I only need help with the answer to E.

I only need help with the answer to E.

Here is the spreadsheet I have but I am off by 140,000 in the equity investment account.

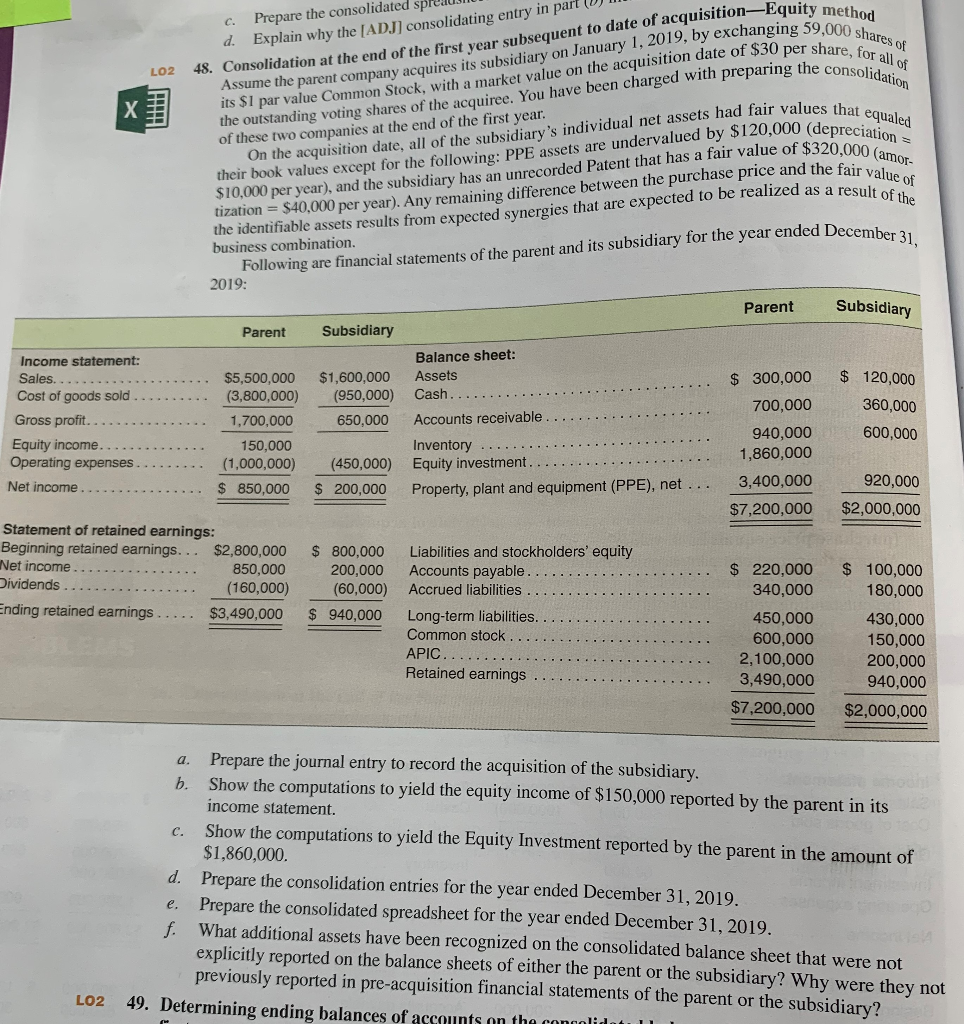

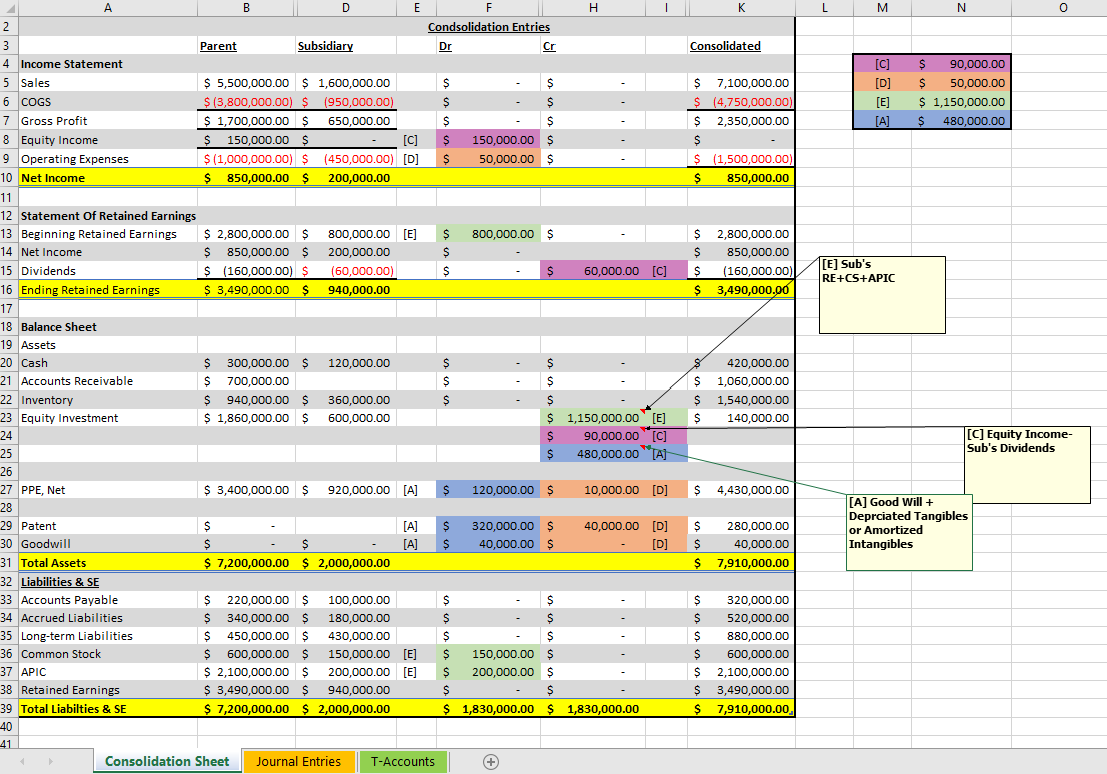

c. Prepare the consolidated sp d. Explain why the (ADJ) consolidating entry in part 48. Consolidation at the end of the first year subsequent to date of acquisition-Equity method Assume the parent company acquires its subsidiary on January 1, 2019, by exchanging 59,000 shares of its $1 par value Common Stock, with a market value on the acquisition date of $30 per share, for all of the outstanding voting shares of the acquiree. You have been charged with preparing the consolidation On the acquisition date, all of the subsidiary's individual net assets had fair values that equaled $10,000 per year), and the subsidiary has an unrecorded Patent that has a fair value of $320,000 (amor- their book values except for the following: PPE assets are undervalued by $120,000 (depreciation $40,000 per year). Any remaining difference between the purchase price and the fair value of the identifiable assets results from expected synergies that are expected to be realized as a result of the Following are financial statements of the parent and its subsidiary for the year ended December 31, LO2 tization business combination. of these two companies at the end of the first year. 2019: Parent Subsidiary Parent Subsidiary $ 300,000 $ 120,000 700.000 Income statement: Sales... Cost of goods sold Gross profit. Equity income Operating expenses Net income $1,600,000 (950,000) 650,000 360,000 $5,500,000 (3,800,000) 1,700,000 150,000 (1,000,000) Balance sheet: Assets Cash. Accounts receivable Inventory Equity investment. Property, plant and equipment (PPE), net 600,000 940,000 1,860,000 (450,000) $ 200,000 $ 850,000 3,400,000 $7,200,000 920,000 $2,000,000 Statement of retained earnings: Beginning retained earnings... $2,800,000 Net income 850.000 Dividends.. (160,000) Ending retained earnings .... $3,490,000 $ 800.000 200,000 (60,000) $ 940,000 $ 100,000 180,000 Liabilities and stockholders' equity Accounts payable. Accrued liabilities Long-term liabilities. Common stock APIC.... Retained earnings $ 220,000 340,000 450,000 600,000 2,100,000 3,490,000 $7,200,000 430,000 150,000 200,000 940,000 $2,000,000 c. Prepare the journal entry to record the acquisition of the subsidiary. b. Show the computations to yield the equity income of $150,000 reported by the parent in its income statement. Show the computations to yield the Equity