Answered step by step

Verified Expert Solution

Question

1 Approved Answer

i need help with tax return forms 4562 and 4797 Melodic Musical Sales, Inc.-Book Balance Sheet Information Account January 1, 2019 Debit Credit December 31,

i need help with tax return forms 4562 and 4797

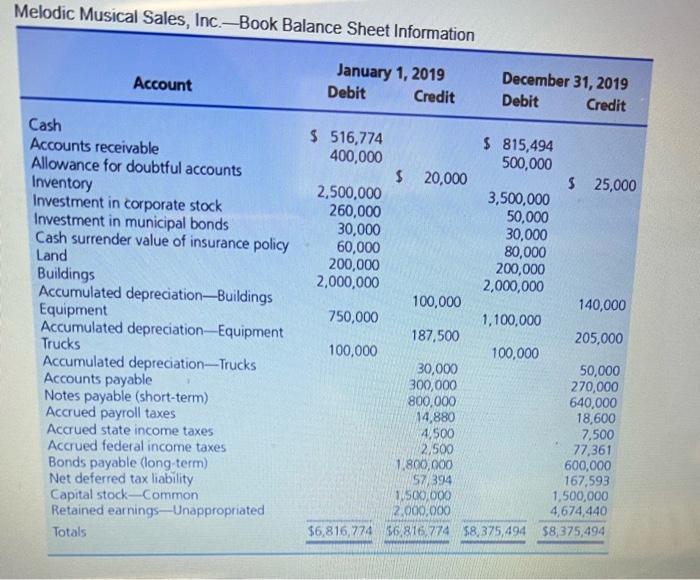

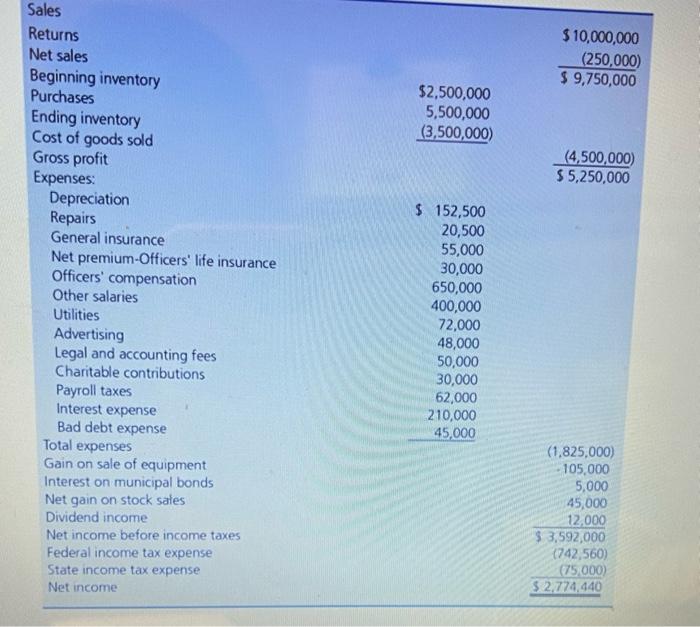

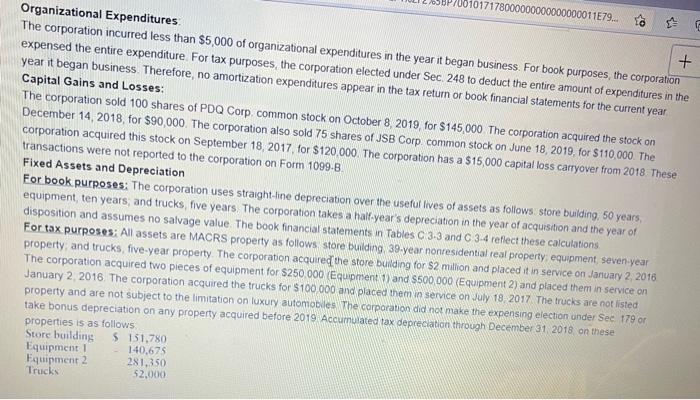

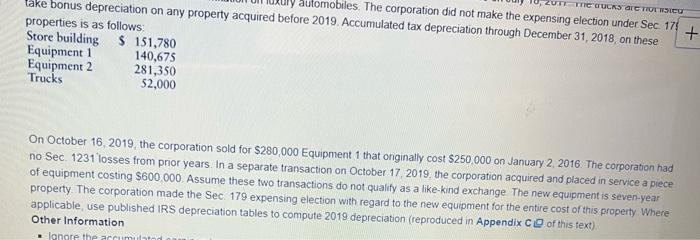

Melodic Musical Sales, Inc.-Book Balance Sheet Information Account January 1, 2019 Debit Credit December 31, 2019 Debit Credit Cash Accounts receivable Allowance for doubtful accounts Inventory Investment in corporate stock Investment in municipal bonds Cash surrender value of insurance policy Land Buildings Accumulated depreciationBuildings Equipment Accumulated depreciation-Equipment Trucks Accumulated depreciation--Trucks Accounts payable Notes payable (short-term) Accrued payroll taxes Accrued state income taxes Accrued federal income taxes Bonds payable (long-term) Net deferred tax liability Capital stock-Common Retained earnings-Unappropriated Totals $ 516,774 $ 815,494 400,000 500,000 $ 20,000 $ 25,000 2,500,000 3,500,000 260,000 50,000 30,000 30,000 60,000 80,000 200,000 200,000 2,000,000 2,000,000 100,000 140,000 750,000 1,100,000 187,500 205,000 100,000 100,000 30,000 50,000 300,000 270,000 800,000 640,000 14,880 18,600 4,500 7.500 2,500 77,361 1.800,000 600,000 57,394 167,593 3.500,000 1,500,000 2.000.000 4,674,440 $6,816,774 56,816,774 58,375,494 $8,375,494 $10,000,000 (250,000) $ 9,750,000 $2,500,000 5,500,000 (3,500,000) (4,500,000 55,250,000 Sales Returns Net sales Beginning inventory Purchases Ending inventory Cost of goods sold Gross profit Expenses: Depreciation Repairs General insurance Net premium-Officers' life insurance Officers' compensation Other salaries Utilities Advertising Legal and accounting fees Charitable contributions Payroll taxes Interest expense Bad debt expense Total expenses Gain on sale of equipment Interest on municipal bonds Net gain on stock sales Dividend income Net income before income taxes Federal income tax expense State income tax expense Net income $ 152,500 20,500 55,000 30,000 650,000 400,000 72,000 48,000 50,000 30,000 62,000 210,000 45,000 (1.825,000) 105,000 5,000 45,000 12,000 $ 3,592,000 (742,560) (75,000) $ 2.774,440 0000000000011E79... + Organizational Expenditures The corporation incurred less than $5,000 of organizational expenditures in the year it began business. For book purposes the corporation + expensed the entire expenditure For tax purposes, the corporation elected under Sec 248 to deduct the entire amount of expenditures in the year it began business. Therefore, no amortization expenditures appear in the tax return or book financial statements for the current year Capital Gains and Losses: The corporation sold 100 shares of PDQ Corp common stock on October 8, 2019 for $145,000 The corporation acquired the stock on December 14, 2018, for $90,000. The corporation also sold 75 shares of JSB Corp. common stock on June 18, 2019 for $110,000. The corporation acquired this stock on September 18, 2017 for $120,000. The corporation has a $15,000 capital loss carryover from 2018 These transactions were not