I need some help with the auditing case study, and I have attached the case and the rubric.

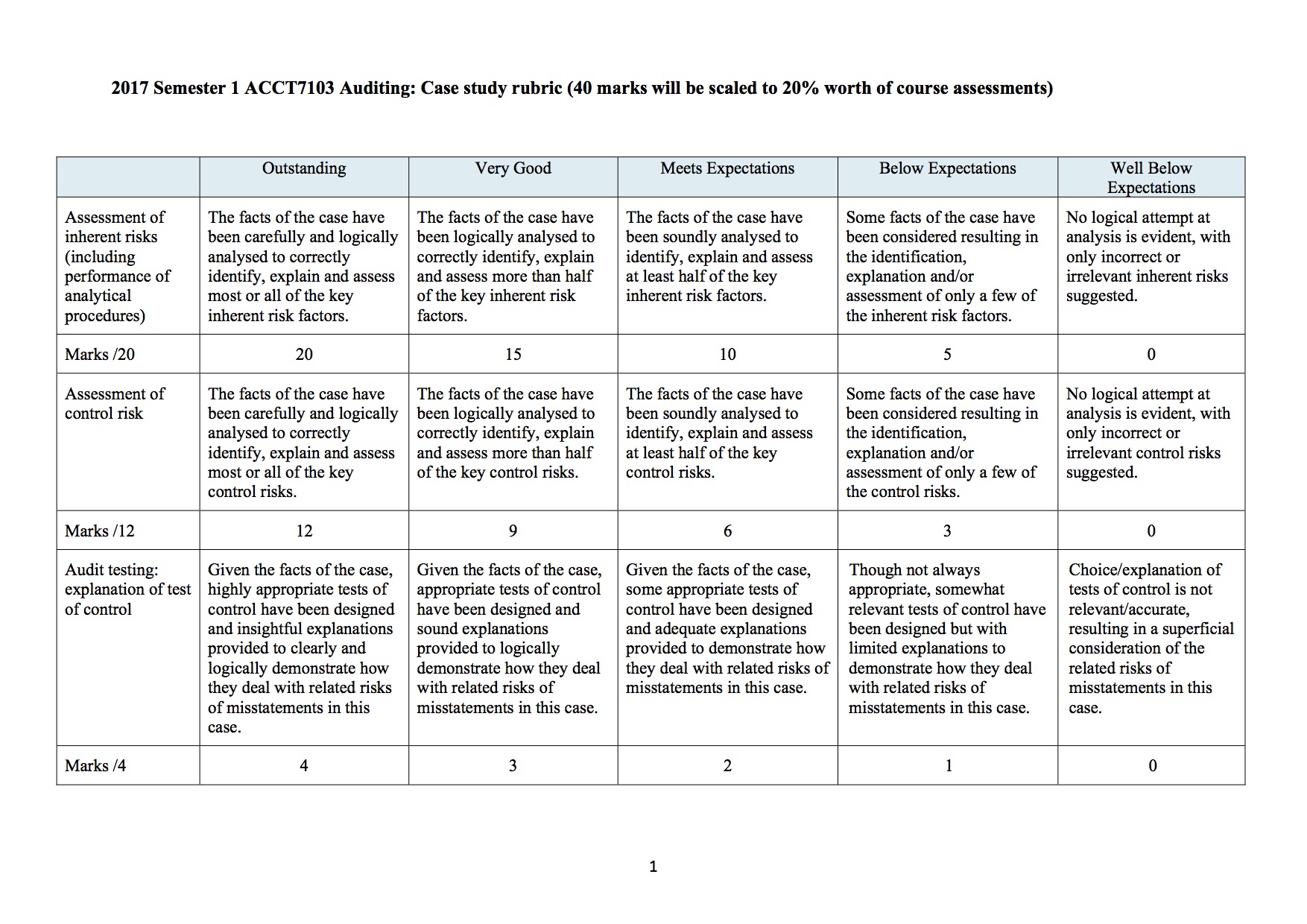

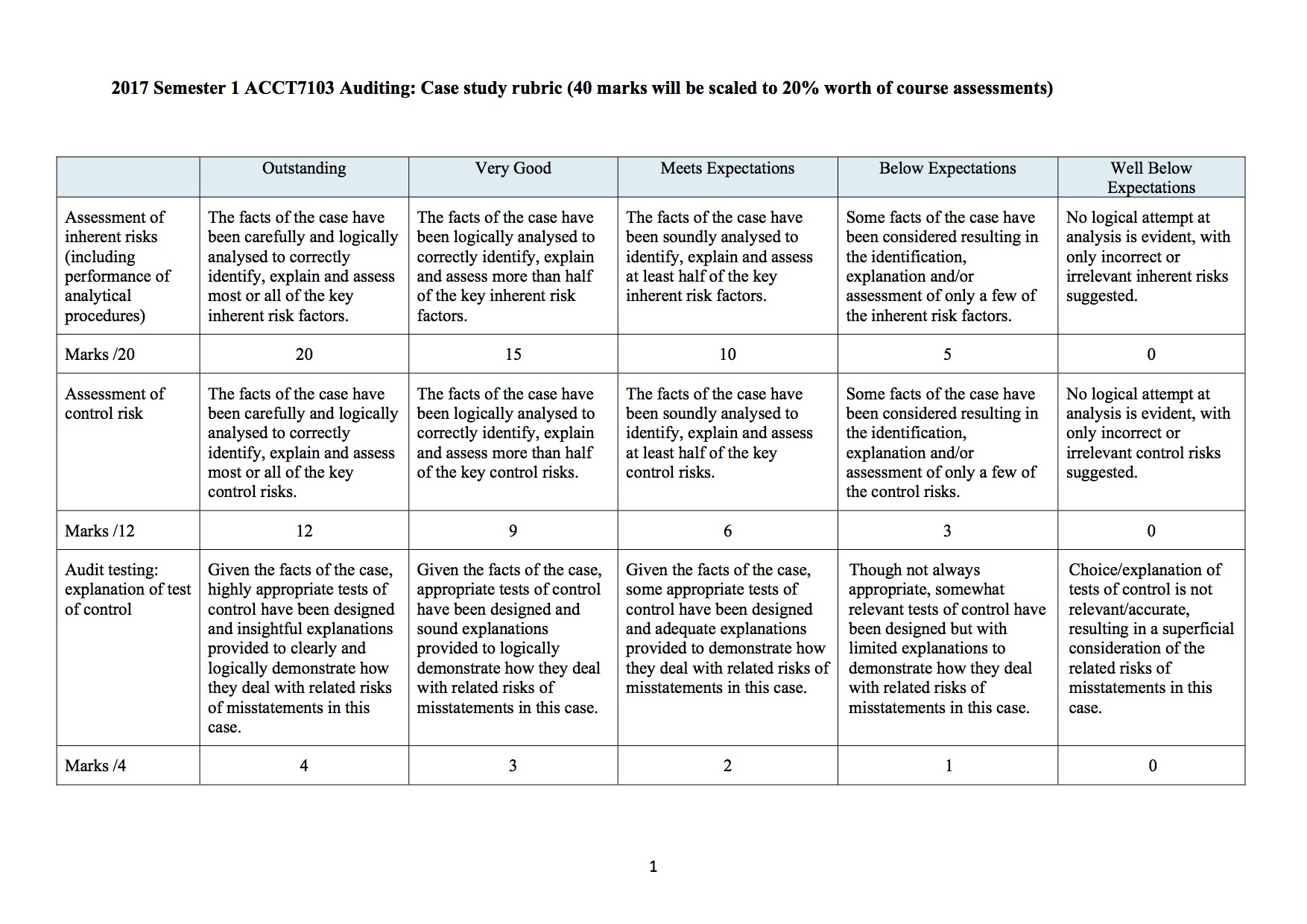

2017 Semester 1 ACCT7103 Auditing: Case study rubric (40 marks will be scaled to 20% worth of course assessments) Outstanding Very Good Meets Expectations Below Expectations Well Below Expectations Assessment of The facts of the case have The facts of the case have The facts of the case have Some facts of the case have No logical attempt at inherent risks been carefully and logically been logically analysed to been soundly analysed to been considered resulting in analysis is evident, with (including analysed to correctly correctly identify, explain identify, explain and assess the identication, only incorrect or performance of identify, explain and assess and assess more than half at least half of the key explanation andfor irrelevant inherent risks analytical most or all of the key of the key inherent risk inherent risk factors. assessment of only a few of suggested. procedures) inherent risk factors. factors. the inherent risk factors. Marks 1'20 20 l 5 l 0 5 0 Assessment of The facts of the case have The facts of the case have The facts of the case have Some facts of the case have No logical attempt at control risk been carefully and logically been logically analysed to been soundly analysed to been considered resulting in analysis is evident, with analysed to correctly correctly identify, explain identify, explain and assess the identication, only incorrect or identify, explain and assess and assess more than half at least half of the key explanation andfor irrelevant control risks most or all of the key of the key control risks. control risks. assessment of only a few of suggested. control risks. the control risks. Marks I 12 12 9 6 3 0 Audit testing: Given the facts of the case, Given the facts of the case, Given the facts of the case, Though not always Choice/explanation of explanation of test highly appropriate tests of appropriate tests of control some appropriate tests of appropriate, somewhat tests of control is not of control control have been designed have been designed and control have been designed relevant tests of control have relevant/accurate, and insightful explanations sound explanations and adequate explanations been designed but with resulting in a supercial provided to clearly and provided to logically provided to demonstrate how limited explanations to consideration of the logically demonstrate how demonstrate how they deal they deal with related risks of demonstrate how they deal related risks of they deal with related risks with related risks of misstatements in this case. with related risks of misstatements in this of misstatements in this misstatements in this case. misstatements in this case. case. case. Marks [4 4 3 0 You are a senior auditor of the accounting firm CST Partners. Your audit team is currently planning the 2016 audit