Investment reported by the parent in the amount of $1,860,000. d. Prepare the consolidation entries for the year ended December 31, 2019. Prepare the consolidated spreadsheet for the year ended December 31, 2019. f. What additional assets have been recognized on the consolidated balance sheet that were not explicitly reported on the balance sheets of either the parent or the subsidiary? Why were they not previously reported in pre-acquisition financial statements of the parent or the subsidiary? 49. Determining ending balances of accounts on the congolid e. LO2 F H L M N 0 Condsolidation Entries Dr Cr Consolidated $ $ $ [C] [D] [E] 90,000.00 $ 50,000.00 $ 1,150,000.00 $ 480,000.00 $ $ $ $ 150,000.00 $ 50,000.00 $ $ 7,100,000.00 $ (4,750,000.00) $ 2,350,000.00 $ $ (1,500,000.00 $ 850,000.00 $ S 800,000.00 $ $ $ $ 2,800,000.00 $ 850,000.00 $ (160,000.00) $ 3,490,000.00 $ 60,000.00 [C] [E] Sub's RE+CS+APIC A B D E 2 3 Parent Subsidiary 4. Income Statement 5 Sales $ 5,500,000.00 $ 1,600,000.00 6 COGS $ (3,800,000.00) $ (950,000.00) 7 Gross Profit $ 1,700,000.00 $ 650,000.00 8 Equity Income $ 150,000.00 $ [C] 9 Operating Expenses $(1,000,000.00) $ (450,000.00) [D] 10 Net Income $ 850,000.00 $ 200,000.00 11 12 Statement of Retained Earnings 13 Beginning Retained Earnings $ 2,800,000.00 $ 800,000.00 [E] 14 Net Income S 850,000.00 $ 200,000.00 15 Dividends $ (160,000.00) $ (60,000.00) 16 Ending Retained Earnings $ 3,490,000.00 $ 940,000.00 17 18 Balance Sheet 19 Assets 20 Cash 300,000.00 $ 120,000.00 21 Accounts Receivable $ 700,000.00 22 Inventory $ 940,000.00 $ 360,000.00 23 Equity Investment $ 1,860,000.00 $ 600,000.00 24 25 26 27 PPE, Net $ 3,400,000.00 $ 920,000.00 [A] 28 29 Patent $ [A] 30 Goodwill $ [A] 31 Total Assets $ 7,200,000.00 $ 2,000,000.00 32 Liabilities & SE 33 Accounts Payable S 220,000.00 $ 100,000.00 34 Accrued Liabilities $ 340,000.00 $ 180,000.00 35 Long-term Liabilities $ 450,000.00 $ 430,000.00 36 Common Stock $ 600,000.00 $ 150,000.00 [E] 37 APIC $ 2,100,000.00 $ 200,000.00 [E] 38 Retained Earnings $ 3,490,000.00 $ 940,000.00 39 Total Liabilties & SE $ 7,200,000.00 $ 2,000,000.00 40 $ $ S $ $ $ $ 1,150,000.00 [E] $ 90,000.00 [C] $ 480,000.00 TA] $ 420,000.00 1,060,000.00 1,540,000.00 140,000.00 S $ $ [C] Equity Income- Sub's Dividends $ 120,000.00 $ 10,000.00 [D] $ 4,430,000.00 $ 320,000.00 $ 40,000.00 $ 40,000.00 [D] [D] [A] Good Will + Deprciated Tangibles or Amortized Intangibles $ $ 280,000.00 $ 40,000.00 $ 7,910,000.00 $ . S $ $ - $ S S - $ 150,000.00 $ S 200,000.00 $ $ $ $ 1,830,000.00 $ 1,830,000.00 - $ 320,000.00 S 520,000.00 $ 880,000.00 $ 600,000.00 S 2,100,000.00 $ 3,490,000.00 $ 7,910,000.00 41 Consolidation Sheet Journal Entries T-Accounts (+ c. Prepare the consolidated sp d. Explain why the (ADJ) consolidating entry in part 48. Consolidation at the end of the first year subsequent to date of acquisition-Equity method Assume the parent company acquires its subsidiary on January 1, 2019, by exchanging 59,000 shares of its $1 par value Common Stock, with a market value on the acquisition date of $30 per share, for all of the outstanding voting shares of the acquiree. You have been charged with preparing the consolidation On the acquisition date, all of the subsidiary's individual net assets had fair values that equaled $10,000 per year), and the subsidiary has an unrecorded Patent that has a fair value of $320,000 (amor- their book values except for the following: PPE assets are undervalued by $120,000 (depreciation $40,000 per year). Any remaining difference between the purchase price and the fair value of the identifiable assets results from expected synergies that are expected to be realized as a result of the Following are financial statements of the parent and its subsidiary for the year ended December 31, LO2 tization business combination. of these two companies at the end of the first year. 2019: Parent Subsidiary Parent Subsidiary $ 300,000 $ 120,000 700.000 Income statement: Sales... Cost of goods sold Gross profit. Equity income Operating expenses Net income $1,600,000 (950,000) 650,000 360,000 $5,500,000 (3,800,000) 1,700,000 150,000 (1,000,000) Balance sheet: Assets Cash. Accounts receivable Inventory Equity investment. Property, plant and equipment (PPE), net 600,000 940,000 1,860,000 (450,000) $ 200,000 $ 850,000 3,400,000 $7,200,000 920,000 $2,000,000 Statement of retained earnings: Beginning retained earnings... $2,800,000 Net income 850.000 Dividends.. (160,000) Ending retained earnings .... $3,490,000 $ 800.000 200,000 (60,000) $ 940,000 $ 100,000 180,000 Liabilities and stockholders' equity Accounts payable. Accrued liabilities Long-term liabilities. Common stock APIC.... Retained earnings $ 220,000 340,000 450,000 600,000 2,100,000 3,490,000 $7,200,000 430,000 150,000 200,000 940,000 $2,000,000 c. Prepare the journal entry to record the acquisition of the subsidiary. b. Show the computations to yield the equity income of $150,000 reported by the parent in its income statement. Show the computations to yield the Equity Investment reported by the parent in the amount of $1,860,000. d. Prepare the consolidation entries for the year ended December 31, 2019. Prepare the consolidated spreadsheet for the year ended December 31, 2019. f. What additional assets have been recognized on the consolidated balance sheet that were not explicitly reported on the balance sheets of either the parent or the subsidiary? Why were they not previously reported in pre-acquisition financial statements of the parent or the subsidiary? 