any kind, are subtracted. These other costs include such items as interest on corporate debt and income taxes. TTM: Trailing Twelve Months; MRQ: Most Recent Quarter; MRI: Most Recent Interim. Latest fiscal year: 2018; Most recent quarter: 1; Fiscal year end month: December All Ratios are calculated for the latest fiscal year end unless otherwise indicated. Data Source: Reuters Fundamentals 2 Independent Auditors' Report To the Shareholders of Wajax Corporation Opinion We have audited the consolidated financial statements of Wajax Corporation (the "Entity ). which comprise: the consolidated statements of financial position as at December 31, 2018 and December 31, 2017 the consolidated statements of earnings for the years then ended . the consolidated statements of comprehensive income for the years then ended . the consolidated statements of changes in shareholders' equity for the years then ended the consolidated statements of cash flows for the years then ended and notes to the consolidated financial statements, including a summary of significant accounting policies (Hereinafter referred to as the financial statements"). In our opinion, the accompanying financial statements present fairly. in all material respects, the consolidated financial position of the Entity as at December 31, 2018 and December 31, 2017, and its consolidated financial performance and its consolidated cash flows for the years then ended in accordance with International Financial Reporting Standards (IFRS). Consolidated Statements of Earnings For the year ended December 21 in thousands of Canadian dollar, except per ahare data Revenue Cost of sales Gross profit Selling and administrative expenses Restructuring and other related costs Earnings before finance costs and income taxes Finance costs Earnings before income taxes Income tax expense Net earnings Note 2018 2017 As adjusted (Note 5 8. 19 $1,481,597 $1,318,731 9 1,209,330 1.068,713 272,267 250,018 209,522 196,816 21 4,143 21 58,602 53,181 22 8,775 15,249 49,827 37,932 23 13,975 10,551 $ 35,852 $ 27,381 Basic earnings per share Diluted earnings per share 17 S 17 1.82 $ 1.78 1.40 1.36 Adjustments Debit Credit Adjusted Trial Balance Debit balances Credit balances $ 3,000,000 31,000,000 2,000,000 164,000,000 280,000,000 10,000,000 3,000,000 56,000,000 40,000,904 8,200,000 9,000,000 Heavy Equipment and Machinery Inc. Trial Balance At December 31, 2019 Unadjusted Trial Balance Debit balances Credit balances Cash and short-term investments $ 3,000,000 Accounts receivable 31,000,000 Allowance for doubtful accounts 2,000,000 Inventory 164,000,000 Land 280,000,000 Building Accumulated depreciation - building Equipment 10,000,000 Accumulated depreciation - equipment Goodwill 3,000,000 Accounts payable 56,000,000 Wages payable 40,000,904 Interest payable Unearned revenue 8,200,000 Dividends payable 9,000,000 Current portion of mortgage payable Lawsuit liability 40,000,000 Mortgage payable 150,000,000 Preferred shares 20,000,000 Common shares 150,000,000 Retained earnings Cash Dividends declared - Preferred Shares 1,000,000 Cash Dividends declared - Common Shares 9,000,000 Sales revenue 743,931,000 Cost of goods sold 560,000,000 Wages expense 65,000,000 Advertising and promotion expense 2,000,000 Insurance expense 3,000,000 Repairs and maintenance expenses 5,000,000 Depreciation expense Utilities expense 6,000,000 Bad debts expense 5,000,000 Bank charges expense 1,000,000 Damages from lawsuits expense 40,000,000 Interest expense 6,131,904 Income tax expense 25,000,000 $ 1,219,131,904 $1,219,131,904 $ 40,000,000 150,000,000 20,000,000 150,000,000 1,000,000 9,000,000 743,931,000 560,000,000 65,000,000 2,000,000 3,000,000 5,000,000 6,000,000 5,000,000 1,000,000 40,000,000 6,131,904 25,000,000 $ 1,219,131,904 $1,219,131,904 Heavy Equipment and Machinery Inc. Statement of Income For Year-ended December 31, 2019 Wajax ($) % Revenues Cost of sales Gross profit Selling and administrative expenses Earnings before finance costs and income taxes Finance costs Earnings before income taxes Income tax expense Net income Common Size (%) $743,931,000 560,000,000 183,931,000 127,000,000 56,931,000 6,131,904 50,799,096 25,000,000 25,799,096 $ EPS Price Earnings Ratio Case Study Information . You have been hired as a Financial Consultant by Heavy Equipment and Machinery Inc. (HEMI). HEMI is a private corporation that has finished its first year of operations. HEMI's owners plan to list the business on the Toronto