of Posh Limited, a listed company that buys and sells home and office furniture. This is the third year your accounting firm is engaged to perform the audit for this client. st The financial year being audited ends on 31 December 2016. Past audit work and initial audit inquiries this year have revealed the following information: Posh Limited hired a new Chief Executive Officer (CEO) in 2013, and the company's sales and profit grew at an average rate of about 6% between 2013 and 2015. The board of directors was satisfied with the company's profit and share price performance, and rewarded the CEO with an annual cash bonus each year when profit growth exceeded 5%. The CEO is keen to maintain the good performance and started a plan to open 15 new stores around the country between 2016 and 2018. To raise the money required for the expansion plan, the company borrowed $7 million in February 2016 from a local bank. The debt contract requires the audit client's interest coverage ratio to be above 10, and the debt to assets ratio is required to be below 60%. The bank loan is not sufficient to cover all costs for the expansion plan, so the company is also planning to make a major public share issue in April 2017. To obtain the best share price possible, it is important for the company to show a strong and healthy financial report. The CEO e-mailed all employees in September 2016 to encourage all staff to focus on increasing revenues and cutting costs. A special bonus would be paid to all staff if the company's profit growth reached 5% for the 2016 financial year. The company spent a substantial amount of money in 2016 on its plan to open 7 new stores this year. All premises have been rented and five stores were opened by August 2016. However, renovation for the other two stores is behind schedule. The company has to pay the rent for the two locations while the renovation continues. Inventories were purchased for all 7 stores at the beginning of 2016. Inventories that are not on display in the stores are kept in the company's central warehouse. A cyclone in December 2016 caused severe flooding of the central warehouse. Consequently, water damage and mould/rust are serious concerns for the inventories in the warehouse. The auditor noted last year that inventory turnover slowed down in 2015. One of the reasons is because the company's main competitors also opened new stores close to the audit client's stores. In addition, the company's sales staff said some of the furniture that was trendy during 2013 and 2014 have become less popular with customers. The company's competitors have started to mark down the selling prices of such furniture since the end of 2015. The audit client has not held a clearance sale for older inventories yet. The audit client uses a perpetual inventory system. The accounting department is separate from other operating departments. Only the accounting staff has access to the accounting system. The CEO does not have direct access to the accounting records. The CEO needs to consult with the chief accountant about any proposed changes to the accounting records. If the chief accountant agrees that an adjustment is appropriate, the chief accountant would then make the change in the computer system. 