Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I NEED HELP FINDING THE ARM PLEASE!!! WITH THE INFORMATION ABOVE! Wildcat Investment Company, LLC decided to purchase the investment property at 2912 N. Main

I NEED HELP FINDING THE ARM PLEASE!!! WITH THE INFORMATION ABOVE!

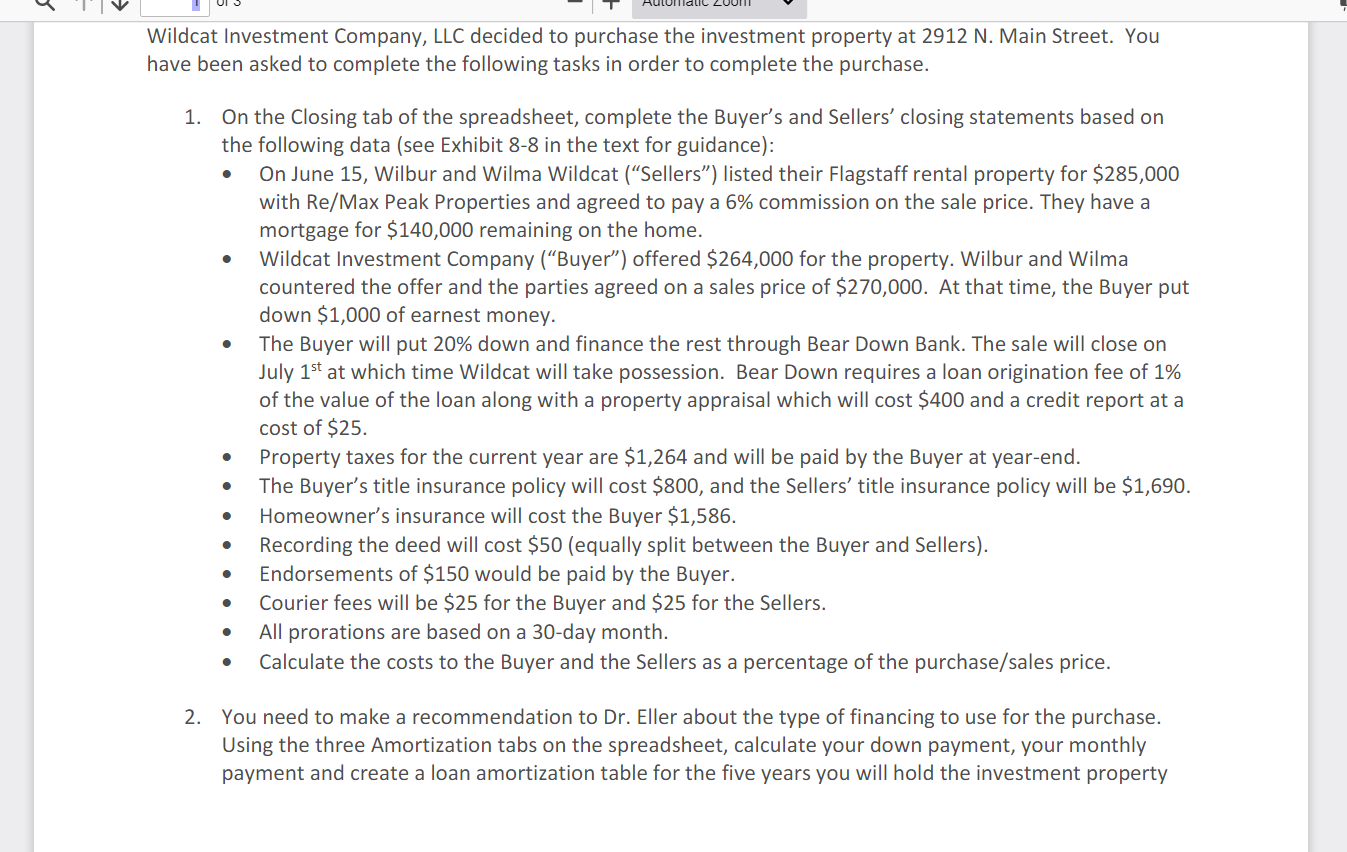

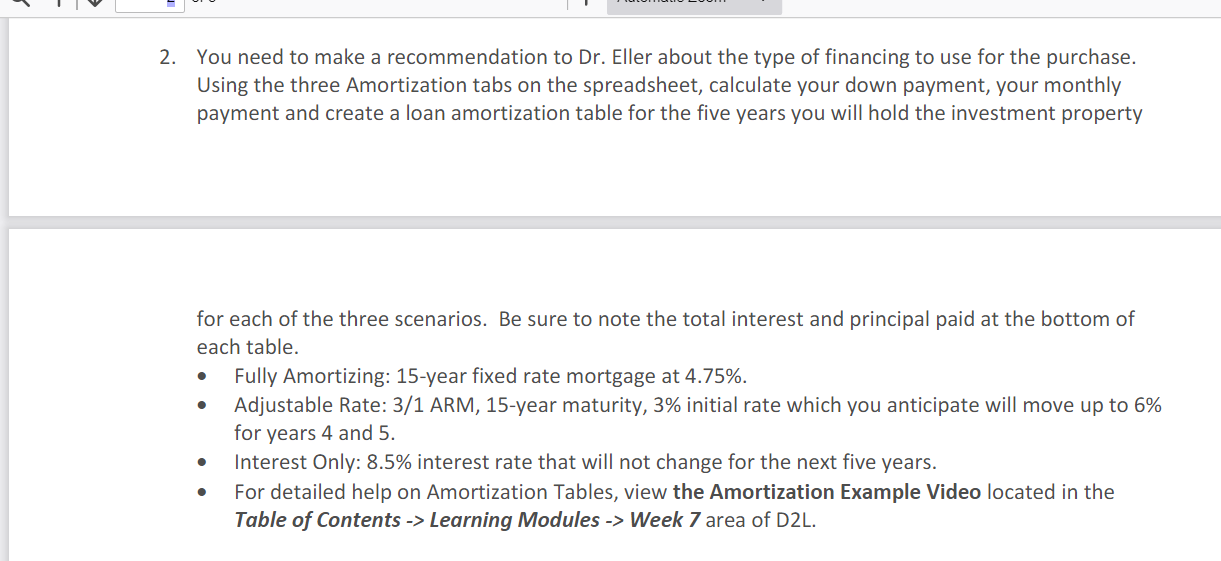

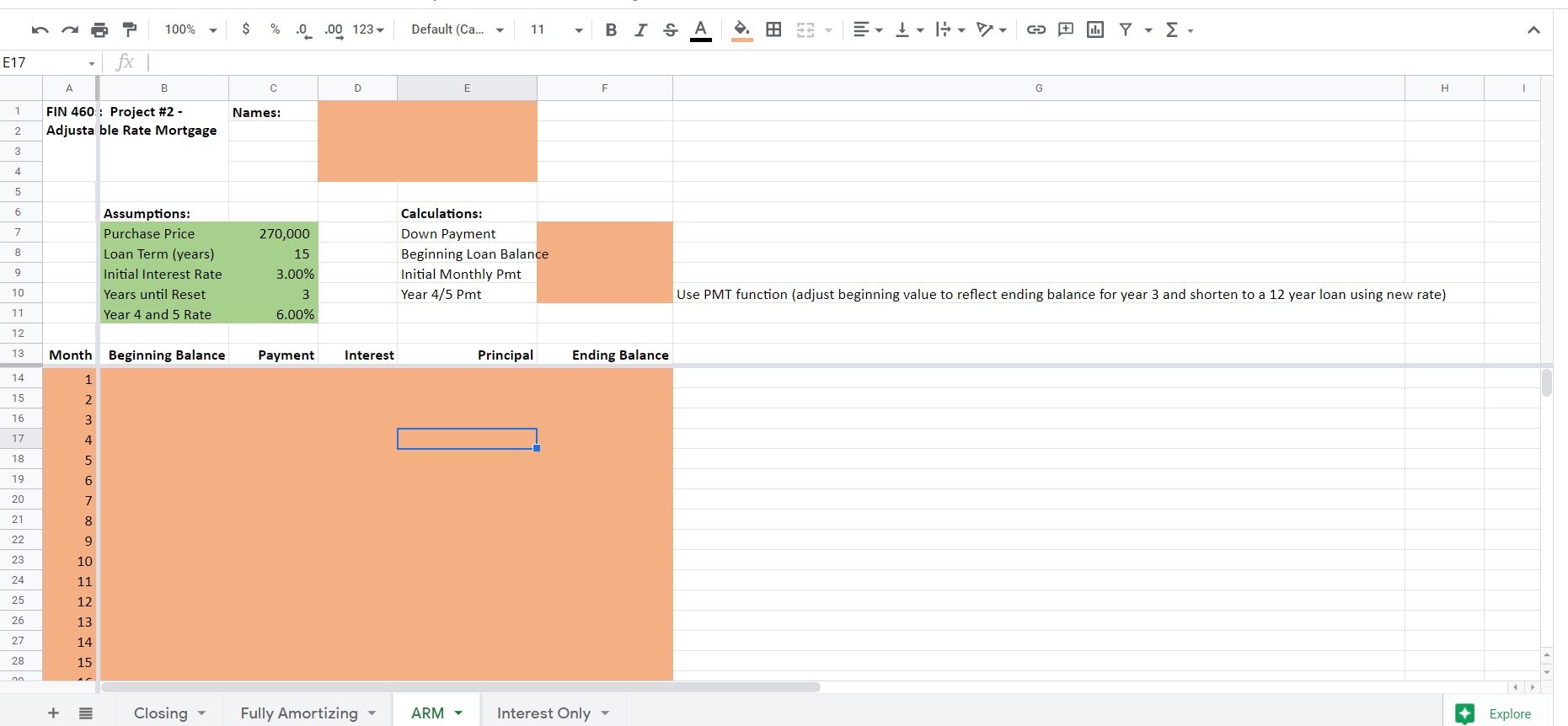

Wildcat Investment Company, LLC decided to purchase the investment property at 2912 N. Main Street. You have been asked to complete the following tasks in order to complete the purchase. 1. On the Closing tab of the spreadsheet, complete the Buyer's and Sellers' closing statements based on the following data (see Exhibit 8-8 in the text for guidance): On June 15, Wilbur and Wilma Wildcat (Sellers) listed their Flagstaff rental property for $285,000 with Re/Max Peak Properties and agreed to pay a 6% commission on the sale price. They have a mortgage for $140,000 remaining on the home. Wildcat Investment Company (Buyer) offered $264,000 for the property. Wilbur and Wilma countered the offer and the parties agreed on a sales price of $270,000. At that time, the Buyer put down $1,000 of earnest money. The Buyer will put 20% down and finance the rest through Bear Down Bank. The sale will close on July 1st at which time Wildcat will take possession. Bear Down requires a loan origination fee of 1% of the value of the loan along with a property appraisal which will cost $400 and a credit report at a cost of $25. Property taxes for the current year are $1,264 and will be paid by the Buyer at year-end. The Buyer's title insurance policy will cost $800, and the Sellers' title insurance policy will be $1,690. Homeowner's insurance will cost the Buyer $1,586. Recording the deed will cost $50 (equally split between the Buyer and Sellers). Endorsements of $150 would be paid by the Buyer. Courier fees will be $25 for the Buyer and $25 for the Sellers. All prorations are based on a 30-day month. Calculate the costs to the Buyer and the Sellers as a percentage of the purchase/sales price. . . 