Stock Exchange (TSE) in the next 5 years; accordingly, are keen to have their financial statements reflect the business in the best light possible using the IFRS Accounting Standards. HEMI's operations are considered to be similar to Wajax Corporation listed on the TSE. In addition to the questions outlined below, the Accountant has provided you with the following two files: An Excel spreadsheet with information from the HEMI's accounting records and HEMI's Statement of Income created by formulas. Selected Wajax Corporation's publicly available financial information. Your consulting assignment requires you to complete the following: 1. Answer the Accountant's questions outlined below (including any necessary adjusting journal entries). 2. Post the adjusting journal entries that you have identified in Step #1 to the Excel trial balance spreadsheet. 3. Enter Wajax Corporation's 2018 Statement of Income beside HEMI's 2019 Statement of Income and enter the formulas to prepare common size Statements of Income for HEMI and Wajax Corporation. Inventory 1. HEMI has a perpetual inventory system with purchases and sales being recorded by its computerized inventory system using the weighted average cost method. HEMI has purchased and placed heavy equipment transmissions at Suncor in Fort McMurray on consignment. Suncor benefits from having the spare part readily available and HEMI saves on storage costs. Accountant has been asked by HEMI's management to provide a profitability report for the consignment arrangement with Suncor. The Accountant extracted the sales ($20,500,000) and cost of sales ($18,504,180) numbers from HEMI's accounting system. The Accountant wants you to: a. Compute the gross profit using the first-in-first out (FIFO) method of costing inventory and the following purchase and sale information (show your calculations): Date Activity Units Total Cost Total Sales Revenues $6,000,000 7,200,000 December 1 December 10 December 11 December 15 December 20 Purchase Purchase Sale (Used by Suncor) Purchase Sale (Used by Suncor) 15 16 (20) 16 (20) $8,500,000 8,800,000 12,000,000 b. Explain why the gross profit is higher under one method when compared to the other method. 2. HEMI's management is cost conscious and does not spend money unless the benefits exceed the amount spent. Accountant understands that physical inventory count is good internal control practice; however, he wants you to explain the benefit of a physical inventory count when HEMI has a perpetual inventory system and the inventory is physically protected. 3. Accountant wants you to evaluate the following major transactions and provide adjusting journal entries, if necessary. For each item, explain why you are (or are not) adjusting HEMI's current account balances and provide supporting calculations for adjustments: a. On December 21, HEMI ordered 25 transmissions for a total cost of $15,000,000 which were shipped on December 27 with the terms FOB Destination. This inventory was not received at year-end and has not been recorded in HEMI's accounting records. b. There is a product in inventory that cost HEMI $11,000,000 which management has indicated will be sold close to its cost. Management is estimating selling price to be $12,000,000 and HEMI will have to pay the transportation costs of approximately $2,000,000 on behalf of its customer(s). Capital Assets 1. HEMI purchased land and building for $280,000,000 on September 1, 2019. Accountant recorded this amount in the Land general ledger account because he did not know how to allocate the costs between land and building. Your research indicates that similar land could be purchased for $80,000,000 and the building was appraised at 240,000,000 for insurance purposes. HEMI's management purchased the building knowing that it needed improvements of $3,000,000 to make it usable for HEMI's needs. Accountant recorded these improvements in the Repairs and Maintenance expense general ledger account. Management expects to sell the land for $200,000,000 and building for 20,000,000 at the end of its useful life of 20 years. HEMI's management want to use the cost method of valuing capital assets in order to save on the costs of appraising capital assets. The Accountant wants you to: a. Allocate the $280,000,000 cost between land and building (show your calculations). Provide an adjusting journal entry to transfer the building costs to the proper account. b. Recommend, with justification, the appropriate accounting treatment for the $3,000,000 of building improvement costs. Provide an adjusting journal entry, if any, to properly account for the building improvement costs. C. Recommend, with justification, the appropriate depreciation method for building. Compute the depreciation expense for the year-ended December 31, 2019 showing your calculations. Provide a depreciation expense adjusting journal entry. 