2017-1 Auditing Case Study, p.1 The computer systems for sales, inventory management and accounting are integrated. However, access to different systems is restricted to authorised staff via individual passwords so that only sales staff has access to the sales computer system, and only accounting staff has access to the accounting system, etc. Authorisation of transactions is also performed via individual passwords. When customers make an order in store, sales staff enters the details for a sales invoice into the sales computer system. The sales system then sends the details of the sales invoice to the inventory management system. The warehouse staff uses this information to prepare delivery documents. Customers are required to sign a paper copy of the delivery document upon receipt of the furniture. Sales invoices and delivery documents are serially numbered. The original copy of the customer-signed delivery document is then sent to the accounting department while the warehouse staff keeps a duplicate copy of the document. At the end of each day, the warehouse manager gives authorisation in the inventory management system to process sales transactions for which delivery has been made. The system then updates the perpetual inventory records, and sends the sales transactions to the accounting system. The accounting staff checks the online sales invoices and the signed delivery documents before giving authorisation for the accounting system to record the sales in the accounting records. The accounting staff is required to regularly check recent sales transactions to see whether there are duplicate or missing sales invoice numbers, and whether each sales transaction has both a sales invoice number and a delivery document number. Monthly inventory reports are prepared by the inventory management computer system. These reports list different types of inventories by the date the last sale was made for a particular type of inventory. That is, these \"last sales\" reports help show inventory categories that have not had a sale for some time. The total value of each inventory category is also shown in the report. A copy of the report is distributed to the sales manager, purchase manager, chief accountant and the CEO. These reports are often used for reference when senior accounting staff holds meetings to discuss major accounting issues such as inventory write-downs. The audit client's draft financial statements for 2016 do not include an inventory write-down expense or an allowance for inventory obsolescence account. Inquiries of the accounting staff reveal that the chief accountant said there is no need to recognise unrealised inventory losses because the amount of the