2. You need to make a recommendation to Dr. Eller about the type of financing to use for the purchase. Using the three Amortization tabs on the spreadsheet, calculate your down payment, your monthly payment and create a loan amortization table for the five years you will hold the investment property 2. You need to make a recommendation to Dr. Eller about the type of financing to use for the purchase. Using the three Amortization tabs on the spreadsheet, calculate your down payment, your monthly payment and create a loan amortization table for the five years you will hold the investment property for each of the three scenarios. Be sure to note the total interest and principal paid at the bottom of each table. Fully Amortizing: 15-year fixed rate mortgage at 4.75%. Adjustable Rate: 3/1 ARM, 15-year maturity, 3% initial rate which you anticipate will move up to 6% for years 4 and 5. Interest Only: 8.5% interest rate that will not change for the next five years. For detailed help on Amortization Tables, view the Amortization Example Video located in the Table of Contents -> Learning Modules -> Week 7 area of D2L. . 100% $ % 0.00 123 Default (Ca... - 11 B I A. 17 IV cu 1. - - E17 fx A B D E F G H 1 1 Names: FIN 460: Project #2 - Adjustable Rate Mortgage 2 3 4 5 6 7 8 Assumptions: Purchase Price Loan Term (years) Initial Interest Rate Years until Reset Year 4 and 5 Rate Calculations: Down Payment Beginning Loan Balance Initial Monthly Pmt Year 4/5 Pmt 270,000 15 3.00% 3 6.00% 9 10 Use PMT function (adjust beginning value to reflect ending balance for year 3 and shorten to a 12 year loan using new rate) 11 12 13 Month Beginning Balance Payment Interest Principal Ending Balance 14 1 15 2 3 16 