I need help with question 3 please!

I need help with question 3 please!

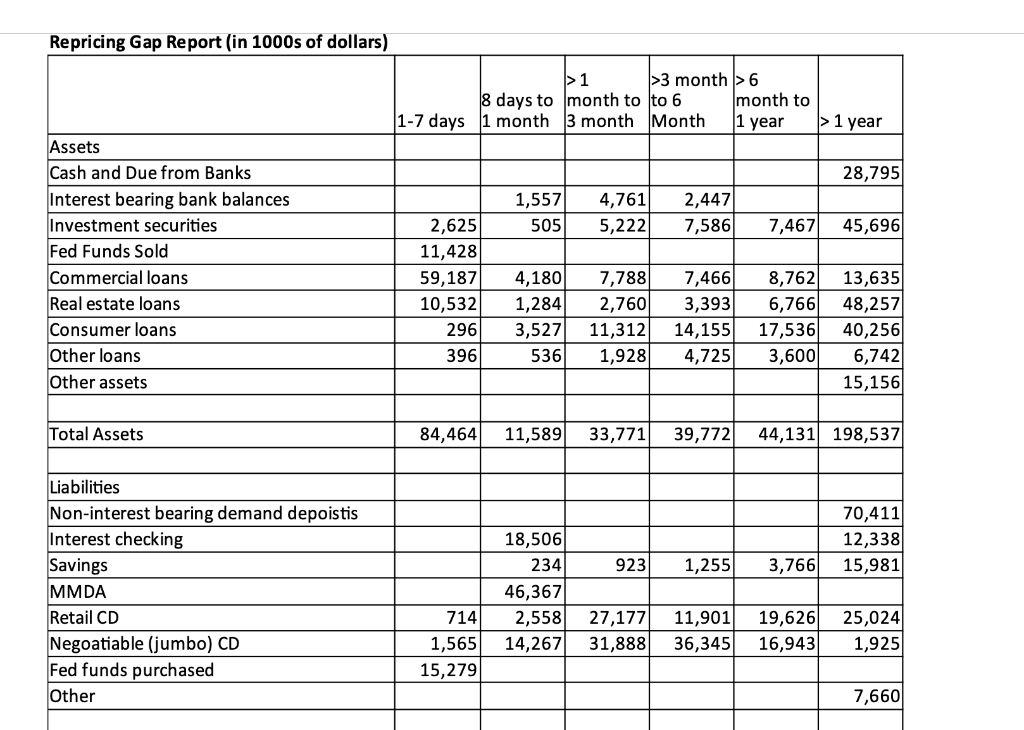

Repricing Gap Report (in 1000s of dollars) 1 >3 month>6 8 days to month to to 6 month to 1-7 days 1 month 3 month Month year > 1 year 28,795 1,557 4,761 5,222 2,447 7,586 505 7,467 45,696 Assets Cash and Due from Banks Interest bearing bank balances Investment securities Fed Funds Sold Commercial loans Real estate loans Consumer loans Other loans Other assets 2,625 11,428 59,187 10,532 296 396 4,180 1,284 3,527 536 7,788 2,760 11,312 1,928 7,466 3,393 14,155 4,725 8,762 6,766 17,536 3,600 13,635 48,257 40,256 6,742 15,156 Total Assets 84,464 11,589 33,771 39,772 44,131 198,537 70,411 12,338 15,981 923 1,255 3,766 Liabilities Non-interest bearing demand depoistis Interest checking Savings MMDA Retail CD Negoatiable (jumbo) CD Fed funds purchased Other 18,506 234 46,367 2,558 14,267 714 1,565 15,279 27,177 31,888 11,901 36,345 19,626 16,943 25,024 1,925 7,660 b. What would the duration be if it paid coupons semiannually! 3. a. b. c. Calculate the duration of a five year Treasury bond with a 8% annual coupon selling at par. Use duration to calculate the approximate price change if interest rates increase by 20 basis points for the security in part a. (That is, use the formula you were given.) Use the mechanics of bond valuation to calculate the exact price change if interest rates increase by 20 basis points for the security in part a. (That is, calculate the exact price using your calculator.) Why are your answers for parts b and c different? d. Repricing Gap Report (in 1000s of dollars) 1 >3 month>6 8 days to month to to 6 month to 1-7 days 1 month 3 month Month year > 1 year 28,795 1,557 4,761 5,222 2,447 7,586 505 7,467 45,696 Assets Cash and Due from Banks Interest bearing bank balances Investment securities Fed Funds Sold Commercial loans Real estate loans Consumer loans Other loans Other assets 2,625 11,428 59,187 10,532 296 396 4,180 1,284 3,527 536 7,788 2,760 11,312 1,928 7,466 3,393 14,155 4,725 8,762 6,766 17,536 3,600 13,635 48,257 40,256 6,742 15,156 Total Assets 84,464 11,589 33,771 39,772 44,131 198,537 70,411 12,338 15,981 923 1,255 3,766 Liabilities Non-interest bearing demand depoistis Interest checking Savings MMDA Retail CD Negoatiable (jumbo) CD Fed funds purchased Other 18,506 234 46,367 2,558 14,267 714 1,565 15,279 27,177 31,888 11,901 36,345 19,626 16,943 25,024 1,925 7,660 b. What would the duration be if it paid coupons semiannually! 3. a. b. c. Calculate the duration of a five year Treasury bond with a 8% annual coupon selling at par. Use duration to calculate the approximate price change if interest rates increase by 20 basis points for the security in part a. (That is, use the formula you were given.) Use the mechanics of bond valuation to calculate the exact price change if interest rates increase by 20 basis points for the security in part a. (That is, calculate the exact price using your calculator.) Why are your answers for parts b and c different? d