2. HEMI paid $10,000,000 for equipment to crate its inventory for shipping. This amount has been recorded in the Equipment general ledger account. This equipment is expected to be useful for 500,000 crates at which point it will be taken to a recycling depot. In 2019, the equipment was used to create 50,000 crates. Accountant wants you to recommend, with justification, the appropriate depreciation method for the equipment. Compute the depreciation expense for the year-ended December 31, 2019 showing your calculations. Provide a depreciation expense adjusting journal entry. a 3. Accountant meticulously calculated that $3,000,000 of advertising and promotion costs were spent to build customer loyalty. This amount has been recorded in the Goodwill general ledger account. Accountant wants you to recommend, with justification, the appropriate accounting treatment for costs incurred to build customer loyalty. Provide an adjusting journal entry, if any, to properly account for costs incurred to build customer loyalty. Current and long-term Liabilities 1. Yukon territorial government entered into an agreement with HEMI to open a warehouse in Whitehorse. The agreement required the Yukon territorial government to prepay $10,000,000 for future equipment purchases and to buy all of its equipment from HEMI over the next 5 years. The government also agreed to only use $9,000,000 of the prepayment (i.e., give HEMI a "breakage" if equipment is supplied from the Whitehorse warehouse). In 2019, HEMI supplied $1,800,000 of equipment from its Whitehorse warehouse. The Unearned Revenues general ledger account is at a balance of $8,200,000 ($10,000,000 less $1,800,000). No adjustment has been made for the "breakage". Accountant has computed the "breakage" revenue at $200,000 that HEMI can recognize for the year-ended December 31, 2019. Provide an adjusting journal entry to recognize the breakage revenue. 2. HEMI took out a mortgage of $150,000,000 on September 1, 2019 to purchase the land and building (noted in the Capital Assets section above). This amount has been recorded in the Mortgage Payable general ledger account. Accountant has recorded the blended interest and principal monthly payments in the Interest Expense general ledger account. You have been provided with the following amortization schedule for the mortgage payable: Month September, 2019 October, 2019 November, 2019 December, 2019 Total Opening balance 150,000,000 148,992,024 147,980,520 146,965,476 Interest expense 525,000 521,472 517,932 514,379 2,078,783 Payment 1,532,976 1,532,976 1,532,976 1,532,976 6,131,904 Closing balance 148,992,024 147,980,520 146,965,476 145,946,879 The Accountant wants you to complete the following: a. Using the above amortization schedule, calculate the total principal reduction in the 2019 fiscal year (show your calculations). b. Provide an adjusting journal entry to move the amount you computed in Part (a) above from Interest Expense to reduction in Mortgage Payable. C. $12,500,000 of mortgage principal will be paid in the next 12 months. Provide an adjusting journal entry to move this amount to Current Portion of Mortgage Payable account. 3. On November 4, 2019 HEMI was sued for $50,000,000 in damages because one of its transmissions was incorrectly installed by Suncor repair technicians which resulted in significant property damage. HEMI's lawyers are of the opinion that the lawsuit is without any merit as the transmission supplied by HEMI was working properly. The problem was with the incorrect installation of the transmission. HEMI plans to defend itself through the Canadian legal system which may take as long as 3 years. The Accountant has recorded $40,000,000 in the general ledger because $10,000,000 of damages will be paid for HEMI's insurance company. The Accountant wants you to explain the appropriate accounting treatment for this contingent loss. Provide an adjusting journal entry, if any, to properly account this contingent loss considering that the contingent loss is already recorded in the accounting records. Shareholders' Equity 