17 4 18 19 20 5 6 7 8 9 21 22 23 10 11 24 25 12 26 13 27 14 15 28 + = MINI Closing Fully Amortizing ARM - Interest Only Explore Wildcat Investment Company, LLC decided to purchase the investment property at 2912 N. Main Street. You have been asked to complete the following tasks in order to complete the purchase. 1. On the Closing tab of the spreadsheet, complete the Buyer's and Sellers' closing statements based on the following data (see Exhibit 8-8 in the text for guidance): On June 15, Wilbur and Wilma Wildcat (Sellers) listed their Flagstaff rental property for $285,000 with Re/Max Peak Properties and agreed to pay a 6% commission on the sale price. They have a mortgage for $140,000 remaining on the home. Wildcat Investment Company (Buyer) offered $264,000 for the property. Wilbur and Wilma countered the offer and the parties agreed on a sales price of $270,000. At that time, the Buyer put down $1,000 of earnest money. The Buyer will put 20% down and finance the rest through Bear Down Bank. The sale will close on July 1st at which time Wildcat will take possession. Bear Down requires a loan origination fee of 1% of the value of the loan along with a property appraisal which will cost $400 and a credit report at a cost of $25. Property taxes for the current year are $1,264 and will be paid by the Buyer at year-end. The Buyer's title insurance policy will cost $800, and the Sellers' title insurance policy will be $1,690. Homeowner's insurance will cost the Buyer $1,586. Recording the deed will cost $50 (equally split between the Buyer and Sellers). Endorsements of $150 would be paid by the Buyer. Courier fees will be $25 for the Buyer and $25 for the Sellers. All prorations are based on a 30-day month. Calculate the costs to the Buyer and the Sellers as a percentage of the purchase/sales price. . . 