I only need part e and f.

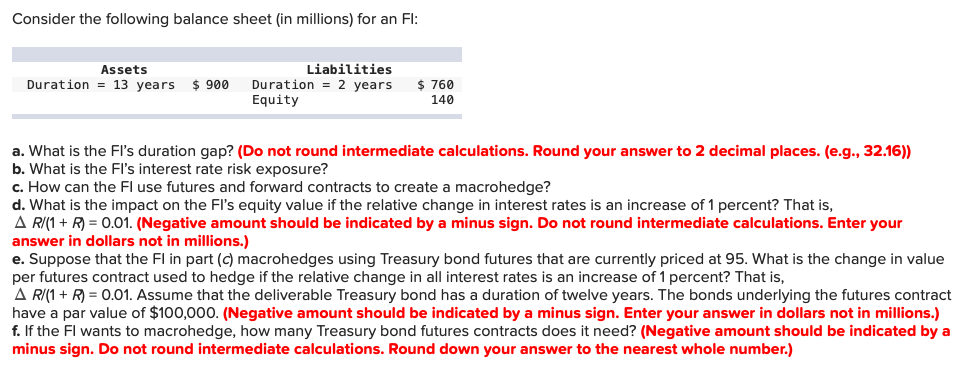

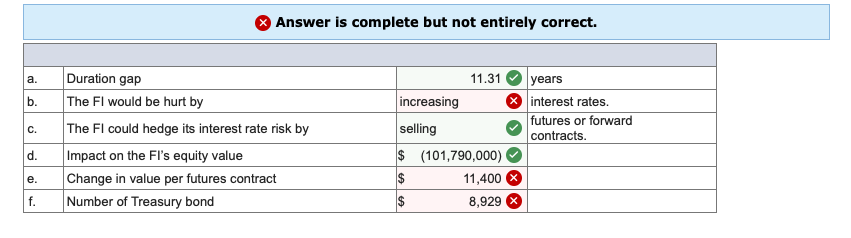

Consider the following balance sheet (in millions) for an FI: Assets Duration = 13 years $ 900 Liabilities Duration = 2 years Equity $ 760 140 a. What is the Fl's duration gap? (Do not round intermediate calculations. Round your answer to 2 decimal places. (e.g., 32.16)) b. What is the Fi's interest rate risk exposure? c. How can the Fl use futures and forward contracts to create a macrohedge? d. What is the impact on the Fl's equity value if the relative change in interest rates is an increase of 1 percent? That is, A R/(1+R) = 0.01. (Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Enter your answer in dollars not in millions.) e. Suppose that the Fl in part (c) macrohedges using Treasury bond futures that are currently priced at 95. What is the change in value per futures contract used to hedge if the relative change in all interest rates is an increase of 1 percent? That is, A R/(1+R) = 0.01. Assume that the deliverable Treasury bond has a duration of twelve years. The bonds underlying the futures contract have a par value of $100,000. (Negative amount should be indicated by a minus sign. Enter your answer in dollars not in millions.) f. If the Fl wants to macrohedge, how many Treasury bond futures contracts does it need? (Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Round down your answer to the nearest whole number.) Answer is complete but not entirely correct. a. b. C. Duration gap The Fl would be hurt by The Fl could hedge its interest rate risk by Impact on the Fi's equity value Change in value per futures contract Number of Treasury bond 11.31 years increasing % interest rates. futures or forward selling contracts. $ (101,790,000) $ 11,400 $ 8,929 e. f. Consider the following balance sheet (in millions) for an FI: Assets Duration = 13 years $ 900 Liabilities Duration = 2 years Equity $ 760 140 a. What is the Fl's duration gap? (Do not round intermediate calculations. Round your answer to 2 decimal places. (e.g., 32.16)) b. What is the Fi's interest rate risk exposure? c. How can the Fl use futures and forward contracts to create a macrohedge? d. What is the impact on the Fl's equity value if the relative change in interest rates is an increase of 1 percent? That is, A R/(1+R) = 0.01. (Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Enter your answer in dollars not in millions.) e. Suppose that the Fl in part (c) macrohedges using Treasury bond futures that are currently priced at 95. What is the change in value per futures contract used to hedge if the relative change in all interest rates is an increase of 1 percent? That is, A R/(1+R) = 0.01. Assume that the deliverable Treasury bond has a duration of twelve years. The bonds underlying the futures contract have a par value of $100,000. (Negative amount should be indicated by a minus sign. Enter your answer in dollars not in millions.) f. If the Fl wants to macrohedge, how many Treasury bond futures contracts does it need? (Negative amount should be indicated by a minus sign. Do not round intermediate calculations. Round down your answer to the nearest whole number.) Answer is complete but not entirely correct. a. b. C. Duration gap The Fl would be hurt by The Fl could hedge its interest rate risk by Impact on the Fi's equity value Change in value per futures contract Number of Treasury bond 11.31 years increasing % interest rates. futures or forward selling contracts. $ (101,790,000) $ 11,400 $ 8,929 e. f