1. Preferred shares cash dividends have been declared and paid. Common share dividends have been declared, but not paid. HEMI is authorized to issue 50,000,000. HEMI issued 12,000,000 common shares on January 2, 2019 (i.e., these were the shares outstanding prior to the stock dividend). HEMI's common shares are valued at $21 per share. The Accountant wants you to use/disregard any relevant information in preparing the trial balance. WJX WAJAX CORP (TORONTO STOCK EXCHANGE) Date: 2 November 2019 Sector: Industrials Industry: Heavy Machinery & Vehicles REUTERS Business Summary Wajax Corp is a Canada-based distributor engaged in the sale and service support of mobile equip- ment, power systems and industrial components. The Company's Equipment business is engaged in distribution, rental, modification and servicing of mobile equipment from manufacturers. Its Power Systems business is engaged in distribution, sales, service of heavy-duty engines, transmissions, and power generation product sales, service, and rentals across Canada. Its Industrial Components business is engaged in the distribution, servicing, engineering, custom design and assembly of in- dustrial components for in-plant customers and original equipment manufacturers. The Company operates through a network of approximately 120 branches in Canada in over three businesses. Its three businesses include the distribution, modification and servicing of equipment; the distribution, servicing and assembly of power systems, and the distribution, servicing and assembly of industrial components. Wajax Corp 2250 Argentia Rd MISSISSAUGA ON L5N 6A5 Canada Andrew Tam (General Counsel, Secretary, IR Contact Officer) http://www.wajax.com/ Share Performance Price (CAD): 15.11 Volume (millions): 0.0 52 Week High: 52 Week Low: CAD 28.17 14.86 Currency: P/E: Employees: 8.49 2,800 WJX.TO 28 Market Cap: Shares Outstanding: Float: (Millions) 304.61 20.16 19.73 26 24 22 Sales 20 1570 1480 wamy 18 1400 1310 16 1220 1140 2018 2019 Dec 16 Dec 17 Dec 18 (CAD Millions) Volume (CAD Millions) Volume 200K Income 44 36 Nov. 1, 2019 4:00 PM 28 19 11 3 Financial Summary BRIEF: For the three months ended 31 March 2019, Wajax Corp revenues increased 9% to C $374.6M. Net income decreased 15% to C$7.9M. Revenues reflect an increase in demand for the Company's products and services due to favorable market conditions. Net income was offset by Selling and administrative expenses increase of 16% to C$56.8M (expense), Interest on long-term debt increase of 93% to C$3.2M (expense). Dec 16 Dec 17 Dec 18 (CAD Millions) Earnings per Share 2.3 1.97 1.65 Valuation Ratios Price/Earnings Price/Sales Price/Book Price/Cashflow Per Share Data Earnings Sales Book Value (MRI) Cash Flow 8.49 0.21 1.36 4.85 1.32 1.78 73.54 14.75 3.12 0.00 0.99 0.67 Cash (MRI) Dec 16 Dec 17 Dec 18 (CAD) 18.38 Dividends per Share Profitability Ratios (%) Gross Margin Operating Margin Net Profit Margin Management Effectiveness (%) Return on Equity (MRI) Return on Assets (MRI) Return on Investment (MRI) 3.96 2.42 12.54 4.70 7.34 1.25 1.0 0.75 0.5 0.25 0.0 6.62 1.00 55.08 Dec 16 Dec 17 Dec 18 (CAD) Financial Strength Dividend Information Quick Ratio (MRI) 0.85 Dividend Yield (%) Current Ratio (MRI) 2.15 Dividend per Share (MRI) LT Debt/Equity (MRI) 0.77 Payout Ratio (MRI) Total Debt/Equity (MRI) 0.79 TTM: Trailing Twelve Months; MRQ: Most Recent Quarter; MRI: Most Recent Interim. Latest fiscal year: 2018, Most recent quarter: 1; Fiscal year end month: December; All Ratios are calculated for the latest fiscal year end unless otherwise indicated. Data Source: Reuters Fundamentals 1 WJX WAJAX CORP (TORONTO STOCK EXCHANGE) Key Ratios & Statistics Financial Strength MRI 12 Mo Dec 16 12 Mo Dec 17 12 Mo Dec 18 0.71 3 Year Average 0.78 0.80 0.84 0.85 Financial Strength looks at business risk. The stronger a company is from a financial standpoint, the less risky it is. The Quick Ratio compares cash and short-term investments (investments that could be converted to cash very quickly) to the financial liabilities they expect to incur within a year's time. 2.07 2.21 2.15 2.15 Quick Ratio Current Ratio LT Debt/Equity Total Debt Equity 2.14 0.46 0.53 0.77 0.77 0.59 0.47 0.55 0.79 0.79 0.60 Current Ratio 2.26 2.21 The Current Ratio compares year-ahead liabilities to cash on hand now plus other inflows (e.g. Ac- counts Receivable) the company is likely to realize over that same twelve-month period. 