Answered step by step

Verified Expert Solution

Question

1 Approved Answer

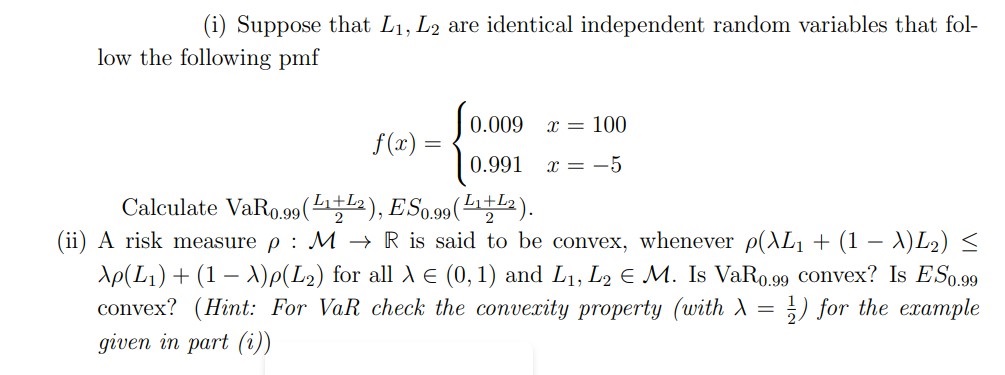

(i) Suppose that L1, L2 are identical independent random variables that fol- low the following pmf J0.009 f(x) = x = 100 0.991 x

(i) Suppose that L1, L2 are identical independent random variables that fol- low the following pmf J0.009 f(x) = x = 100 0.991 x = -5 Calculate VaR0.99 (+2), ES0.99 (L1+2). (ii) A risk measure p: MR is said to be convex, whenever p(AL + (1 - )L2) Ap(L1) + (1A)p(L2) for all AE (0, 1) and L1, L2 E M. Is VaR0.99 convex? Is ES0.99 convex? (Hint: For VaR check the convexity property (with \ = ) for the example given in part (i))

Step by Step Solution

★★★★★

3.33 Rating (147 Votes )

There are 3 Steps involved in it

Step: 1

i To calculate VaR099 12 and ES099 12 using the provided probability mass function pmf we need to fi...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Probability and Random Processes With Applications to Signal Processing and Communications

Authors: Scott Miller, Donald Childers

2nd edition

123869811, 978-0121726515, 121726517, 978-0130200716, 978-0123869814