reported to the corporation on Form 1099-8. Fixed Assets and Depreciation For book, purposes: The corporation uses straight-line depreciation over the useful lives of assets as follows store building, 50 years, equipment, ten years, and trucks, five years. The corporation takes a half-year's depreciation in the year of acquisition and the year of disposition and assumes no salvage value. The book financial statements in Tables C 3-3 and C 3-4 reflect these calculations For tax purposes: All assets are MACRS property as follows store building 39-year nonresidential real property, equipment, seven-year property and trucks, five-year property. The corporation acquire the store building for $2 million and placed it in service on January 2, 2016 The corporation acquired two pieces of equipment for $250.000 Equipment ) and $500,000 (Equipment 2) and placed them in service on January 2, 2016. The corporation acquired the trucks for $100 000 and placed them in service on July 18, 2017 The trucks are not listed property and are not subject to the limitation on luxury automobiles The corporation did not make the expensing election under Sec 179 or take bonus depreciation on any property acquired before 2019 Accumulated tax depreciation through December 31, 2018 on these properties is as follows: Store building $ 151,780 Equipment 140,675 Equipment 2 281.350 Trucks 52.000 TIIUCRS TELU automobiles. The corporation did not make the expensing election under Sec 17 take bonus depreciation on any property acquired before 2019. Accumulated tax depreciation through December 31, 2018, on these properties is as follows: Store building $ 151,780 Equipment 1 140,675 Equipment 2 281,350 Trucks 52,000 + On October 16, 2019, the corporation sold for $280,000 Equipment that onginally cost $250,000 on January 2, 2016. The corporation had no Sec. 1231 losses from prior years. In a separate transaction on October 17, 2019, the corporation acquired and placed in service a piece of equipment costing $600.000. Assume these two transactions do not quality as a like kind exchange The new equipment is seven-year property. The corporation made the Sec 179 expensing election with regard to the new equipment for the entire cost of this property. Where applicable, use published IRS depreciation tables to compute 2019 depreciation (reproduced in Appendix C of this text) Other Information langre the arcumulated $ 51,280 15,613 62.450 19.200 $148,543 $600,000 $748,543 Current year depreciation on property placed in service before 2019. Building ($2,000,000 x 0.02564) Equipment 1 ($250,000 x 0.1249 x 0.5) Equipment 2 ($500,000 x 0.1249) Trucks ($100,000 x 0.192) Total Current year depreciation on equipment placed in service in 2019 Sec. 179 expensing Total current-year depreciation Capital gains and losses for 2019: Short-term capital gain on sale of PDQ stock Long-term capital loss on sale of JSB stock Sale of Equipment 1: Selling price Cost $250,000 Minus: Accumulated depreciation (156,288) Adjusted basis Gain recognized Sec. 1245 recapture Sec. 1231 gain $ 55,000 (10,000) $280,000 (93,712) $186,288 $156,288 $ 30,000 Underpayment penalty: Omit Form 2220 and just insert $3,809 penalty on Form 1120, Page 1, Line 33. Schedule M-3: Omit this schedule. Prepare the following forms/schedules and submit in the following order: 1. Form 1120 (all 6 pages) 2. Schedule DV 3. Form 8949 4. Form 1125-AV 5. Form 1125-E 6. Form 4562 Melodic Musical Sales, Inc.