49. Determining ending balances of accounts on the congolid e. LO2 F H L M N 0 Condsolidation Entries Dr Cr Consolidated $ $ $ [C] [D] [E] 90,000.00 $ 50,000.00 $ 1,150,000.00 $ 480,000.00 $ $ $ $ 150,000.00 $ 50,000.00 $ $ 7,100,000.00 $ (4,750,000.00) $ 2,350,000.00 $ $ (1,500,000.00 $ 850,000.00 $ S 800,000.00 $ $ $ $ 2,800,000.00 $ 850,000.00 $ (160,000.00) $ 3,490,000.00 $ 60,000.00 [C] [E] Sub's RE+CS+APIC A B D E 2 3 Parent Subsidiary 4. Income Statement 5 Sales $ 5,500,000.00 $ 1,600,000.00 6 COGS $ (3,800,000.00) $ (950,000.00) 7 Gross Profit $ 1,700,000.00 $ 650,000.00 8 Equity Income $ 150,000.00 $ [C] 9 Operating Expenses $(1,000,000.00) $ (450,000.00) [D] 10 Net Income $ 850,000.00 $ 200,000.00 11 12 Statement of Retained Earnings 13 Beginning Retained Earnings $ 2,800,000.00 $ 800,000.00 [E] 14 Net Income S 850,000.00 $ 200,000.00 15 Dividends $ (160,000.00) $ (60,000.00) 16 Ending Retained Earnings $ 3,490,000.00 $ 940,000.00 17 18 Balance Sheet 19 Assets 20 Cash 300,000.00 $ 120,000.00 21 Accounts Receivable $ 700,000.00 22 Inventory $ 940,000.00 $ 360,000.00 23 Equity Investment $ 1,860,000.00 $ 600,000.00 24 25 26 27 PPE, Net $ 3,400,000.00 $ 920,000.00 [A] 28 29 Patent $ [A] 30 Goodwill $ [A] 31 Total Assets $ 7,200,000.00 $ 2,000,000.00 32 Liabilities & SE 33 Accounts Payable S 220,000.00 $ 100,000.00 34 Accrued Liabilities $ 340,000.00 $ 180,000.00 35 Long-term Liabilities $ 450,000.00 $ 430,000.00 36 Common Stock $ 600,000.00 $ 150,000.00 [E] 37 APIC $ 2,100,000.00 $ 200,000.00 [E] 38 Retained Earnings $ 3,490,000.00 $ 940,000.00 39 Total Liabilties & SE $ 7,200,000.00 $ 2,000,000.00 40 $ $ S $ $ $ $ 1,150,000.00 [E] $ 90,000.00 [C] $ 480,000.00 TA] $ 420,000.00 1,060,000.00 1,540,000.00 140,000.00 S $ $ [C] Equity Income- Sub's Dividends $ 120,000.00 $ 10,000.00 [D] $ 4,430,000.00 $ 320,000.00 $ 40,000.00 $ 40,000.00 [D] [D] [A] Good Will + Deprciated Tangibles or Amortized Intangibles $ $ 280,000.00 $ 40,000.00 $ 7,910,000.00 $ . S $ $ - $ S S - $ 150,000.00 $ S 200,000.00 $ $ $ $ 1,830,000.00 $ 1,830,000.00 - $ 320,000.00 S 520,000.00 $ 880,000.00 $ 600,000.00 S 2,100,000.00 $ 3,490,000.00 $ 7,910,000.00 41 Consolidation Sheet Journal Entries T-Accounts (+