2. You need to make a recommendation to Dr. Eller about the type of financing to use for the purchase. Using the three Amortization tabs on the spreadsheet, calculate your down payment, your monthly payment and create a loan amortization table for the five years you will hold the investment property 2. You need to make a recommendation to Dr. Eller about the type of financing to use for the purchase. Using the three Amortization tabs on the spreadsheet, calculate your down payment, your monthly payment and create a loan amortization table for the five years you will hold the investment property for each of the three scenarios. Be sure to note the total interest and principal paid at the bottom of each table. Fully Amortizing: 15-year fixed rate mortgage at 4.75%. Adjustable Rate: 3/1 ARM, 15-year maturity, 3% initial rate which you anticipate will move up to 6% for years 4 and 5. Interest Only: 8.5% interest rate that will not change for the next five years. For detailed help on Amortization Tables, view the Amortization Example Video located in the Table of Contents -> Learning Modules -> Week 7 area of D2L. . 100% $ % 0.00 123 Default (Ca... - 11 B I A. 17 IV cu 1. - - E17 fx A B D E F G H 1 1 Names: FIN 460: Project #2 - Adjustable Rate Mortgage 2 3 4 5 6 7 8 Assumptions: Purchase Price Loan Term (years) Initial Interest Rate Years until Reset Year 4 and 5 Rate Calculations: Down Payment Beginning Loan Balance Initial Monthly Pmt Year 4/5 Pmt 270,000 15 3.00% 3 6.00% 9 10 Use PMT function (adjust beginning value to reflect ending balance for year 3 and shorten to a 12 year loan using new rate) 11 12 13 Month Beginning Balance Payment Interest Principal Ending Balance 14 1 15 2 3 16 17 4 18 19 20 5 6 7 8 9 21 22 23 10 11 24 25 12 26 13 27 14 15 28 + = MINI Closing Fully Amortizing ARM - Interest Only ExploreStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Practical Financial Management

Authors: William R. Lasher

4th Edition

0324260768, 9780324260762