-Book Balance Sheet Information Account January 1, 2019 Debit Credit December 31, 2019 Debit Credit Cash Accounts receivable Allowance for doubtful accounts Inventory Investment in corporate stock Investment in municipal bonds Cash surrender value of insurance policy Land Buildings Accumulated depreciationBuildings Equipment Accumulated depreciation-Equipment Trucks Accumulated depreciation--Trucks Accounts payable Notes payable (short-term) Accrued payroll taxes Accrued state income taxes Accrued federal income taxes Bonds payable (long-term) Net deferred tax liability Capital stock-Common Retained earnings-Unappropriated Totals $ 516,774 $ 815,494 400,000 500,000 $ 20,000 $ 25,000 2,500,000 3,500,000 260,000 50,000 30,000 30,000 60,000 80,000 200,000 200,000 2,000,000 2,000,000 100,000 140,000 750,000 1,100,000 187,500 205,000 100,000 100,000 30,000 50,000 300,000 270,000 800,000 640,000 14,880 18,600 4,500 7.500 2,500 77,361 1.800,000 600,000 57,394 167,593 3.500,000 1,500,000 2.000.000 4,674,440 $6,816,774 56,816,774 58,375,494 $8,375,494 $10,000,000 (250,000) $ 9,750,000 $2,500,000 5,500,000 (3,500,000) (4,500,000 55,250,000 Sales Returns Net sales Beginning inventory Purchases Ending inventory Cost of goods sold Gross profit Expenses: Depreciation Repairs General insurance Net premium-Officers' life insurance Officers' compensation Other salaries Utilities Advertising Legal and accounting fees Charitable contributions Payroll taxes Interest expense Bad debt expense Total expenses Gain on sale of equipment Interest on municipal bonds Net gain on stock sales Dividend income Net income before income taxes Federal income tax expense State income tax expense Net income $ 152,500 20,500 55,000 30,000 650,000 400,000 72,000 48,000 50,000 30,000 62,000 210,000 45,000 (1.825,000) 105,000 5,000 45,000 12,000 $ 3,592,000 (742,560) (75,000) $ 2.774,440 0000000000011E79... + Organizational Expenditures The corporation incurred less than $5,000 of organizational expenditures in the year it began business. For book purposes the corporation + expensed the entire expenditure For tax purposes, the corporation elected under Sec 248 to deduct the entire amount of expenditures in the year it began business. Therefore, no amortization expenditures appear in the tax return or book financial statements for the current year Capital Gains and Losses: The corporation sold 100 shares of PDQ Corp common stock on October 8, 2019 for $145,000 The corporation acquired the stock on December 14, 2018, for $90,000. The corporation also sold 75 shares of JSB Corp. common stock on June 18, 2019 for $110,000. The corporation acquired this stock on September 18, 2017 for $120,000. The corporation has a $15,000 capital loss carryover from 2018 These transactions were not reported to the corporation on Form 1099-8. Fixed Assets and Depreciation For book, purposes: The corporation uses straight-line depreciation over the useful lives of assets as follows store building, 50 years, equipment, ten years, and trucks, five years. The corporation takes