Answered step by step

Verified Expert Solution

Question

1 Approved Answer

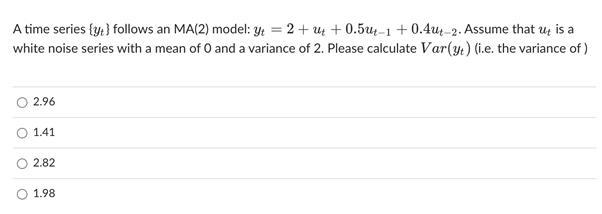

A time series {y} follows an MA(2) model: y = 2 + +0.5ut-1+0.4ut-2. Assume that u is a white noise series with a mean

A time series {y} follows an MA(2) model: y = 2 + +0.5ut-1+0.4ut-2. Assume that u is a white noise series with a mean of O and a variance of 2. Please calculate Var(y+) (i.e. the variance of) 2.96 1.41 2.82 1.98

Step by Step Solution

★★★★★

3.50 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

The detailed answer for the above question is provided below The given time series foll...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Electric Machinery

Authors: Charles Kingsley, Jr, Stephen D. Umans

6th Edition

71230106, 9780073660097, 73660094, 978-0071230100