Answered step by step

Verified Expert Solution

Question

1 Approved Answer

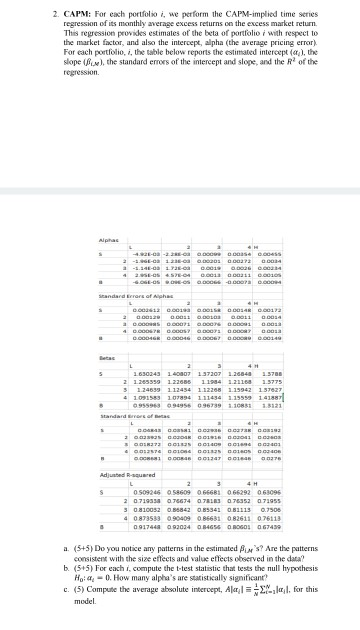

I need help with the above question, any help would be greatly appreciated. thanks. 2. CAPM: For each portfolo i, we perform the CAPM-implied time

I need help with the above question, any help would be greatly appreciated. thanks.

2. CAPM: For each portfolo i, we perform the CAPM-implied time series regression of its monthly average excess returns on the excess market return This regression providkes estimates of the beta of portfolio i with respect to the market factor, and also the intercept, alpha (the average pricing error) For each prtfolio, i, the table below reports the estimated intercept (a), the slope (..), the standard emors of the intercept and slope, and the R2 of the regression 0 000468 00046 21 285359 122688 11984 21168 3.5773 11394 955963a 0 66681 0 66292 0 4 087353 o 090409 92034 0 86681 0 82611 0 a. (5+5)Do you notice any patterns in the estimated Pr's? Are the patterns consistent with the size effects and value effects observed in the data b (55) For each i, compute the ttest statistic that tests the null hypothesis Ho: c.(5) Compute the average absolute intercept, Al 0. How many alpha's are statistically significant? 11",l, for this N model. 2. CAPM: For each portfolo i, we perform the CAPM-implied time series regression of its monthly average excess returns on the excess market return This regression providkes estimates of the beta of portfolio i with respect to the market factor, and also the intercept, alpha (the average pricing error) For each prtfolio, i, the table below reports the estimated intercept (a), the slope (..), the standard emors of the intercept and slope, and the R2 of the regression 0 000468 00046 21 285359 122688 11984 21168 3.5773 11394 955963a 0 66681 0 66292 0 4 087353 o 090409 92034 0 86681 0 82611 0 a. (5+5)Do you notice any patterns in the estimated Pr's? Are the patterns consistent with the size effects and value effects observed in the data b (55) For each i, compute the ttest statistic that tests the null hypothesis Ho: c.(5) Compute the average absolute intercept, Al 0. How many alpha's are statistically significant? 11",l, for this N modelStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Plain And Simple

Authors: Sebastian Nokes

1st Edition

0273731297, 978-0273731290