a half-year's depreciation in the year of acquisition and the year of disposition and assumes no salvage value. The book financial statements in Tables C 3-3 and C 3-4 reflect these calculations For tax purposes: All assets are MACRS property as follows store building 39-year nonresidential real property, equipment, seven-year property and trucks, five-year property. The corporation acquire the store building for $2 million and placed it in service on January 2, 2016 The corporation acquired two pieces of equipment for $250.000 Equipment ) and $500,000 (Equipment 2) and placed them in service on January 2, 2016. The corporation acquired the trucks for $100 000 and placed them in service on July 18, 2017 The trucks are not listed property and are not subject to the limitation on luxury automobiles The corporation did not make the expensing election under Sec 179 or take bonus depreciation on any property acquired before 2019 Accumulated tax depreciation through December 31, 2018 on these properties is as follows: Store building $ 151,780 Equipment 140,675 Equipment 2 281.350 Trucks 52.000 TIIUCRS TELU automobiles. The corporation did not make the expensing election under Sec 17 take bonus depreciation on any property acquired before 2019. Accumulated tax depreciation through December 31, 2018, on these properties is as follows: Store building $ 151,780 Equipment 1 140,675 Equipment 2 281,350 Trucks 52,000 + On October 16, 2019, the corporation sold for $280,000 Equipment that onginally cost $250,000 on January 2, 2016. The corporation had no Sec. 1231 losses from prior years. In a separate transaction on October 17, 2019, the corporation acquired and placed in service a piece of equipment costing $600.000. Assume these two transactions do not quality as a like kind exchange The new equipment is seven-year property. The corporation made the Sec 179 expensing election with regard to the new equipment for the entire cost of this property. Where applicable, use published IRS depreciation tables to compute 2019 depreciation (reproduced in Appendix C of this text) Other Information langre the arcumulated $ 51,280 15,613 62.450 19.200 $148,543 $600,000 $748,543 Current year depreciation on property placed in service before 2019. Building ($2,000,000 x 0.02564) Equipment 1 ($250,000 x 0.1249 x 0.5) Equipment 2 ($500,000 x 0.1249) Trucks ($100,000 x 0.192) Total Current year depreciation on equipment placed in service in 2019 Sec. 179 expensing Total current-year depreciation Capital gains and losses for 2019: Short-term capital gain on sale of PDQ stock Long-term capital loss on sale of JSB stock Sale of Equipment 1: Selling price Cost $250,000 Minus: Accumulated depreciation (156,288) Adjusted basis Gain recognized Sec. 1245 recapture Sec. 1231 gain $ 55,000 (10,000) $280,000 (93,712) $186,288 $156,288 $ 30,000 Underpayment penalty: Omit Form 2220 and just insert $3,809 penalty on Form 1120, Page 1, Line 33. Schedule M-3: Omit this schedule. Prepare the following forms/schedules and submit in the following order: 1. Form 1120 (all 6 pages) 2. Schedule DV 3. Form 8949 4. Form 1125-AV 5. Form 1125-E 6. Form 4562 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: LibbyShort

7th Edition

78111021, 978-0078111020