2.16 2.12 H 2.07 Current Ratio Total Current Assets Total Current Liabilities 2.15 624.83 290.13 2.02 12 Mo Dec 16 12 Mo 12 Mo MRI Dec 17 Dec 18 3 Year Average Quick Ratio: Cash plus Short Term Investments plus Accounts Receivable divided by the Total Cur- rent Liabilities for the same period. Current Ratio: Total Current Assets divided by Total Current Liabilities for the same period. Long Term Debt To Total Equity: Total Long Term Debt divided by Total Shareholder Equity. Total Debt to Total Equity: Total Debt divided by Total Shareholder Equity for the same period. The Long Term Debt/Equity Ratio looks at the company's capital base. A ratio of 1.00 means the company's long-term debt and equity are equal. The Total Debt/Equity Ratio includes long-term debt and short term debt. Profitability 12 Mo Dec 16 12 Mo Dec 17 12 Mo Dec 18 3 Year Average These ratios realize overall profitability, or the bot- tom line. 18.90 19.32 18.38 18.87 2.20 4.40 3.96 3.52 Gross Margin (%) Operating Margin (%) Net Profit Margin (%) Interest Coverage 2.34 2.42 0.90 2.41 1.89 4.30 Gross Margin (%) Gross Profit x 100 Revenue 18.38 (%) 272.27 x 100 1,481.60 3.80 6.68 Gross Margin (%) 19.63 19.32 19.01 Gross Margin shows the amount of revenue left over after deducting direct costs of producing the goods or services. Operating Profit and Operating Margin trace the progress revenue down to another impor- tant level. From gross profit, we now subtract indi- rect costs, often referred to as overhead e.g. facili- ties and salaries associated with headquarters op- erations. 18.69 18.38 18.07 12 Mo 12 Mo 12 Mo Dec 16 Dec 17 Dec 18 3 Year Average Gross Margin: This value measures the percent of revenue left after paying all direct production ex- penses. It is calculated as Revenue minus the Cost of Goods Sold divided by the Revenue and multiplied by 100. Operating Margin: This value measures the percent of revenues remaining after paying all operating expenses. It is calculated as Operating Income divided by the Total Revenue, multiplied by 100. Net Profit Margin: Also known as Return on Sales, this value is the Income After Taxes divided by Total Revenue for the same period and is expressed as a percentage. Interest Coverage: The Operating Income divided by the company's interest obligations. Finally, Profit Margin shows you how much of each revenue dollar is left after all costs, of any kind, are subtracted. These other costs include such items as interest on corporate debt and income taxes. TTM: Trailing Twelve Months; MRQ: Most Recent Quarter; MRI: Most Recent Interim. Latest fiscal year: 2018; Most recent quarter: 1; Fiscal year end month: December All Ratios are calculated for the latest fiscal year end unless otherwise indicated. Data Source: Reuters Fundamentals 2 Independent Auditors' Report To the Shareholders of Wajax Corporation Opinion We have audited the consolidated financial statements of Wajax Corporation (the "Entity ). which comprise: the consolidated statements of financial position as at December 31, 2018 and December 31, 2017 the consolidated statements of earnings for the years then ended . the consolidated statements of comprehensive income for the years then ended . the consolidated statements of changes in shareholders' equity for the years then ended the consolidated statements of cash flows for the years then ended and notes to the consolidated financial statements, including a summary of significant accounting policies (Hereinafter referred to as the financial statements"). In our opinion, the accompanying financial statements present fairly. in all material respects, the consolidated financial position of the Entity as at December 31, 2018 and December 31, 2017, and its consolidated financial performance and its consolidated cash flows for the years then ended in accordance with International Financial Reporting Standards (IFRS). Consolidated Statements of Earnings For the year ended December 21 in thousands of Canadian dollar, except per ahare data Revenue Cost of sales Gross profit Selling and administrative expenses Restructuring and other related costs Earnings before finance costs and income taxes Finance costs Earnings before income taxes Income tax expense Net earnings Note 2018 2017 As adjusted (Note 5 8. 19 $1,481,597 $1,318,731 9 1,209,330 1.068,713 272,267 250,018 209,522 196,816 21 4,143 21 58,602 53,181 22 8,775 15,249 49,827 37,932 23 13,975 10,551 $ 35,852 $ 27,381 Basic earnings per share Diluted earnings per share 17 S 17 1.82 $ 1.78 1.40 1.36