loss is uncertain so the information would be misleading to financial report users. The chief accountant told the staff that inventory write-down expense will be recorded only when inventory items are actually sold. The chief accountant was hired by the CEO three years ago and they are close friends. The chief accountant keeps the CEO updated about the company's financial progress and discusses major accounting issues with the CEO. However, they both say that the CEO does not attempt to override the chief accountant's professional judgment. Both the CEO and chief accountant are very friendly to the auditors and the directors. These managers have a good relationship with the board of directors. 2017-1 Auditing Case Study, p.2 The following table shows some of the audit client's ratios over the period of 2013 to 2016. The ratios for 2016 are based on unaudited financial results. Interest coverage ratio = Net profit divided by interest expense. Debt to assets ratio = Total liabilities divided by total assets. Profit growth = the difference between current period profit and prior period profit divided by prior period profit, i.e., (Profit t - Profit t-1) / Profit t-1. Inventory turnover = cost of goods sold for year t divided by average inventory (i.e., the average of beginning and ending inventory balances for year t). Required For the (A) occurrence general audit objective of the sales revenue account, and (B) the net realisable value general audit objective of the inventory account, answer all of the following questions in accordance with the Australian Auditing Standards. You need to perform your analysis using the facts in the case study. For each of the two audit objectives of the accounts specified above: . (1) Assess inherent risk and perform analytical procedures to assess the likelihood of misstatements for each of the general audit objectives of the accounts given above. Analyse and explain your findings. (Total 20 marks) . (2) Assess control risk for each of the general audit objectives of the accounts given above. In your answer, identify existing internal controls that are relevant to the specified audit objectives and briefly explain how each internal control can prevent/detect misstatements for the specified audit objectives. (12 marks) . (3) Identify an existing internal control that is specific to each of the two general audit objectives of the accounts specified above, and design one test of control for each case. The internal controls and tests of controls must be based on the facts given in the case study. Briefly explain how the tests of controls specifically check the relevant audit objectives of the accounts specified. (4 marks) . (4) Design one substantive procedure that produces reasonably reliable evidence for each of the general audit objectives of the accounts given above. Do NOT use the same procedures here as the tests of controls in part (3). Do NOT use analytical procedures for sales occurrence. (4 marks)