Answered step by step

Verified Expert Solution

Question

1 Approved Answer

I need help with (c)(ii), a detailed answer that covers all the points given in the examiner's commentaries and have a clear argument point. Thanks!

I need help with (c)(ii), a detailed answer that covers all the points given in the examiner's commentaries and have a clear argument point. Thanks!

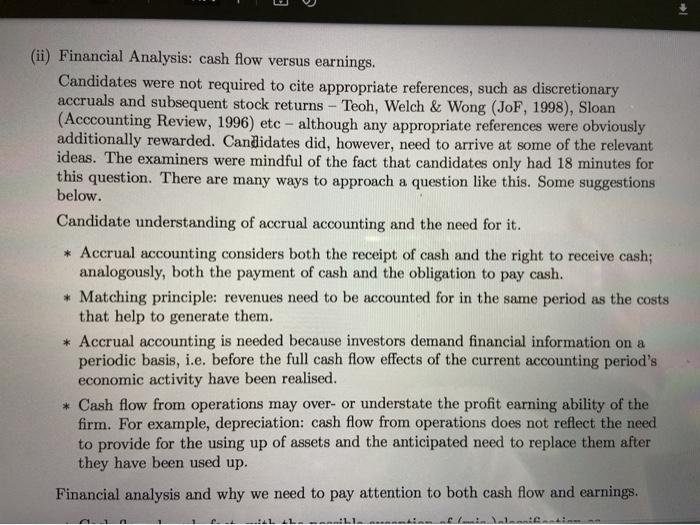

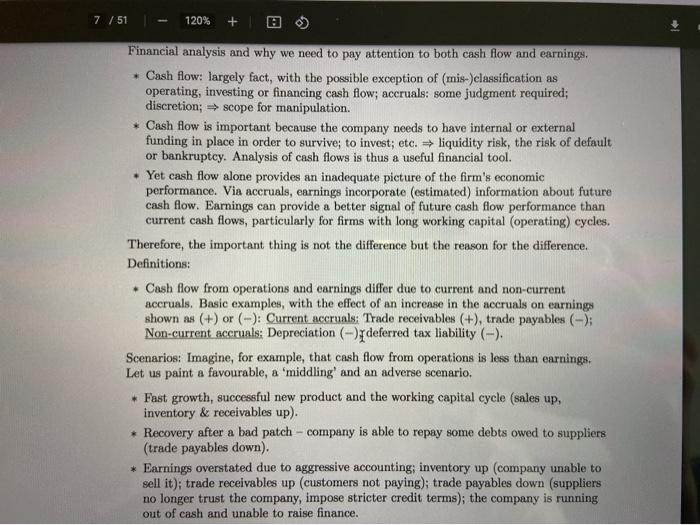

(c) Provide an analytical discussion of one of the following two questions. Either: (i) Would it be possible to the improve comparability of financial statements within an industry, and hence to improve the informational efficiency of equity markets, by reducing management discretion in financial reporting? Or: (ii) When undertaking financial analysis, should we pay more attention to cash flow information or to earnings information? (10 marks) (ii) Financial Analysis: cash flow versus earnings. Candidates were not required to cite appropriate references, such as discretionary accruals and subsequent stock returns - Teoh, Welch & Wong (JoF, 1998), Sloan (Acccounting Review, 1996) etc - although any appropriate references were obviously additionally rewarded. Candidates did, however, need to arrive at some of the relevant ideas. The examiners were mindful of the fact that candidates only had 18 minutes for this question. There are many ways to approach a question like this. Some suggestions below. Candidate understanding of accrual accounting and the need for it. * Accrual accounting considers both the receipt of cash and the right to receive cash; analogously, both the payment of cash and the obligation to pay cash. * Matching principle: revenues need to be accounted for in the same period as the costs that help to generate them. * Accrual accounting is needed because investors demand financial information on a periodic basis, i.e. before the full cash flow effects of the current accounting period's economic activity have been realised. * Cash flow from operations may over- or understate the profit earning ability of the firm. For example, depreciation: cash flow from operations does not reflect the need to provide for the using up of assets and the anticipated need to replace them after they have been used up. Financial analysis and why we need to pay attention to both cash flow and earnings. 7 / 51 120% + 0 Financial analysis and why we need to pay attention to both cash flow and earnings, Cash flow: largely fact, with the possible exception of (mis-)classification as operating, investing or financing cash flow; accruals: some judgment required; discretion; scope for manipulation. * Cash flow is important because the company needs to have internal or external funding in place in order to survive; to invest; etc. liquidity risk, the risk of default or bankruptcy. Analysis of cash flows is thus a useful financial tool. Yet cash flow alone provides an inadequate picture of the firm's economic performance. Via accruals, earnings incorporate (estimated) information about future cash flow. Earnings can provide a better signal of future cash flow performance than current cash flows, particularly for firms with long working capital (operating) cycles. Therefore, the important thing is not the difference but the reason for the difference. Definitions: - Cash flow from operations and earnings differ due to current and non-current accruals. Basic examples, with the effect of an increase in the accruals on earnings shown as (+) or (-): Current accruals: Trade receivables (+), trade payables (-); Non-current accruals: Depreciation (-) deferred tax liability (-). Scenarios: Imagine, for example, that cash flow from operations is less than earnings. Let us paint a favourable, a 'middling' and an adverse scenario, Fast growth, successful new product and the working capital cycle (sales up, inventory & receivables up). Recovery after a bad patch - company is able to repay some debts owed to suppliers (trade payables down). * Earnings overstated due to aggressive accounting, inventory up (company unable to sell it); trade receivables up (customers not paying); trade payables down (suppliers no longer trust the company, impose stricter credit terms); the company is running out of cash and unable to raise finance. (c) Provide an analytical discussion of one of the following two questions. Either: (i) Would it be possible to the improve comparability of financial statements within an industry, and hence to improve the informational efficiency of equity markets, by reducing management discretion in financial reporting? Or: (ii) When undertaking financial analysis, should we pay more attention to cash flow information or to earnings information? (10 marks) (ii) Financial Analysis: cash flow versus earnings. Candidates were not required to cite appropriate references, such as discretionary accruals and subsequent stock returns - Teoh, Welch & Wong (JoF, 1998), Sloan (Acccounting Review, 1996) etc - although any appropriate references were obviously additionally rewarded. Candidates did, however, need to arrive at some of the relevant ideas. The examiners were mindful of the fact that candidates only had 18 minutes for this question. There are many ways to approach a question like this. Some suggestions below. Candidate understanding of accrual accounting and the need for it. * Accrual accounting considers both the receipt of cash and the right to receive cash; analogously, both the payment of cash and the obligation to pay cash. * Matching principle: revenues need to be accounted for in the same period as the costs that help to generate them. * Accrual accounting is needed because investors demand financial information on a periodic basis, i.e. before the full cash flow effects of the current accounting period's economic activity have been realised. * Cash flow from operations may over- or understate the profit earning ability of the firm. For example, depreciation: cash flow from operations does not reflect the need to provide for the using up of assets and the anticipated need to replace them after they have been used up. Financial analysis and why we need to pay attention to both cash flow and earnings. 7 / 51 120% + 0 Financial analysis and why we need to pay attention to both cash flow and earnings, Cash flow: largely fact, with the possible exception of (mis-)classification as operating, investing or financing cash flow; accruals: some judgment required; discretion; scope for manipulation. * Cash flow is important because the company needs to have internal or external funding in place in order to survive; to invest; etc. liquidity risk, the risk of default or bankruptcy. Analysis of cash flows is thus a useful financial tool. Yet cash flow alone provides an inadequate picture of the firm's economic performance. Via accruals, earnings incorporate (estimated) information about future cash flow. Earnings can provide a better signal of future cash flow performance than current cash flows, particularly for firms with long working capital (operating) cycles. Therefore, the important thing is not the difference but the reason for the difference. Definitions: - Cash flow from operations and earnings differ due to current and non-current accruals. Basic examples, with the effect of an increase in the accruals on earnings shown as (+) or (-): Current accruals: Trade receivables (+), trade payables (-); Non-current accruals: Depreciation (-) deferred tax liability (-). Scenarios: Imagine, for example, that cash flow from operations is less than earnings. Let us paint a favourable, a 'middling' and an adverse scenario, Fast growth, successful new product and the working capital cycle (sales up, inventory & receivables up). Recovery after a bad patch - company is able to repay some debts owed to suppliers (trade payables down). * Earnings overstated due to aggressive accounting, inventory up (company unable to sell it); trade receivables up (customers not paying); trade payables down (suppliers no longer trust the company, impose stricter credit terms); the company is running out of cash and unable to raise finance Here are the examiner's commentaries to (c)(ii):

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting The Basics

Authors: Ilias Basioudis

1st Edition

1138605514, 9781138605510